Zomato: Reviewing Q4 Results

– Zomato delivered on its target of being adjusted EBITDA break-even for its business excluding quick commerce.

– Zomato has announced that they are targeting to get to positive adjusted EBITDA & PAT on a consolidated basis (including quick commerce) within the next four quarters.

– In this article, I will look at Zomato’s three businesses individually and see how they did against my expectations from my previous article (https://www.thryvv.in/article/zomato-is-there-enough-juice-left-at-current-valuation/).

– In the end, I value Zomato based on the sum of the three businesses.

Since this is a follow-up article, I am not going into the details of Zomato’s three businesses. Rather, I am going to jump straight into the Q4 & FY23 numbers and see how they did against my assumptions. I will also review whether I was too optimistic or pessimistic in my future assumptions and what the revised valuation looks like.

If you are interested in learning a bit more about the food delivery, Hyperpure, and Blinkit business, please read my previous article here. (https://www.thryvv.in/article/zomato-is-there-enough-juice-left-at-current-valuation/).

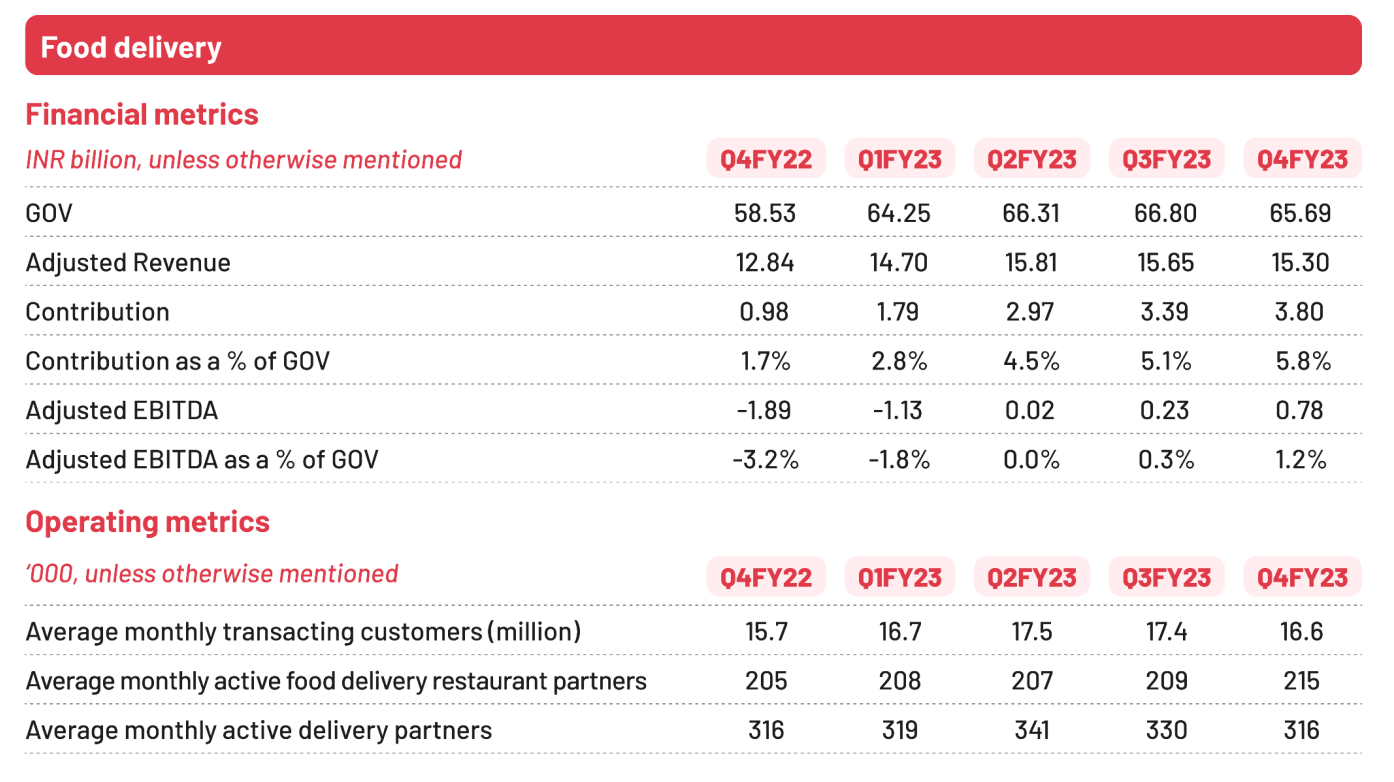

Zomato’s Food Delivery Business

Looking at the Q4FY23 numbers, we can see that Zomato is making good progress on the Adjusted EBITDA. However, the YoY adjusted revenue growth is around 19% for Q4 and the QoQ adjusted revenue has shown a negative growth. While the GOV has grown by around 12% YoY, it has remained almost flat since Q1FY23. The average monthly transacting customers have grown by a million if one looks at the YoY numbers, but if one looks at the QoQ numbers, they have dropped by about a million.

Personally, I was expecting the GOV to grow a little bit more and the adjusted revenue to show around 25% growth YoY. And at the same time, I was hoping for the average monthly transacting customers to remain flat QoQ if not improve a little bit.

Source: Q4FY23 shareholder’s letter & results

Source: Q4FY23 shareholder’s letter & results

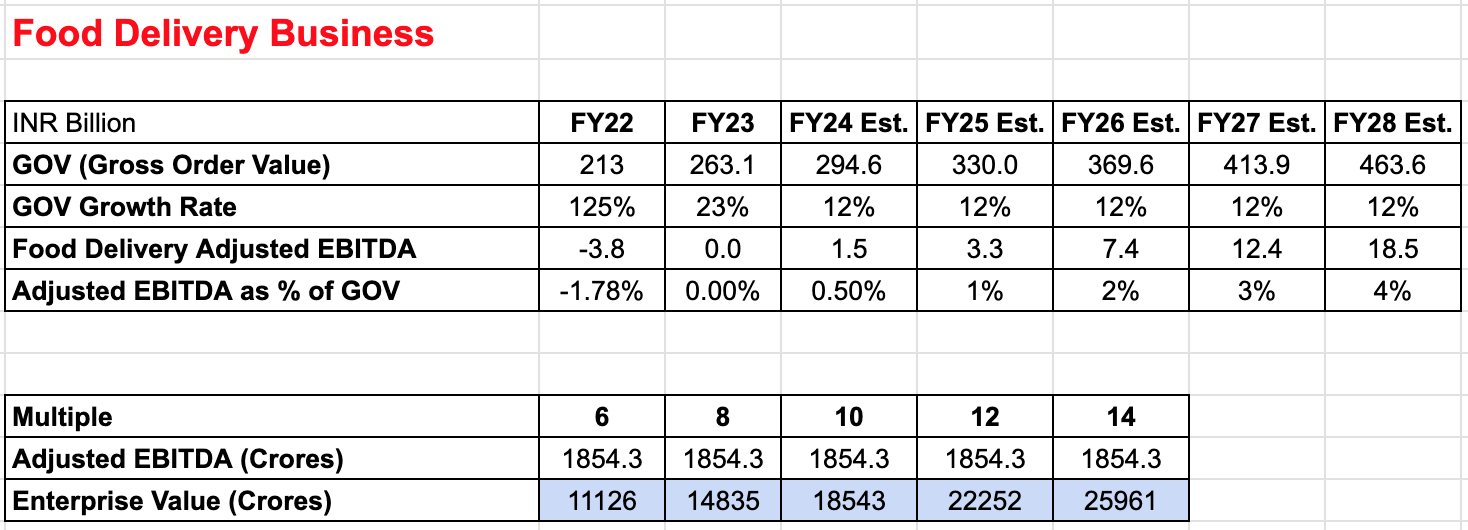

The table below shows Zomato’s FY19 to FY23 consolidated numbers for the food delivery business. The GOV has grown at a rate of 23.5% from FY22 to FY23 and the food delivery adjusted revenue has grown at a rate of 29%. And if you see my previous article, I had estimated FY23 GOV at 266.3 (INR Billion). Although I would have liked Zomato to come ahead of my estimates, I am not too dissatisfied with this. My main concern is with the GOV and adjusted revenue remaining almost flat for the last four quarters (Q1 to Q4 FY23).

Source: Author’s own tabulation based on FY21-22 Annual Report and Q4FY23 shareholder’s letter & results

One would assume that the focus on profitability is a major reason for this slowdown in growth. But that is not the case according to the management. Below is what the management said in its Q4FY23 earnings call:

And the point we’re trying to make here is that the improvement in profitability is not, therefore, coming at the cost of growth. That’s what we believe. And the efficiency and the improvement in margins has been on account of levers, which do not necessarily impact customer growth. So at least our view is that our improvement in profitability has a very, very little to no impact on what the growth would have been had we not had these changes.

This statement from management concerns me. Another statement that is of concern is quoted below:

So, as we’ve been saying over the last few quarters that we’ve been trying to look at all levers of efficiency in the business. The team has been executing well across the board and we just started to see a little bit of bounce back which is going to lead to a modest high single-digit growth in the current quarter sequentially, which is what we have indicated in our letter. What we’ll have to wait and watch is whether this momentum sustains beyond Q1, and that’s something we’ll have to wait and watch. At this point, we’ve shared whatever we could on what we’re seeing on the growth front in our letter

Looking at the above two statements, I was maybe too optimistic in my growth assumptions for this business.

Food Delivery Business Valuation

Looking at the Q4FY23 numbers and what the management said about the business going forward, if we estimate that the GOV will grow at a rate of between 12% for the next five years and the Adjusted EBITDA as a percentage of GOV will trend towards 4-5%, then we can arrive at an estimated Adjusted EBITDA of Rs. 1854 Crores in FY28. And if we are to apply a reasonable EV/Adj. EBITDA multiple of 8, we get an enterprise value of Rs. 14,835 Crores based on the FY28 estimated numbers.

Source: Author’s own estimates

Source: Author’s own estimates

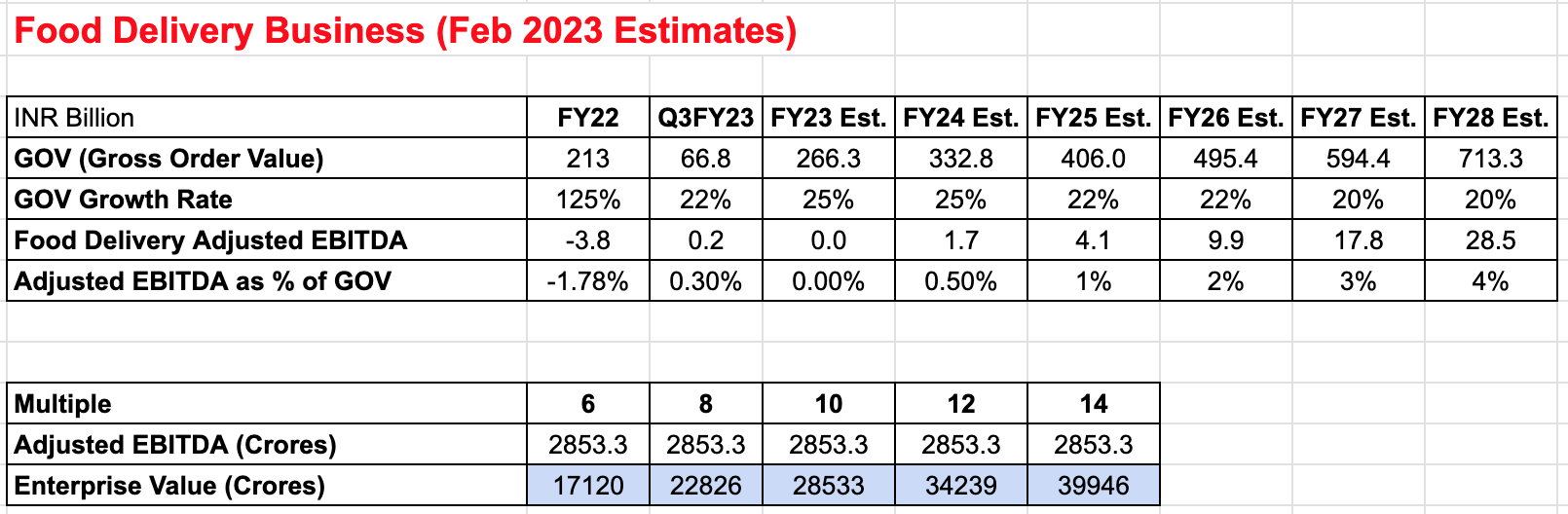

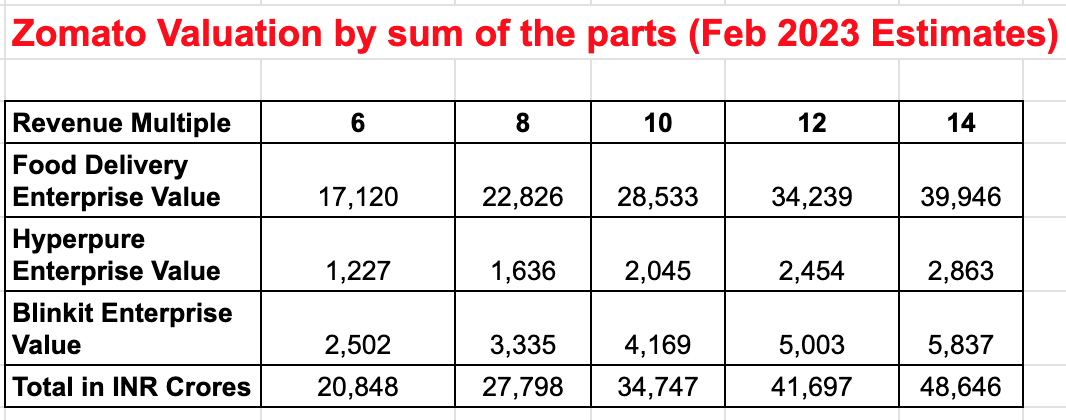

Below are my estimates from the previous article:

Source: Zomato: Is There Enough Juice Left At Current Valuation?

Source: Zomato: Is There Enough Juice Left At Current Valuation?

If we look at my previous and current estimates, there is a drop of almost 8,000 crores in enterprise value for Zomato’s food delivery business.

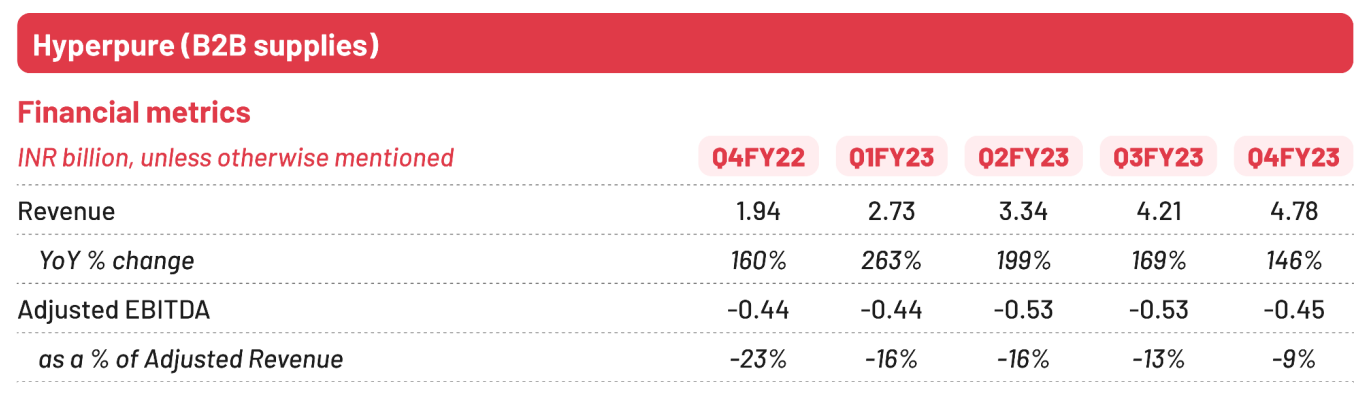

Zomato’s Hyperpure (B2B) Business

Looking at the Q4FY23 numbers, one can see that Hyperpure has continued its rapid growth while improving the adjusted EBITDA. In fact, I am impressed by the growth rate and the big improvement in the adjusted EBITDA margin.

Source: Q4FY23 shareholder’s letter & results

Source: Q4FY23 shareholder’s letter & results

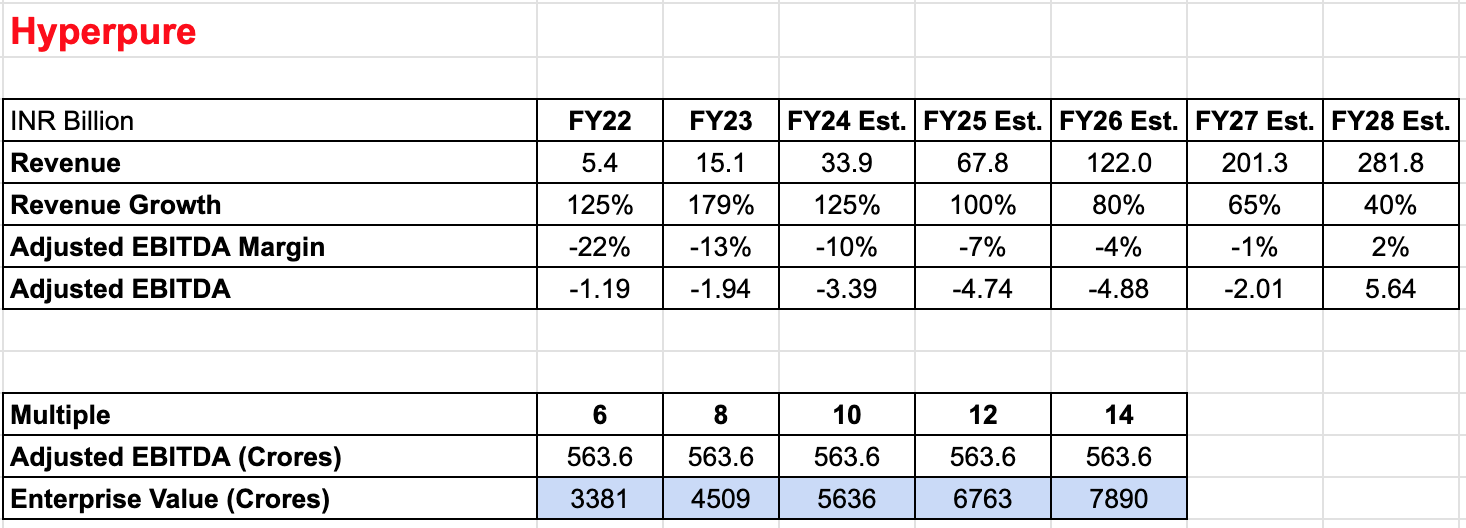

Based on the Q4FY23 & FY23 numbers if we estimate the revenue growth and adjusted EBITDA margin as shown in the table below, we get an estimated FY28 adjusted EBITDA of Rs. 563.6 Crores. And if we are to apply a reasonable EV/Adj. EBITDA multiple of 8, we get an enterprise value of Rs. 4,509 Crores based on the FY28 estimated numbers.

Source: Author’s own estimates

Source: Author’s own estimates

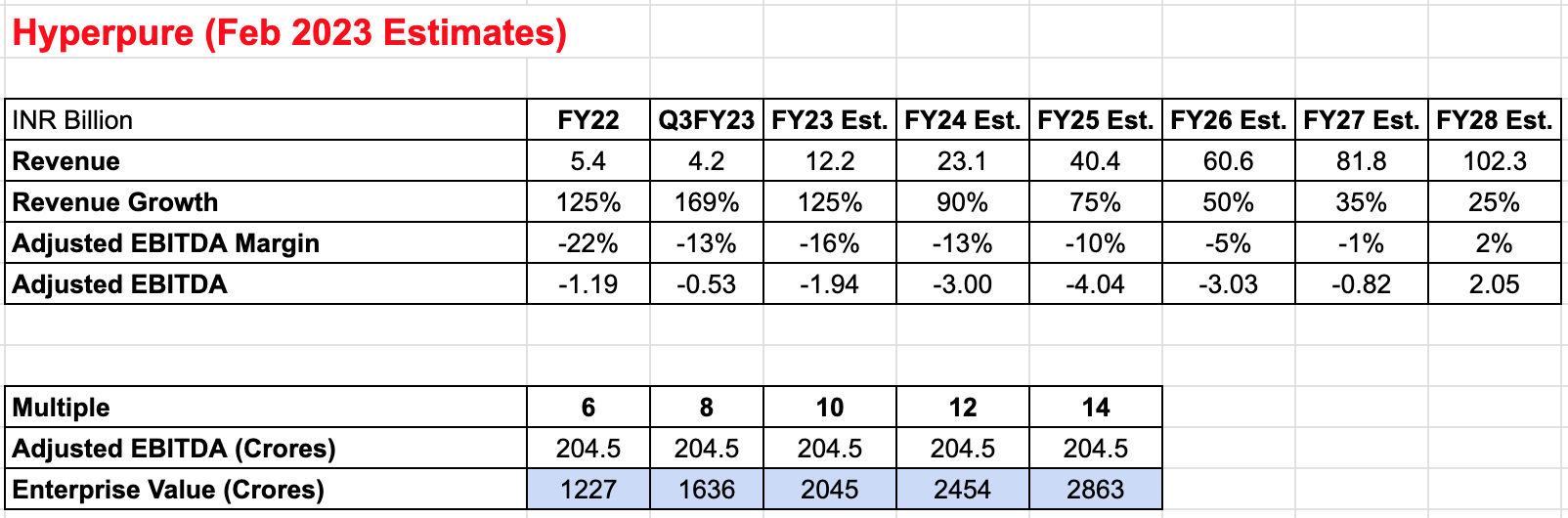

Below are my estimates from the previous article:

Source: Zomato: Is There Enough Juice Left At Current Valuation?

Source: Zomato: Is There Enough Juice Left At Current Valuation?

Comparing the two, Hyperpure’s enterprise value has increased by almost 3,000 crores based on my estimates. Hyperpure being a very young business that is growing at a very rapid rate, it is always tough to forecast too far out in the future. But one can be very happy with the progress that Hyperpure is making.

Blinkit

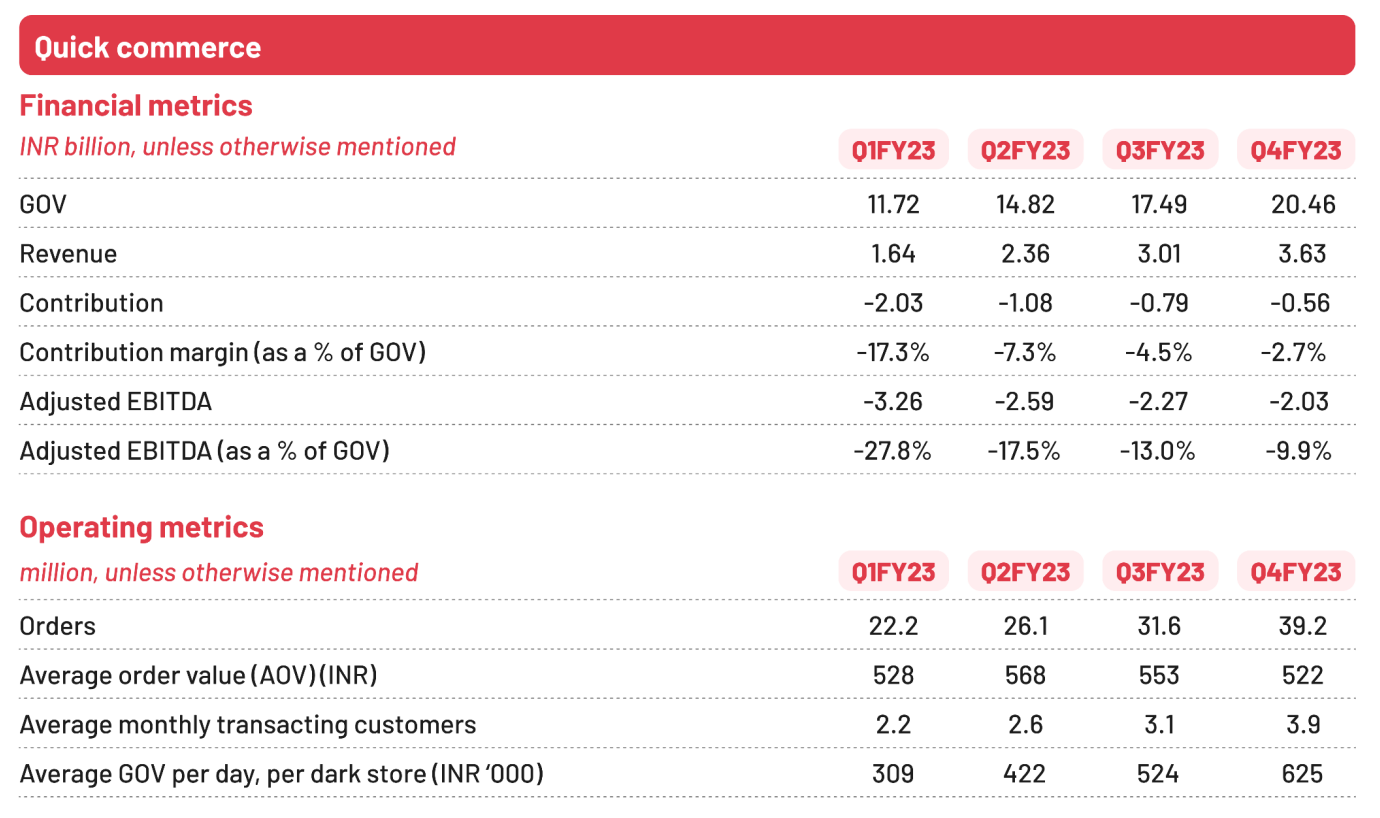

Blinkit’s growth rate and improvement in adjusted EBITDA margin are good. Revenue has grown by ~21% from 301 crores in Q3FY23 to 363 crores in Q4FY23. Also, the adjusted EBITDA margin has improved from -13% to -9.9%. The average GOV (gross order value) per day per dark store has grown at a rate of ~19% from Rs. 5,24,000 in Q3FY23 to Rs. 6,25,000 in Q4FY23.

Source: Q4FY23 shareholder’s letter & results

Source: Q4FY23 shareholder’s letter & results

As mentioned in the previous article, Blinkit is a business with high operating leverage. So, the EBITDA margins will improve exponentially as the AOV and GOV per day per dark store increase. This is due to the fact that a major portion of store costs are fixed in nature.

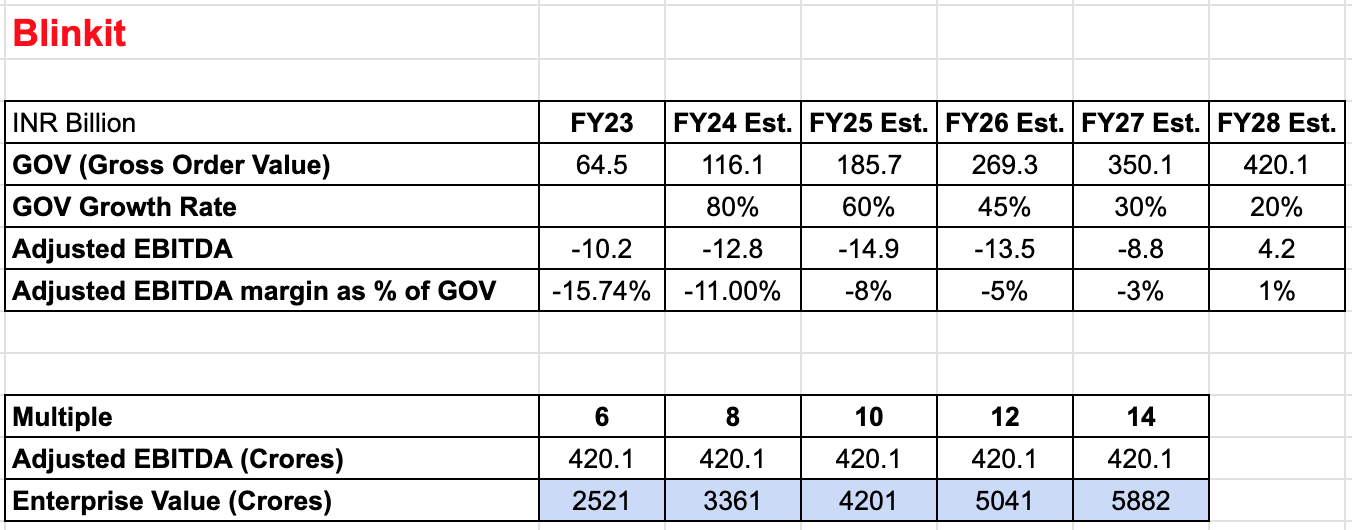

For the Blinkit business, not enough has changed. So, I am sticking with my previous assumptions of GOV growth and adjusted EBITDA margin as shown in the table below. This gives us an estimated FY28 adjusted EBITDA of Rs. 420.1 Crores. And if we are to apply a reasonable EV/Adj. EBITDA multiple of 8, we get an enterprise value of Rs. 3,361 Crores based on the FY28 estimated numbers.

Source: Author’s own estimates

Source: Author’s own estimates

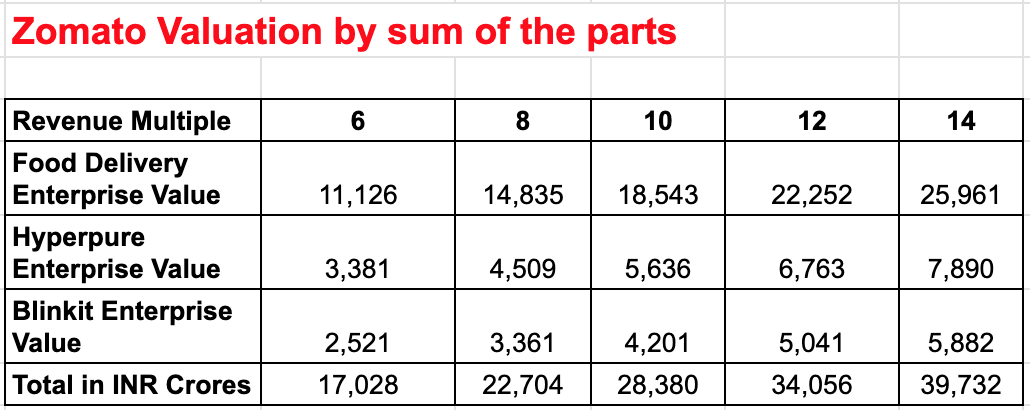

Zomato’s Valuation

Based on the valuation exercise that I have done above for the three businesses separately, we can arrive at a combined valuation of the company by adding the valuation of the three businesses. If I do the math, I arrive at an enterprise value of Rs. 22,704 Crores assuming an exit multiple of eight times FY28 estimated adjusted EBITDA.

Source: Author’s own estimates

Source: Author’s own estimates

Below is my previous estimate for Zomato. One can see that the slowdown in revenue growth for Zomato’s food delivery business in Q4FY23 has lowered the current valuation. I would say that perhaps, I was too optimistic when I did Zomato’s valuation in February 2023. However, the market and the wider investment community seem to disagree with me and are liking the Q4FY23 numbers better than I do and have in fact sent Zomato’s shares up by around 25% since the Q4FY23 results announcement.

Source: Zomato: Is There Enough Juice Left At Current Valuation?

Source: Zomato: Is There Enough Juice Left At Current Valuation?

Since Hyperpure & Blinkit are early-stage businesses, and the management is more focused on the growth of those businesses rather than profitability, the assumptions that I have made above for the growth rates and Adjusted EBITDA margin for those two businesses are extremely likely to be wrong.

If you are more pessimistic or optimistic about Zomato’s prospects, you can vary the growth rates, Adjusted EBITDA margins, and the exit multiples that you assign to arrive at a valuation that you think is right for Zomato.

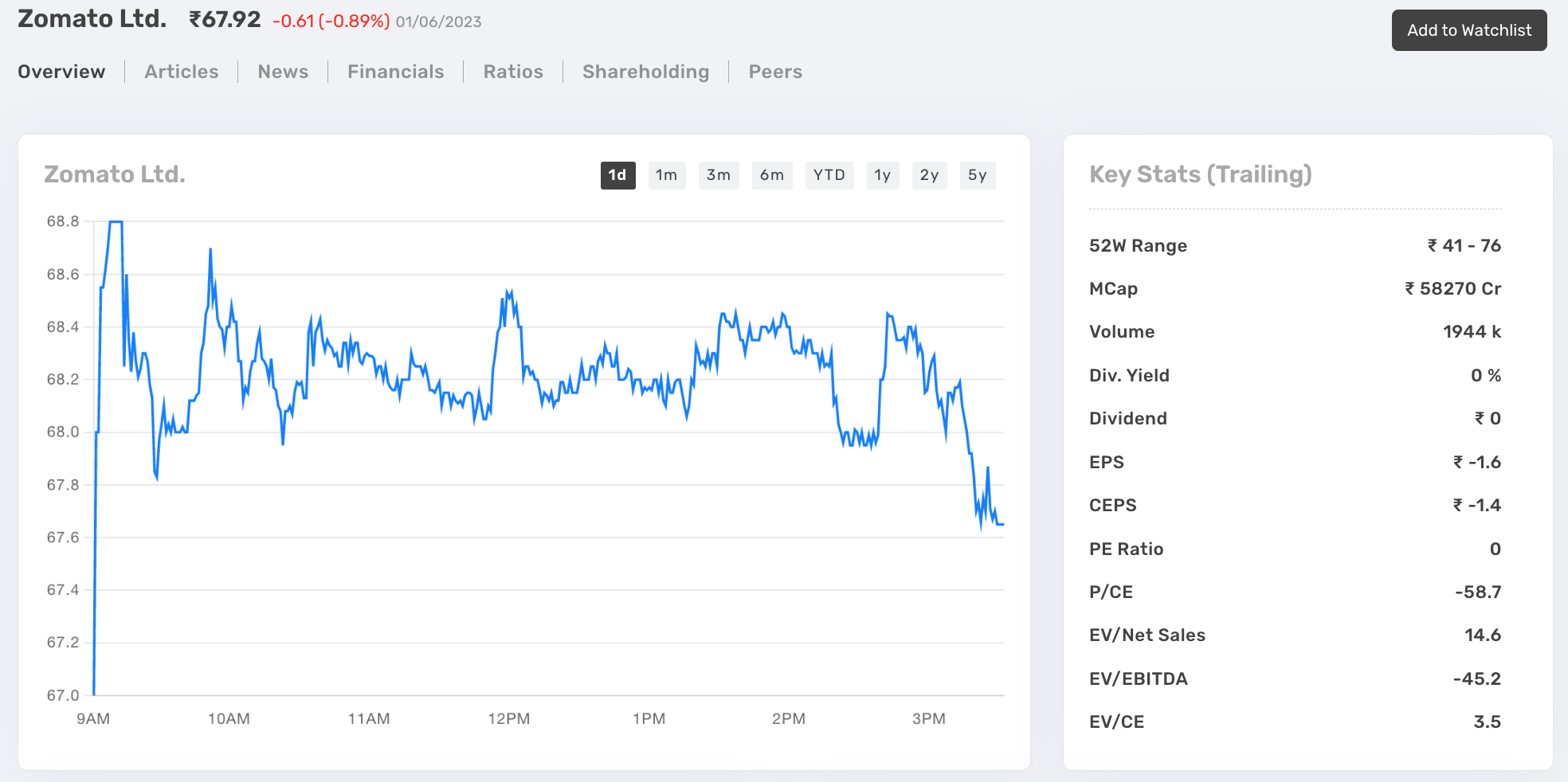

Zomato is currently trading at a Market Cap of around Rs. 58,000 crores.

Source: thryvv.in

Risks

- ONDC (open network for digital commerce) can put a lot of pressure on Zomato and Swiggy’s take rate from the restaurant and derails its profitability plans.

- ONDC could take away market share at the expense of Zomato and Swiggy.

- Zomato’s private competitor Swiggy could take away market share and delay Zomato’s path to profitability by engaging in price wars.

- Since I was not able to reliably estimate the share-based future payments and future rental costs, I have used Adjusted EBITDA in my calculations.

- I have assumed that over the medium to long term, there won’t be a significant difference between Zomato’s EBITDA & Adjusted EBITDA numbers. However, they could be meaningfully different and my use of Adjusted EBITDA numbers to arrive at an Enterprise value could look like an obvious error.

- Another major acquisition like Blinkit could divert the management’s focus and derail its path to profitability.

- Recent senior management exits are a cause of concern and need to be monitored.

I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

This article is for information and education purposes only. I wrote this article myself, and it expresses my own opinions. I have no business relationship with any company whose stock is mentioned in this article. The facts and opinions appearing in the article do not reflect the views of Thryvv Analytics Pvt. Ltd. and Thryvv Analytics Pvt. Ltd. does not assume any responsibility or liability for the same.

Disclosure: This article should not be taken as financial advice. Please consult your financial advisor before making any investment decision.