Zomato: Is there enough juice left at current valuation?

– While most users are aware of the restaurant food delivery business of Zomato, the other two Zomato businesses namely Hyperpure & Blinkit are also worth taking a look at.

– I introduce the three businesses of Zomato and try to value them individually as separate businesses.

– In the end, I value Zomato based on the sum of the three businesses and compare it to three global competitors.

Zomato Introduction

Zomato is one of the new-age startups from India that has been successful at scaling its operations, capturing significant market share, growing at a fast pace, and finally getting listed on NSE & BSE as a public company.

While most users are aware of the restaurant food delivery business of Zomato, the other two Zomato businesses namely Hyperpure & Blinkit are also worth taking a look at. There is one more business unit called “Feeding India” and that is an ESG (Environmental, Social, and Governance) initiative from Zomato.

The Indian restaurant food delivery market is mostly a duopoly between Zomato and Swiggy.

Zomato’s Food delivery business

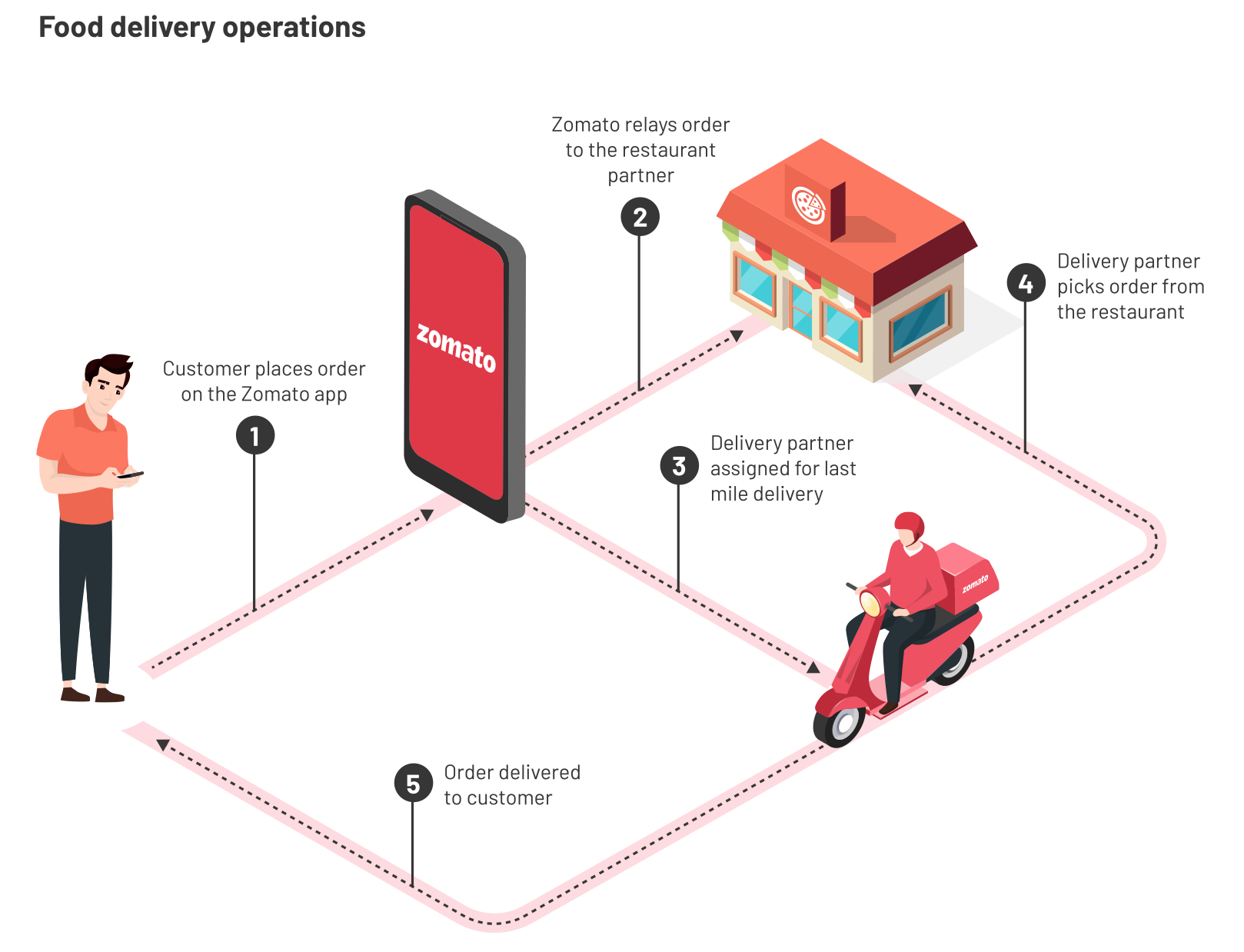

The below illustration taken from Zomato’s FY 2021-2022 Annual Report beautifully illustrates the workings of the food delivery business.

The Zomato app enables the customer to search for or discover restaurants & food items, allows him to place an order, automatically assigns a delivery partner who delivers the order to the customer’s desired location and collects payment via cash or online payment methods.

Zomato generates revenue from its restaurant partners via the commissions that they charge them for orders generated on the Zomato platform, and also from food delivery related advertising income.

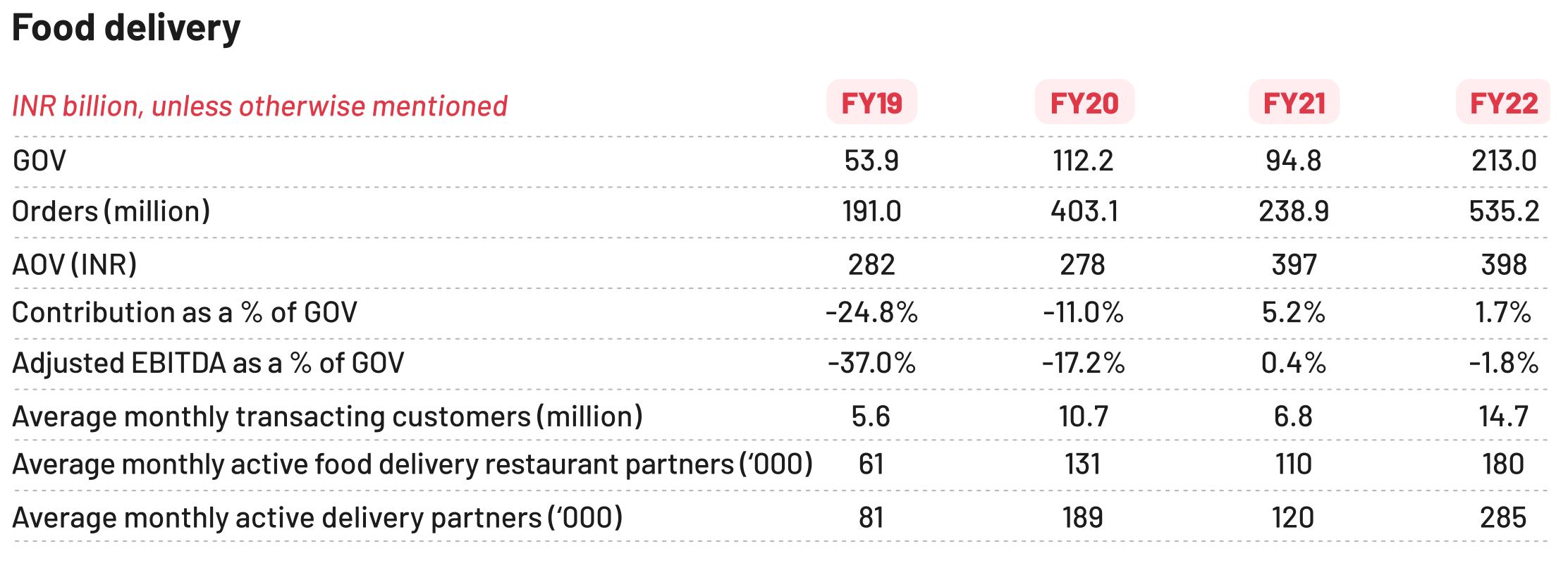

From FY2019 to FY2022, Zomato’s Food delivery business has grown its GOV (Gross Order Value) at a CAGR (Compounded annual growth rate) of around 41%, and the number of orders has multiplied by 2.8x in the same period. The AOV (Average order value) has also grown from Rs. 282 to Rs. 398 in the same period. Another point to note is the improvement seen in Adjusted EBITDA, which has improved from -37% to -1.8%.

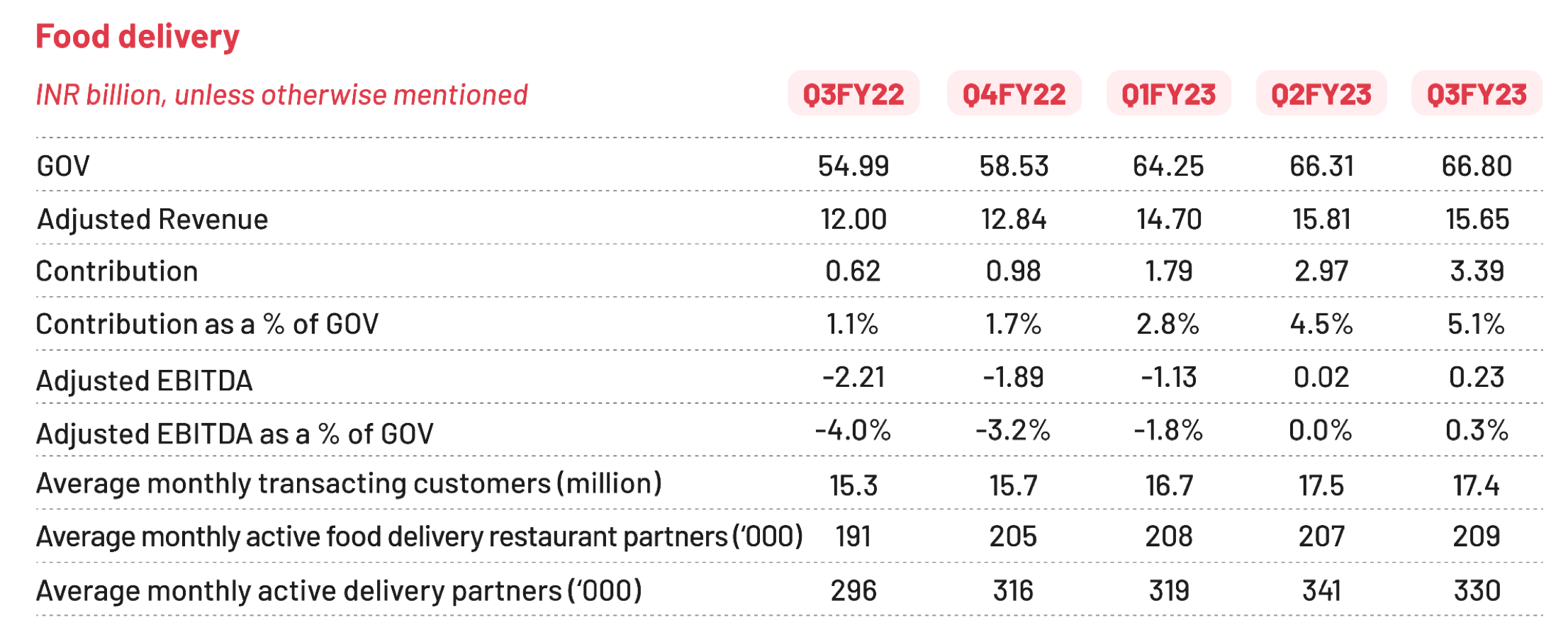

Looking at the quarterly numbers, one can see that the Adjusted EBITDA has improved from -4.0% in Q3FY22 to 0.3% in Q3FY23, and the YoY revenue growth has slowed down to 30%. One can interpret this as management letting go of low-quality growth in favor of better unit economics. And as per the Q3FY23 shareholder’s letter & results, the management is guiding towards a long-term Adjusted EBITDA margin of 4-5%.

Source: Q3FY23 shareholder’s letter & results

Food Delivery Business Valuation

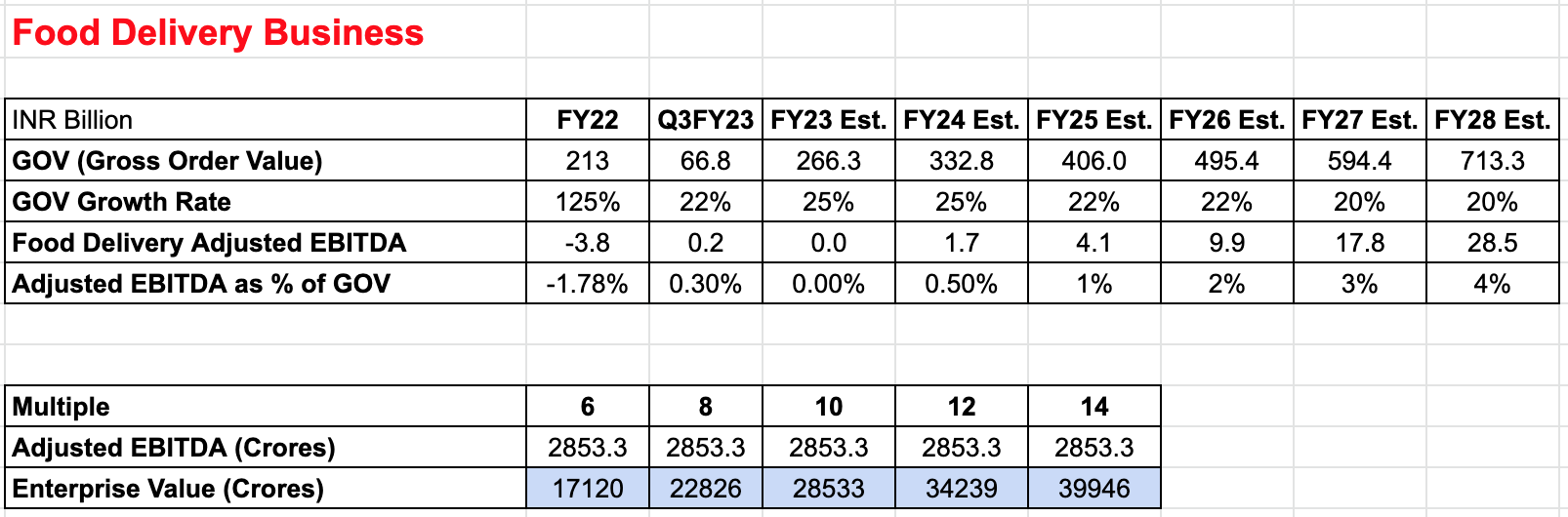

Based on what Zomato has been able to demonstrate for the food delivery business, if we estimate that the GOV will grow at a rate of between 20-25% for the next five years and the Adjusted EBITDA as a percentage of GOV will trend towards 4-5%, then we can arrive at an estimated Adjusted EBITDA of Rs. 2853 Crores in FY28. And if we are to apply a reasonable EV/Adj. EBITDA multiple of 8, we get an enterprise value of Rs. 22,826 Crores based on the FY28 estimated numbers.

Source: Author’s own estimates

Zomato’s Hyperpure (B2B) Business

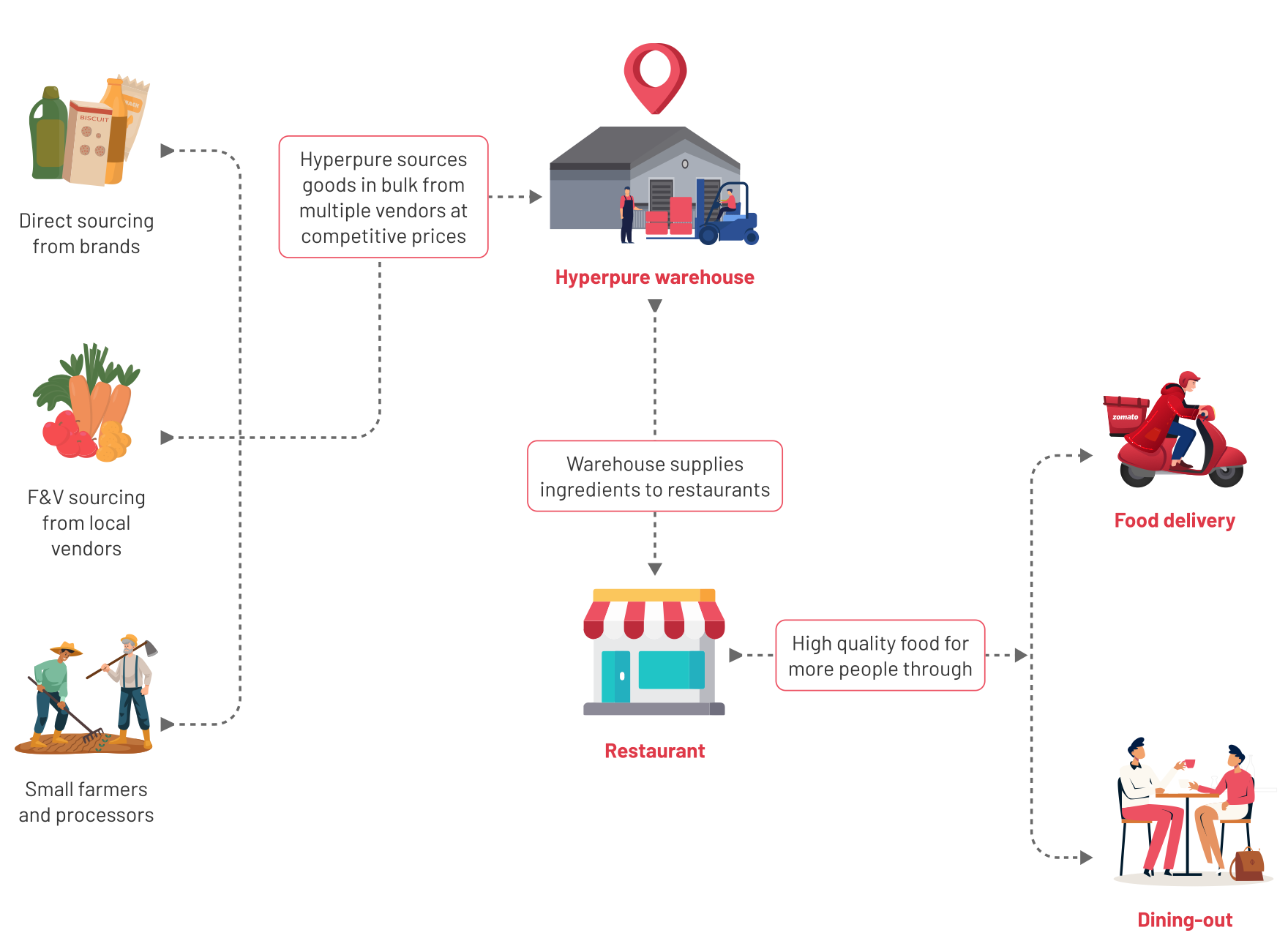

Hyperpure is Zomato’s restaurant supply business, where Hyperpure procures fruits, vegetables, flour, dairy, meat, packaged food, beverages, etc at scale and at competitive prices and supplies it to its restaurant partners. With Hyperpure, Zomato is able to increase its engagement with the restaurant partners and also improve the quality of ingredients used by the restaurants, which in turn benefits Zomato’s food delivery business gets repeat customers. Also, Hyperpure has an opportunity to supply to sellers who are selling on Blinkit (Zomato’s recent acquisition). Below is an illustration taken from Zomato’s FY 2021-2022 Annual Report which shows the functioning of Hyperpure.

Source: Zomato’s FY 2021-2022 Annual Report

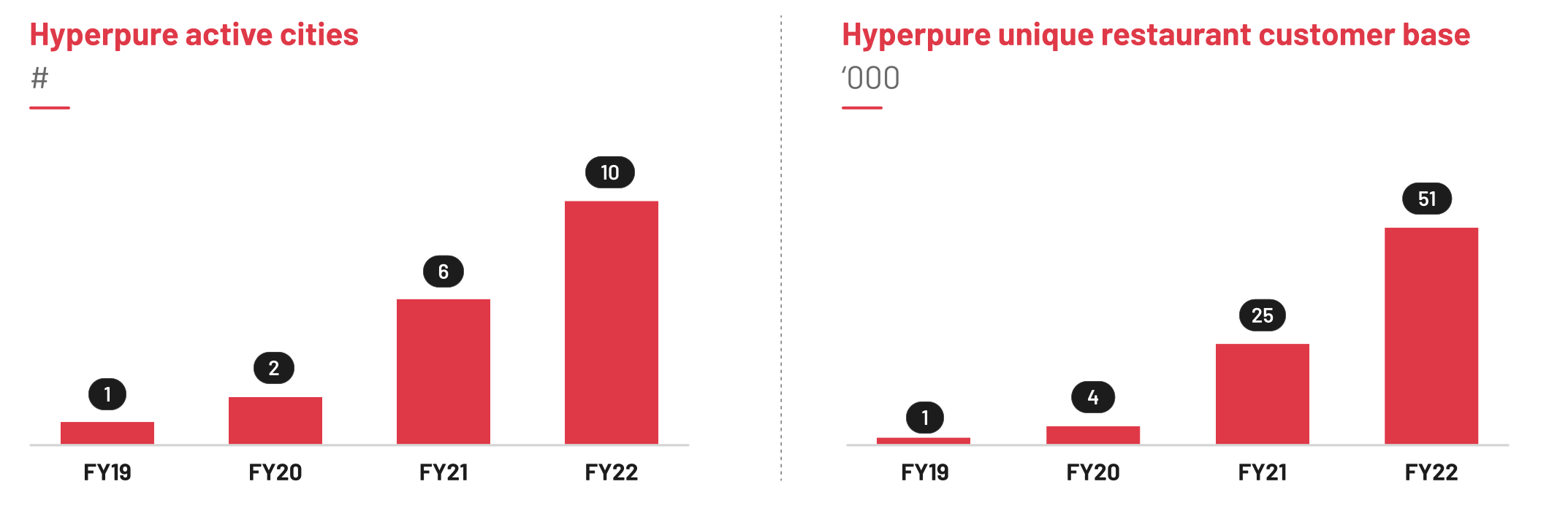

Hyperpure has been expanding very rapidly the number of cities that it serves and the number of restaurants that it supplies. The below chart shows the rapid growth that Hyperpure has been able to achieve.

Source: Zomato’s FY 2021-2022 Annual Report

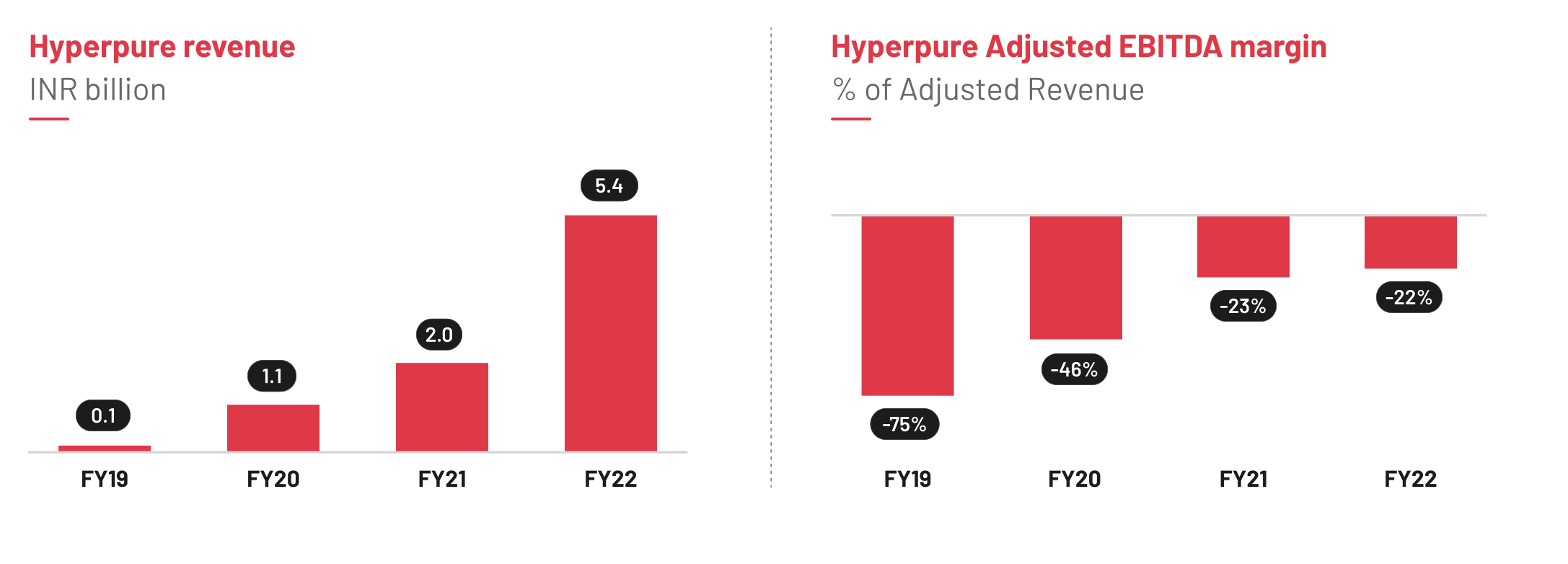

And this growth in cities and restaurants has resulted in equally rapid growth in Hyperpure revenue. And as expected with such a high-growth business, the Adjusted EBITDA margin is negative but it is improving.

Source: Zomato’s FY 2021-2022 Annual Report

Source: Zomato’s FY 2021-2022 Annual Report

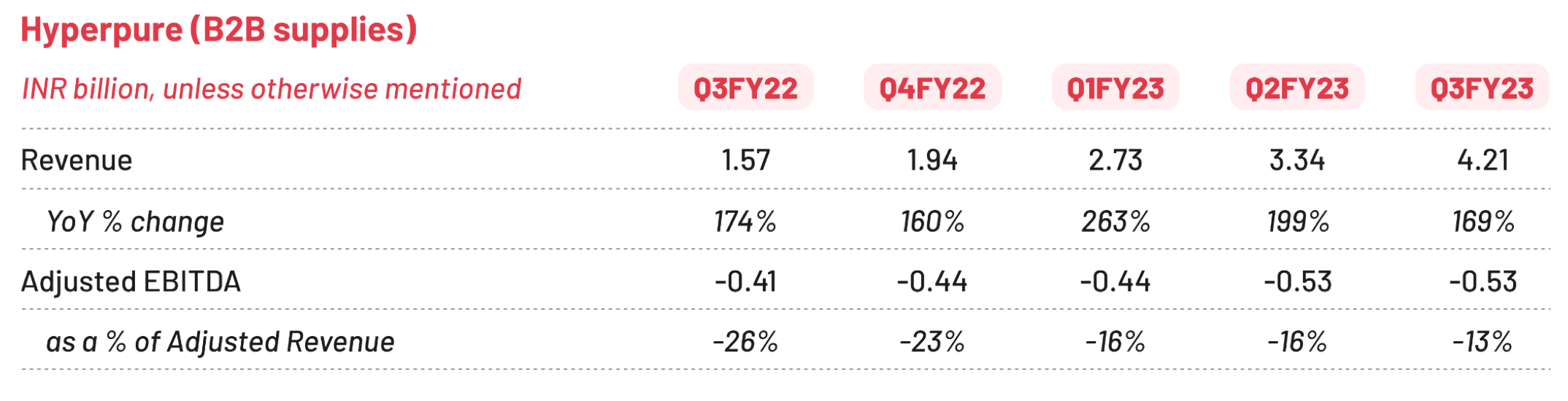

If we look at the last five quarters for Hyperpure, we can see that Hyperpure is still growing at a very rapid rate and is slowly improving the Adjusted EBITDA margin. And as the business scales, it can be expected that Hyperpure will turn EBITDA positive and start contributing positively to the overall Zomato bottom line.

Source: Q3FY23 shareholder’s letter & results

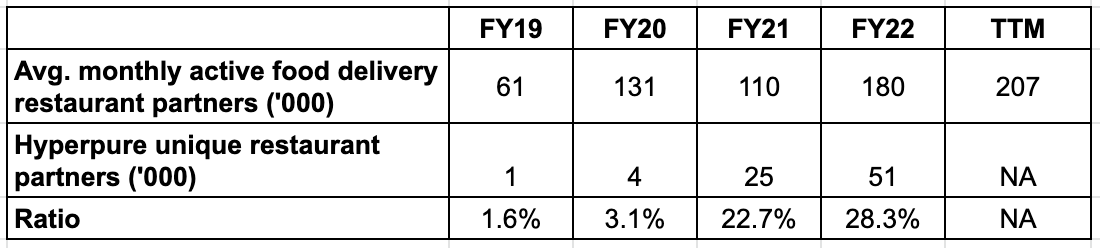

The table below shows the number of unique restaurants being served by Hyperpure.

Source: Author’s own work based on FY21-22 AR & Q3FY23 shareholder’s letter & results

As you can see, the number of unique restaurants being served by Hyperpure has increased from 1000 in FY19 to 51,000 in FY22. Also, if we look at the percentage of food delivery restaurant partners being served by Hyperpure, that number has also grown from a mere 1.6% in FY19 to 28% in FY22. One can conclude that the Hyperpure offering is beneficial to the restaurant partners and hence more and more restaurant partners are using them. Considering this, one can expect Hyperpure’s revenue to keep growing at a very high growth rate for a considerable amount of time. Also, according to the management,

Food and supplies cost is typically 25-30% of a restaurant’s revenue. Broadly speaking, that means that Hyperpure addressable market also is about 25-30% of restaurant food consumption in India. Even if we restrict our presence to the top 20 cities here, that translates into a very large addressable market.

Also, as we go along, Hyperpure could become a much larger business than just supplying to restaurants. As we expand into quick commerce, the capabilities we have built in Hyperpure will also come in handy. Hence, there is a long runway for growth here.

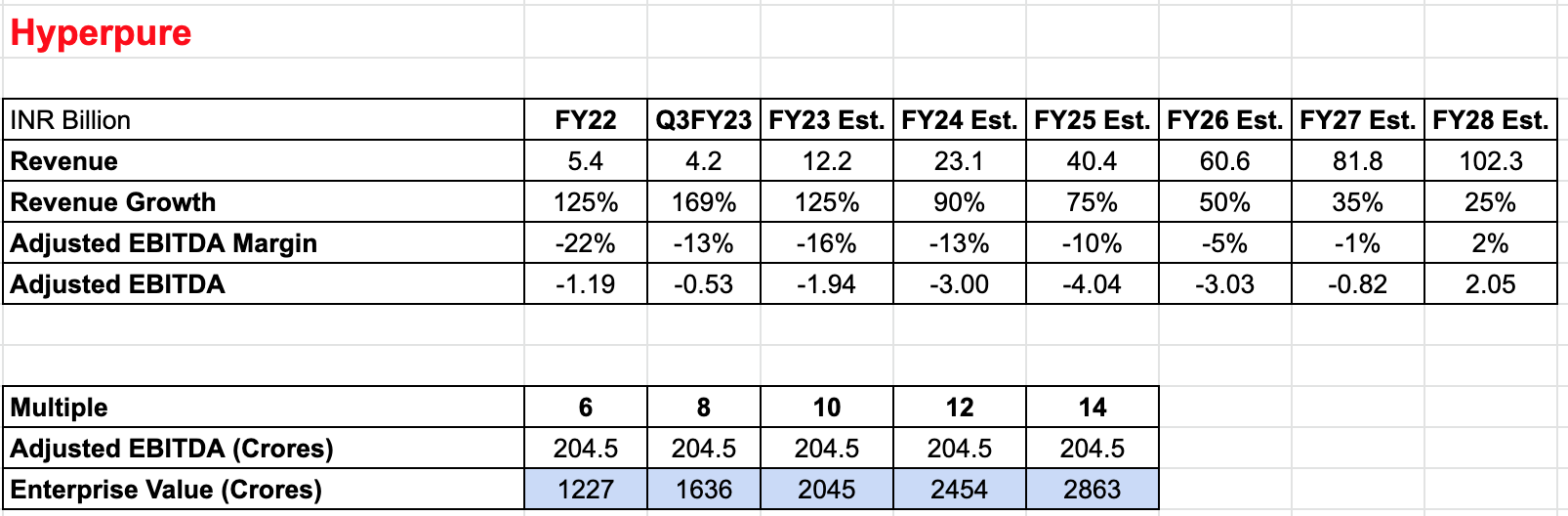

Based on this if we estimate the revenue growth and adjusted EBITDA margin as shown in the table below, we get an estimated FY28 adjusted EBITDA of Rs. 204.5 Crores. And if we are to apply a reasonable EV/Adj. EBITDA multiple of 8, we get an enterprise value of Rs. 1,636 Crores based on the FY28 estimated numbers.

Source: Author’s own work

Blinkit

Zomato entered the quick commerce space by acquiring Blinkit. Blinkit allows customers to shop for fruits, vegetables, dairy, meat, snacks, personal care items, pharma & wellness items, etc on its online platform and then delivers those items to the customers in a very short time, typically within 15-20 minutes.

According to the management, Blinkit’s opportunity is as big as its food delivery business. Below is an excerpt from Zomato’s Q1FY23 shareholders letter & results:

Quick commerce cuts across a wide range of essential spends including grocery, fruits and vegetables, beauty and personal care, OTC medicines, stationery items, among others. Therefore, we expect the overall customer base, average order value as well as monthly order frequency to be higher than food delivery (restaurant food in India is still regarded more as a discretionary spend).

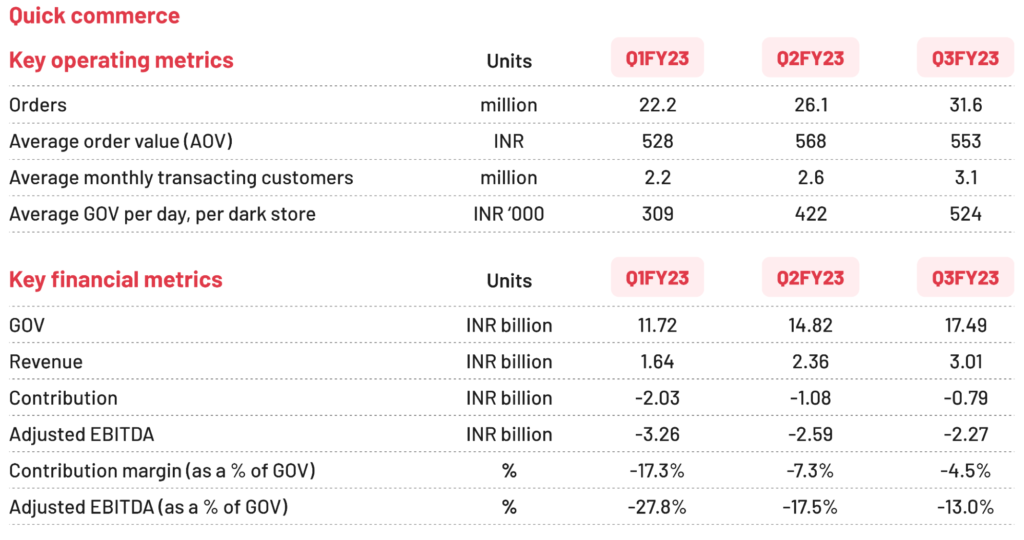

Looking at the key operational & financial metrics of Blinkit, one can see that the revenue has grown by ~28% from 236 crores in Q2FY23 to 301 crores in Q3FY23. Also, the adjusted EBITDA margin has improved from -17% to -13%. The average GOV (gross order value) per day per dark store has grown at a rate of ~24% from Rs. 4,22,000 in Q2FY23 to Rs. 5,24,000 in Q3FY23.

Source: Q3FY23 shareholder’s letter & results

Now the question arises that how can Blinkit reach EBITDA breakeven or turn EBITDA positive. For Blinkit, the answer lies in increasing the AOV (average order value) & GOV per store. Since a big portion of the dark store operating costs are fixed, any additional increase in AOV & GOV per store exponentially improves the EBITDA margin. In other terms, Blinkit is what one would call a “high operating leverage” business.

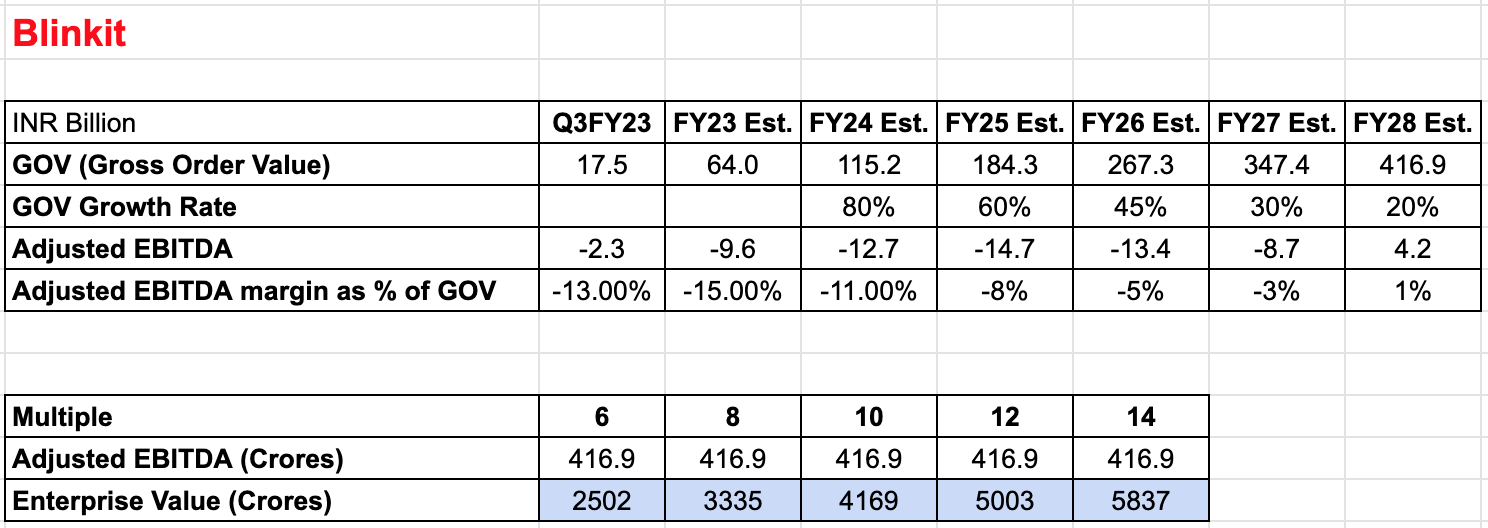

Based on the growth rates and the improvements that we have seen in the last two quarters for Blinkit, if we estimate the GOV growth and adjusted EBITDA margin as shown in the table below, we get an estimated FY28 adjusted EBITDA of Rs. 416.9 Crores. And if we are to apply a reasonable EV/Adj. EBITDA multiple of 8, we get an enterprise value of Rs. 3,335 Crores based on the FY28 estimated numbers.

Source: Author’s own work

Zomato’s Valuation

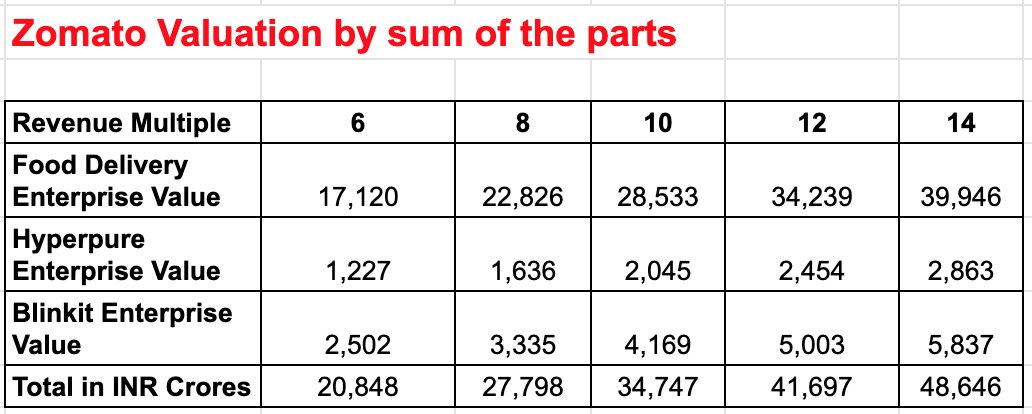

Based on the valuation exercise that I have done above for the three businesses separately, we can arrive at a combined valuation of the company by adding the valuation of the three businesses. If I do the math, I arrive at an enterprise value of Rs. 27,798 Crores assuming an exit multiple of eight times FY28 estimated adjusted EBITDA.

Source: Author’s own work

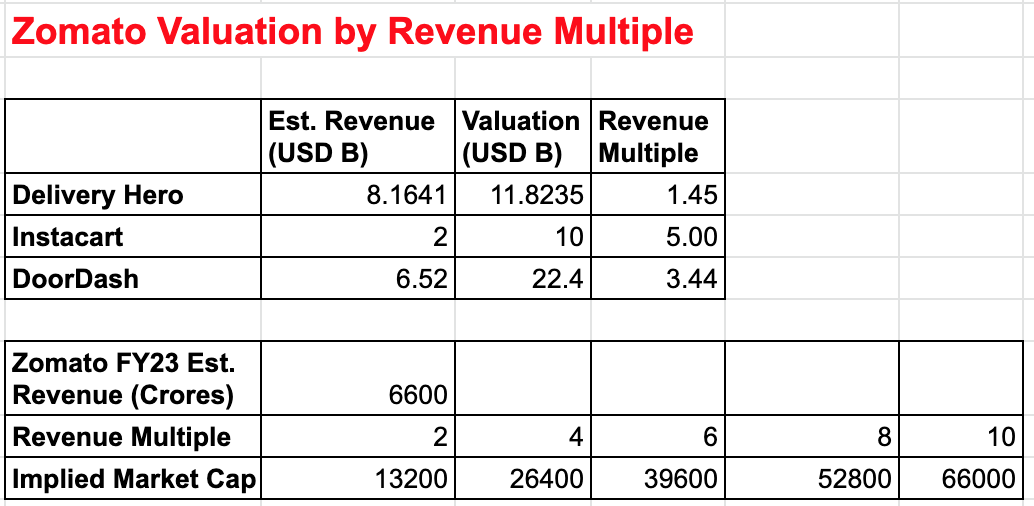

Since Hyperpure & Blinkit are early-stage businesses, and the management is more focused on the growth of those businesses rather than profitability, the assumptions that I have made above for the growth rates and Adjusted EBITDA margin for those two businesses are extremely likely to be wrong. So, another way to value the Zomato business is by assigning it a revenue multiple based on what other global competitors are currently valued at. In order to arrive at the right revenue multiple for Zomato, I have looked at three global competitors’ revenue, public valuation, and growth rates. Zomato has a huge potential market to tap into (India) and it is growing at a decent rate. If I convert Zomato’s FY23 estimated revenue of INR 6,600 Crores to USD (assuming 1 INR = 80 USD), I get Zomato’s FY23 estimated revenue as $0.825 Billion. And based on the size of the other three global competitors, one can see that Zomato is growing from a relatively small revenue base number and has a long runway to grow. So, I have assigned a revenue multiple of 6 to arrive at a Rs. 39,600 Crores valuation for Zomato.

Source: Author’s own work, Delivery Hero, DoorDash, Instacart

If you are more pessimistic or optimistic about Zomato’s prospects, you can vary the growth rates, Adjusted EBITDA margins, and the exit multiples that you assign to arrive at a valuation that you think is right for Zomato.

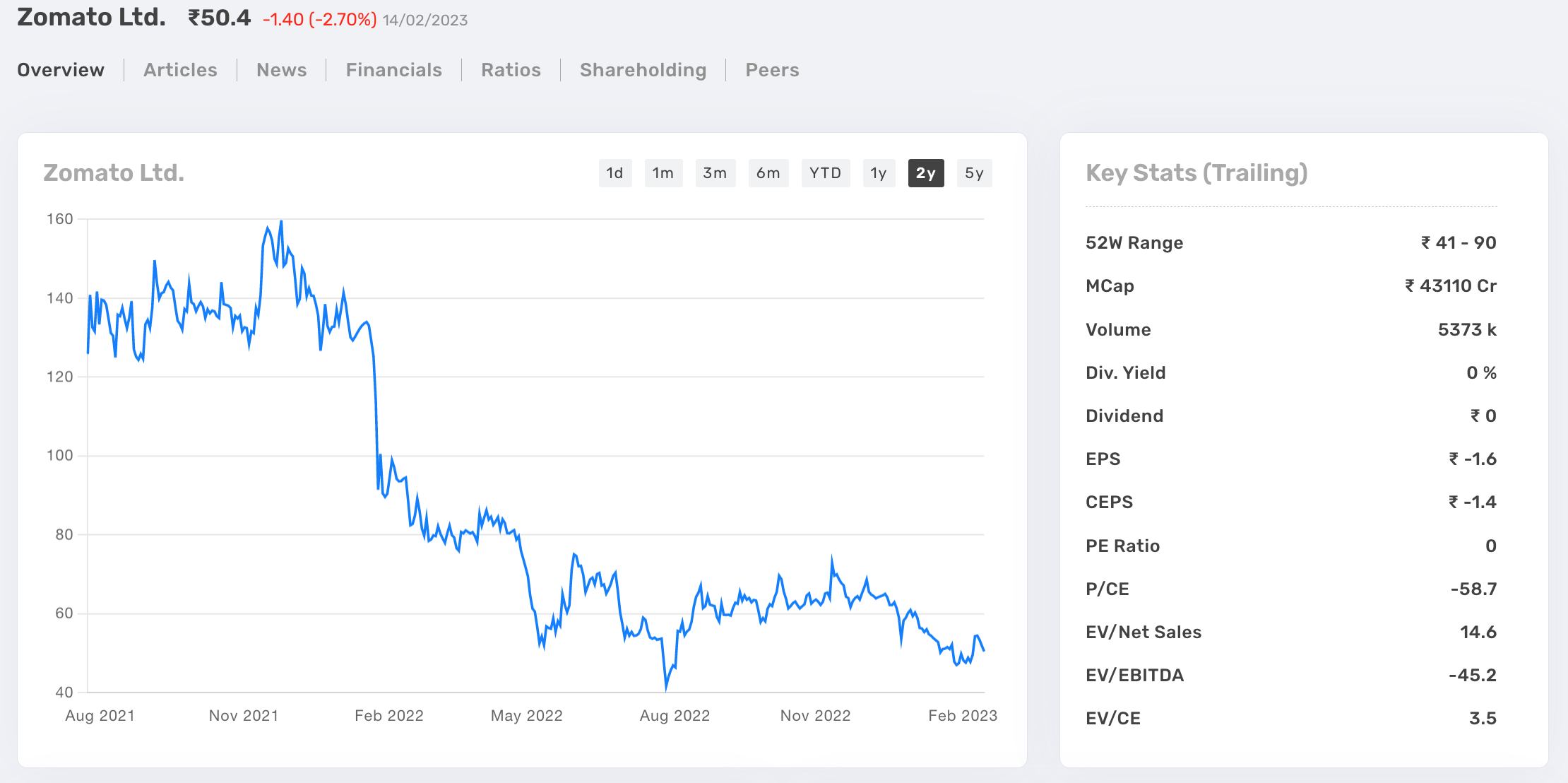

Zomato is currently trading at a Market Cap of around Rs. 43,000 crores.

Source: thryvv.in

Zomato’s other initiatives

Recently, Zomato has introduced “Zomato Gold” in place of the older loyalty program that was discontinued. Below is what the management said about Zomato Gold in its Q3FY23 shareholders’ letter & results:

The key highlight of Zomato Gold is ‘On Time Guarantee’. This feature was three years in the making, and the tech which powers this feature is a significant achievement for our team. Gold members also get priority access to more restaurants during peak times and offers from a number of restaurants on both delivery and dining-out. We have also made our intercity delivery from legendary restaurants (called Intercity Legends) exclusively available to Gold members. And of course, free delivery on orders meeting certain criteria.

In less than a month, the Zomato Gold program has scaled to 900k+ members.

“Intercity Legends” as the name suggests is a service of delivering food from legendary (popular/well-known) restaurants across cities.

Another upcoming initiative that looks promising is called “Zomato Everyday”. This service is geared towards customers that are looking for home-style cooked meals at affordable prices. Zomato believes that there is a large addressable market for such a service and it is an untapped market.

Risks

- Zomato’s private competitor Swiggy could take away market share and delay Zomato’s path to profitability by engaging in price wars.

- Since I was not able to reliably estimate the share-based future payments and future rental costs, I have used Adjusted EBITDA in my calculations.

- I have assumed that over the medium to long term, there won’t be a significant difference between Zomato’s EBITDA & Adjusted EBITDA numbers. However, they could be meaningfully different and my use of Adjusted EBITDA numbers to arrive at an Enterprise value could look like an obvious error.

- Another major acquisition like Blinkit could divert the management’s focus and derail its path to profitability.

- Recent senior management exits are a cause of concern and need to be monitored.

I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

This article is for information and education purposes only. I wrote this article myself, and it expresses my own opinions. I have no business relationship with any company whose stock is mentioned in this article. The facts and opinions appearing in the article do not reflect the views of Thryvv Analytics Pvt. Ltd. and Thryvv Analytics Pvt. Ltd. does not assume any responsibility or liability for the same.

Disclosure: This article should not be taken as financial advice. Please consult your financial advisor before making any investment decision.