Zen Technologies Ltd.: Review after Q1FY25 Results

– Zen Technologies Ltd. is a pioneer in defence training solutions and anti-drone solutions.

– Zen Technologies recently launched four new products: Hawkeye, Barbarik – URCWS, Prahasta, and Sthir Stab 640.

– The company currently trades at a TTM P/E ratio of more than 89.

– The company boasts of an order book of Rs. 1158 Crores while its FY24 revenues were Rs. 442 Crores.

This is a follow-up article to my previous article on Zen Technologies Ltd which was shared when Zen stock was around Rs. 840. (https://www.thryvv.in/article/zen-technologies-ltd-a-defence-company-worth-looking-at/)

I will discuss the new developments in this article, review the latest Q1FY25 results, and provide an update on the valuation.

New Developments

In February 2024, Zen Technologies announced that it would acquire a 51% stake in AiTuring Technologies for a total consideration of approximately Rs 3.87 crore.

With the help of that recent acquisition, Zen has launched four new products.

- Hawkeye is a state-of-the-art anti-drone system camera, featuring multiple sensor detection modules for all-weather drone tracking up to 15 km. It ensures continuous threat detection and enhanced security. Here is a link to the product page.

- Barbarik – URCWS is the world’s lightest remote-controlled weapon station, offering precise targeting capabilities (5.56mm to 7.62mm calibers) for ground vehicles and naval vessels, maximizing battlefield effectiveness while minimizing personnel risk. The URCWS has undergone recent firing trials at Infantry School Mhow and Armoured School Ahmednagar and performed well.

- Prahasta is a revolutionary automated quadruped that uses LIDAR and reinforcement learning to understand and create real-time 3D terrain mapping for unparalleled mission planning, navigation, and threat assessment. The quadruped can be armed with various caliber weapons such as 9mm, 5.56mm, and 7.62mm. The quadruped can be used as the first line of defense for commandos during CI operations like 26/11, thereby saving lives.

- Sthir Stab 640 is a rugged stabilized sight designed mainly for armored vehicles, ICVs, and boats. The sight encompasses an intelligent fiber optic gyro-stabilized system and delivers exceptional situational awareness with automatic search and tracking capabilities. The sight can be used in different weapon mounts such as 7.62mm, 12.7mm, 20mm, and 30mm. Here is a link to the product page.

These products if well received can become an additional revenue stream for the company going forward.

Q1FY25

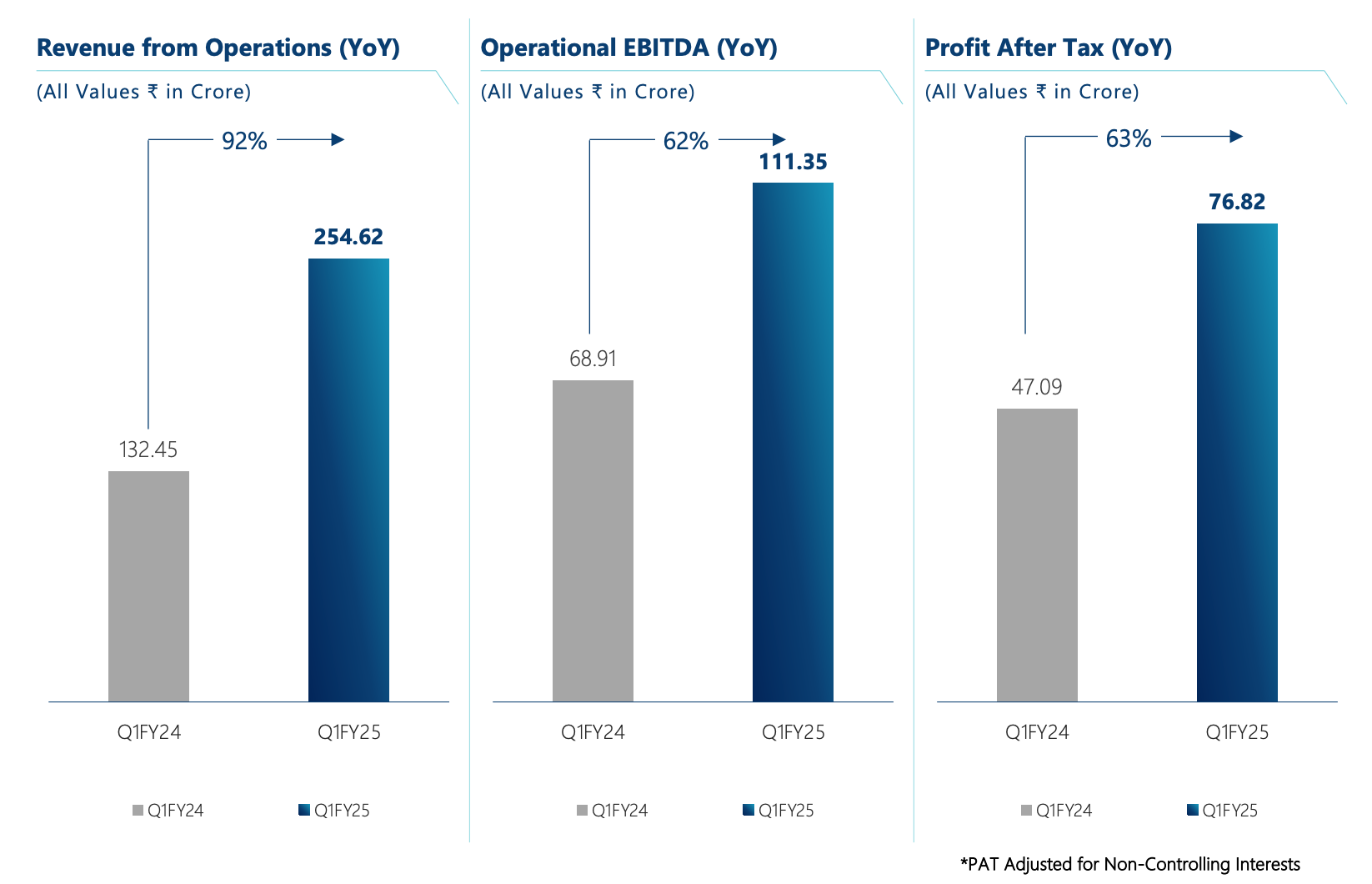

Zen Technologies Limited had an exceptionally strong start to FY25. Revenue from operations for Q1FY25 came in at Rs. 254.62 crores, which represents a YoY growth of 92%. Operational EBITDA came in at Rs. 111.35 crores, and the net profit came in at Rs. 76.82 crores, recording an EBITDA growth of 62% and PAT growth of 63% year-on-year respectively. Here is the link to the company presentation.

Source: Q1FY25 Investor Presentation

Source: Q1FY25 Investor Presentation

Notes from Q1FY25 Conference Call

The company had an order book of Rs. 1158 Crore as of June 30th, 2024. The company is anticipating more orders in the upcoming quarters, especially Q4. Mr. Ashok Atluri (Chairman & MD) explained that in their industry majority of the big orders usually materialize in Q4.

The management is confident of reaching the Rs. 900 Crore FY25 revenue target. The company is expected to reach Rs. 2000 Crore revenue in FY27. The management has guided for a 35% EBITDA (Earnings Before Interest Tax Depreciation & Amortization) and 25% PAT (Profit After Tax) margins for the long term.

The management said that the market for ADS (Anti Drone Systems) is around 10,000 Crores for the next 3-5 years. And the management is expecting that this might be a conservative estimate. Mr Ashok Atluri mentioned that ADS has been categorized as IDDM (Indigenously Designed, Developed, and Manufactured). Mr. Ashok said that as far as he remembers, there are only two companies that meet the IDDM criteria, Zen Technologies and BHEL.

The recently launched new products will likely start contributing to the top line sometime in the next year. The management expects that these “Sight & Surveillance” products will become a separate revenue stream in the long term. More product launches are planned in the near future.

Mr. Ashok Atluri said that the former chief of army staff Mr. Manoj Pande had mentioned that training and simulator orders are just getting started. So the company is expecting an increasing demand going forward.

Here is the link to the Q1FY25 conference call. If you have time, do watch it. There is a cool demo of the four new products that the company launched.

Valuation

If I take the current price of the company as Rs. 1700 and use the TTM EPS of Rs. 19, then I get a TTM P/E ratio of around 89.

If I take FY27 guidance of Rs. 2000 Crores topline and 25% PAT margin, I get Rs. 500 Crore PAT which may be roughly Rs. 55 EPS. If I use these numbers and the current price as Rs. 1700, I get an FY27 P/E ratio of around 31.

And for a company growing at around 50%, how much would one be willing to pay in 2027 ? If I assume a 35, 50, and 70 multiple of the Rs. 55 EPS, I get an exit price of Rs. 1925, Rs. 2750, and Rs. 3850 in FY27.

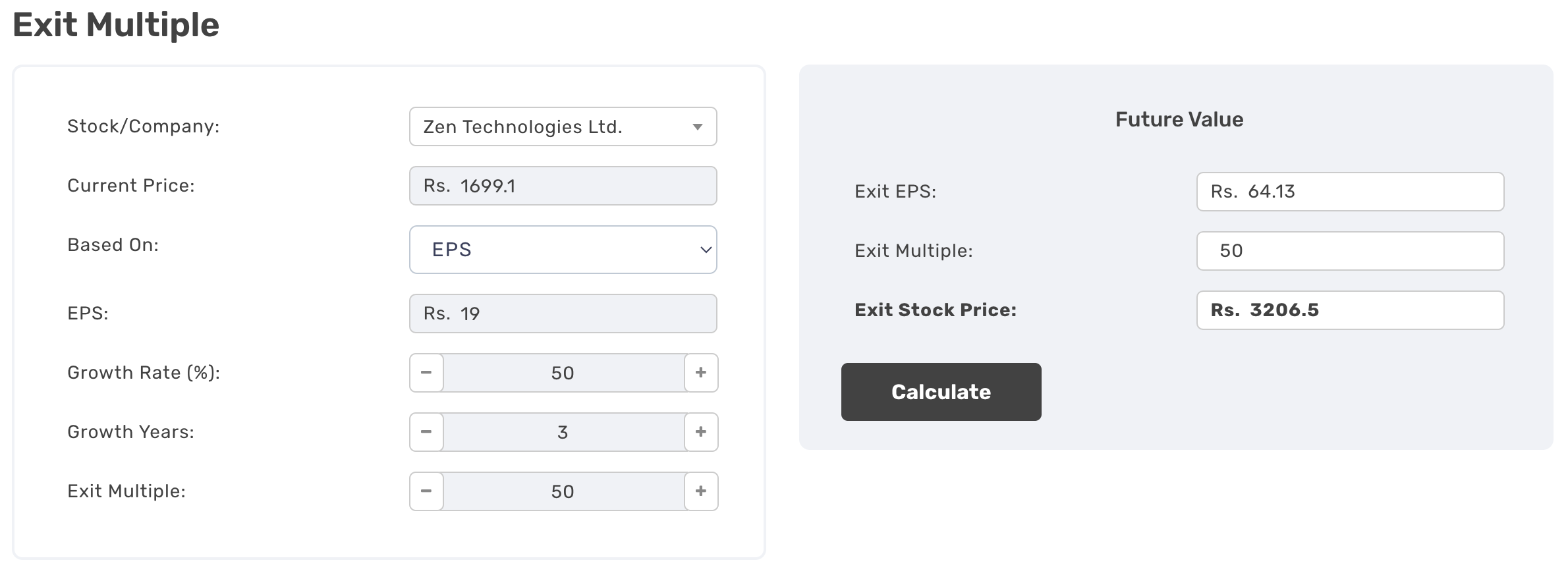

If I use the TTM EPS of Rs. 19, exit multiple of 50, and a growth rate of 50% for the next three years (since the management has guided towards that number), I get an exit price after 3 years of Rs. 3206.5.

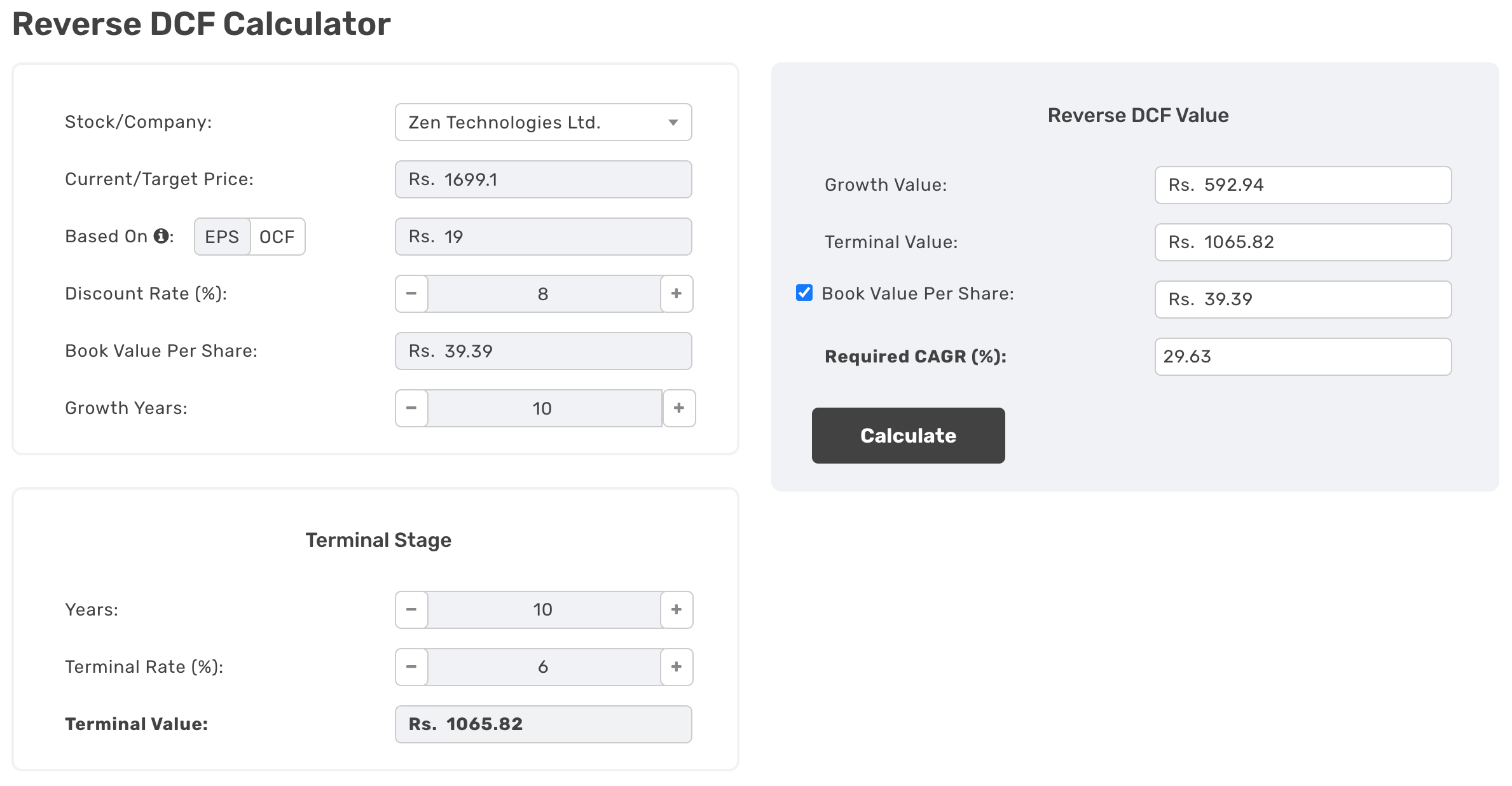

And if I use the Reverse DCF calculator, with inputs as shown in the below picture, I get a required CAGR of 29.63%, which seems high. For a company to grow its EPS at that rate for 10 years is not an easy task. (When we use a DCF or Reverse DCF calculator, we are assuming a short finite life of the company, in this case, we have assumed the life of the company as 20 years (10 years of growth and 10 years of terminal stage)).

Whether Exit Multiple or the Reverse DCF method is the right way to value the company, I leave that in your hands. And the output number could be a lot different if you assume different numbers than what I have assumed. You could be a lot more optimistic or pessimistic about the company than I am and that is why valuation is a personal judgement call. Feel free to explore the Reverse DCF (https://www.thryvv.in/reverse-dcf-calculator/) and the Exit Multiple calculators (https://www.thryvv.in/exit-multiple/) that are available on this website.

Risks

- Future order flows not materializing as per the management’s expectations could derail the growth story.

- A change in the government at the center (Indian Government) could also impact future order flows significantly.

- Operations and profit margins might be at risk due to escalating competition and aggressive pricing strategies by international competitors. These firms may significantly drop their prices to secure a larger market share in India.

- Unfavorable macroeconomic conditions could pose a risk to the company. In such circumstances, governments may shift their focus to immediate concerns and possibly deprioritize defense spending.

- Much of the simulator production is based on specific client feedback, with no guaranteed purchase of the end product. This scenario places the company at a substantial financial risk.

- The standard governmental policy of procurement from the lowest bidder could pose a threat to the Company. Occasionally, other vendors, having already amortized their development costs, can offer cheaper solutions due to their larger capacity.

- Zen Technologies heavily relies on the Indian Government for a significant part of its business, whether it’s policy-driven or on actual product sales.

I/we are long Zen Technologies Ltd.

This article is for information and education purposes only. I wrote this article myself, and it expresses my own opinions. I have no business relationship with any company whose stock is mentioned in this article. The facts and opinions appearing in the article do not reflect the views of Thryvv Analytics Pvt. Ltd. and Thryvv Analytics Pvt. Ltd. does not assume any responsibility or liability for the same.