Zen Technologies Ltd.: A Defence Company Worth Looking At

– Zen Technologies Ltd. is a pioneer in defence training solutions and anti-drone solutions.

– The company works on an asset-light model where most of the operations are outsourced and high-value functions like R&D, Engineering, Marketing, Sales, and After-Sales Services are kept in-house.

– The company currently trades at a TTM P/E ratio of more than 60.

– The company boasts of an order book of Rs. 1434 Crores while its FY23 revenues were Rs. 219 Crores.

About the Company

Zen Technologies Ltd. is a pioneer in defence training solutions and anti-drone solutions.

From land-based military training simulators and driving simulators to live range equipment and anti-drone systems, the solutions provided by Zen Technologies Ltd. are unmatched in measuring combat readiness and creating realistic battle experiences. Their proprietary training platform integrates the entire range of products.

The company’s product portfolio consists of the following:

- Anti-drone solutions

- Live Ranges

- Live Simulation and Virtual Simulation

- Combat Training Center

FY23 Annual Report lists all the products that the company offers in detail. It is very informative.

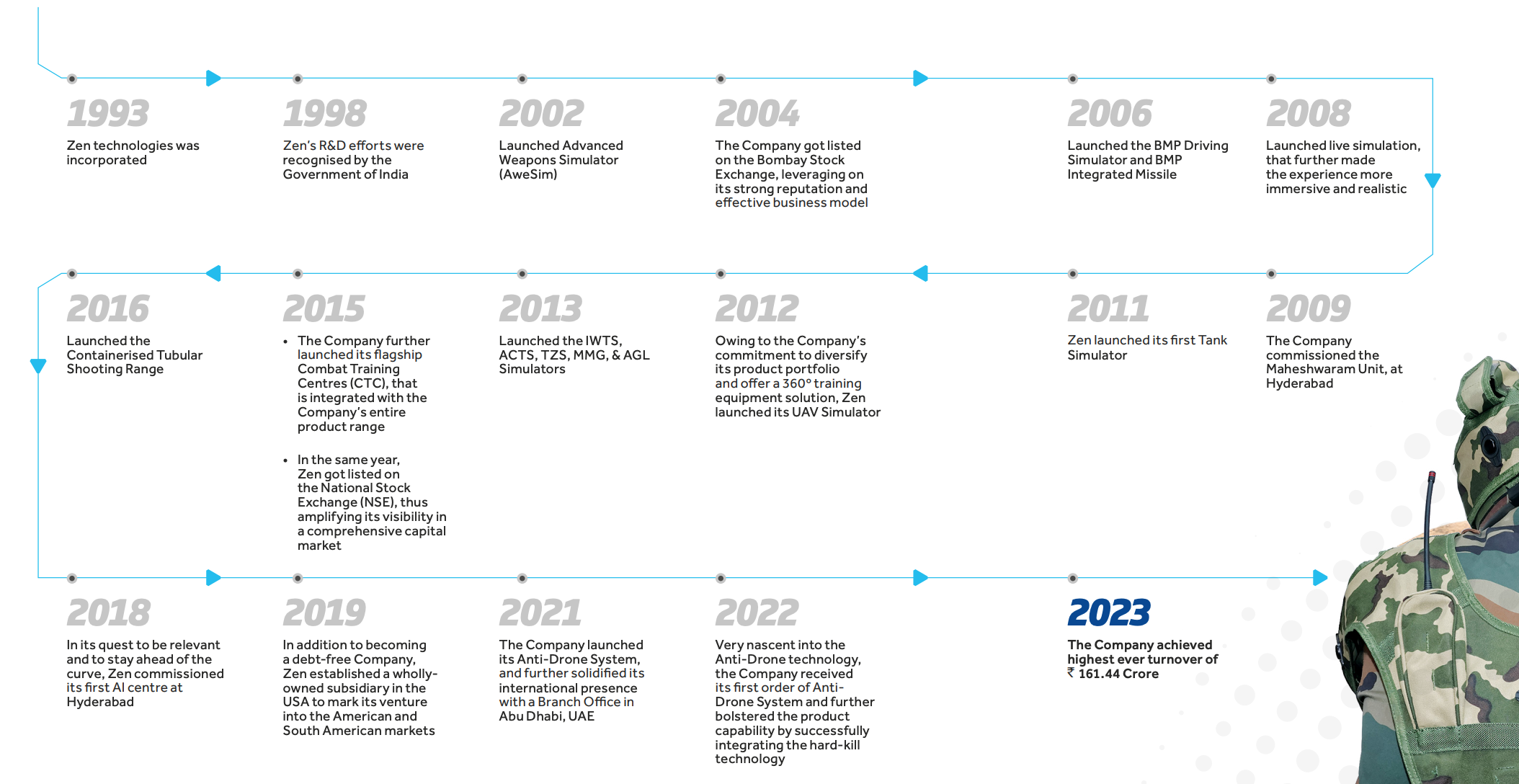

The image below shows the company’s journey from 1993 to 2023.

Here is an interesting quote from Zen Technologies Ltd. from its FY23 Annual Report.

Over the past 3 decades, we have spent hundreds of Crore in R&D to build great products and develop a unique set of capabilities that makes Zen a rare beast in Indian defense. What makes it rare is that, unlike most companies that conduct research funded by DRDO against guaranteed orders, Zen chooses its products, finances its research, and shoulders the complete risk of failure. Remarkably, the IP developed here is 100% owned by Zen. For the first 25 years of its existence, Zen remained laser-focused on simulators, cultivating exceptionally deep expertise in this domain. By contrast, in most other organizations, the IP is either owned exclusively by DRDO, shared jointly with DRDO, or held in collaboration with another partner. Today, in most categories of army simulators, Zen has arguably the world’s best simulators.

The company works on an asset-light model where most of the operations are outsourced and high-value functions like R&D, Engineering, Marketing, Sales, and After-Sales Services are kept in-house. Leveraging the reliable supply chain built over the last three decades, the company can outsource most of its manufacturing, resulting in minimum capital investments and fixed assets. Being an IP-driven business, with bills of material costs typically accounting for 15-35% of the final price, the post-breakeven contributions are substantial.

Chairman & MD of the company Mr. Ashok Atluri mentioned the moment that created a seismic shift for Indian defence companies.

It was in 2015, that the late Mr. Manohar Parrikar immediately got the concept of how Indigenously Designed, Developed and Manufactured (IDDM) can completely alter the Indian defence landscape and included it in the Defence Procurement Procedure 2016 by the category Buy Indian IDDM. I think this was the seminal moment that flipped the defence efforts of the industry from only seeking foreign partnerships for #MakeInIndia and being glorified coolies to establishing indigenous innovative and IP-focused companies developing Indian-owned IP, thus symbolising true #Atmanirbharbharat (self-reliance). This focus on IDDM has helped Zen win new tenders. The IDDM procurement process, thankfully, is very rigorous and companies that want to fake the category are backing out due to the various parameters being tested and severe possible penalties. In many of the tenders, with few companies spending serious R&D money, Zen has emerged as a resultant single vendor. This is helping us not only win Indian orders but also establish ourselves as a global leader for army simulators. Even in the case of anti-drone systems (ADS), we have got orders after being a resultant single vendor. While we are a very serious player in ADS in India, we are putting in extraordinary efforts to gain global leadership too. We plan to continuously invest massive R&D resources in our effort to give absolutely the latest to the Indian and friendly foreign forces. We expect ADS to be a blockbuster product in the coming years.

Current & Future Prospects

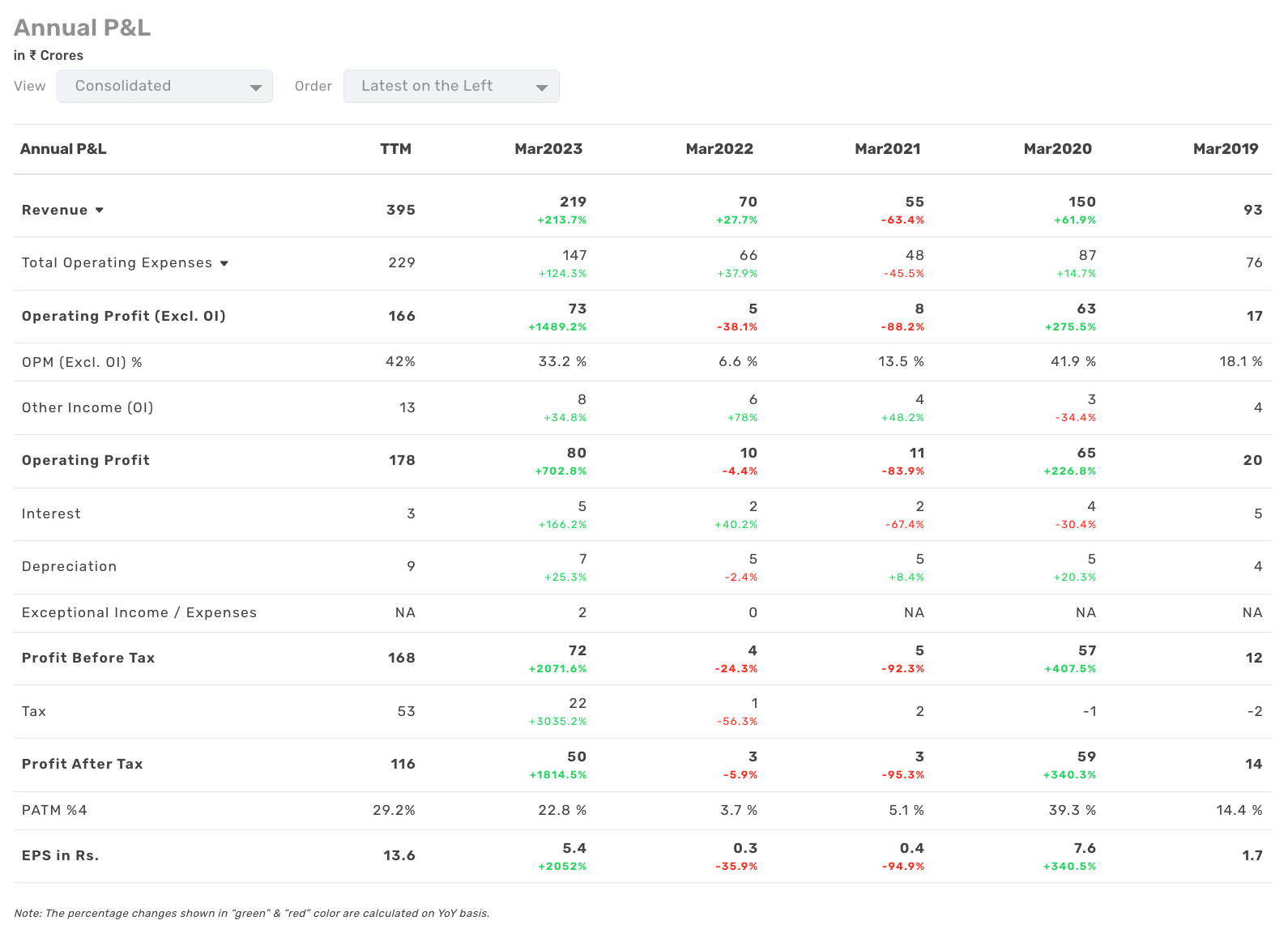

The company has grown rapidly in the last two years. The company’s revenue has jumped from 70 Crores in FY22 to 219 Crores in FY23. And it is expected to reach 450+ Crores in FY24. Along with the revenue growth, the operating margins have improved significantly, resulting in a PAT and EPS of Rs. 116 Crores and Rs. 13.6 respectively.

Notes from the Q4FY23 Conference Call

The company had an order book of Rs. 1434 Crore as of December 31st, 2024. The company is anticipating more orders in the upcoming quarters. The company expects to do Rs. 900 Crore in sales/revenue next year (FY25). And the management is guiding for a CAGR of 50% between FY26 and FY28. The company is guiding towards a 35% EBITDA (Earnings Before Interest Tax Depreciation & Amortization) target for the long term.

The company is also very optimistic about the export markets. The current export order book is around 35% and the company expects this to be a minimum of 50% by FY28. The company is also very optimistic about its anit-drone solutions and expects to be a world leader in this market by FY28. And by FY28 the company expects that the anti-drone solutions will contribute 50% of the revenue.

The company is also looking at inorganic opportunities for growth. The board of directors has approved the company’s proposal to raise Rs. 1000 Crores via QIP if it finds a suitable target for acquisition.

Zen Technologies Ltd. is building a facility in Goa where they expect to do the same work as their Hyderabad facility. A big reason for the Goa facility is to diversify geographically so that if something happens in the Hyderabad facility, then the company has a backup option in Goa.

Here is the link to the company’s Q4FY23 conference call held on January 30th, 2024 (https://www.zentechnologies.com/calls-and-conferences).

Valuation

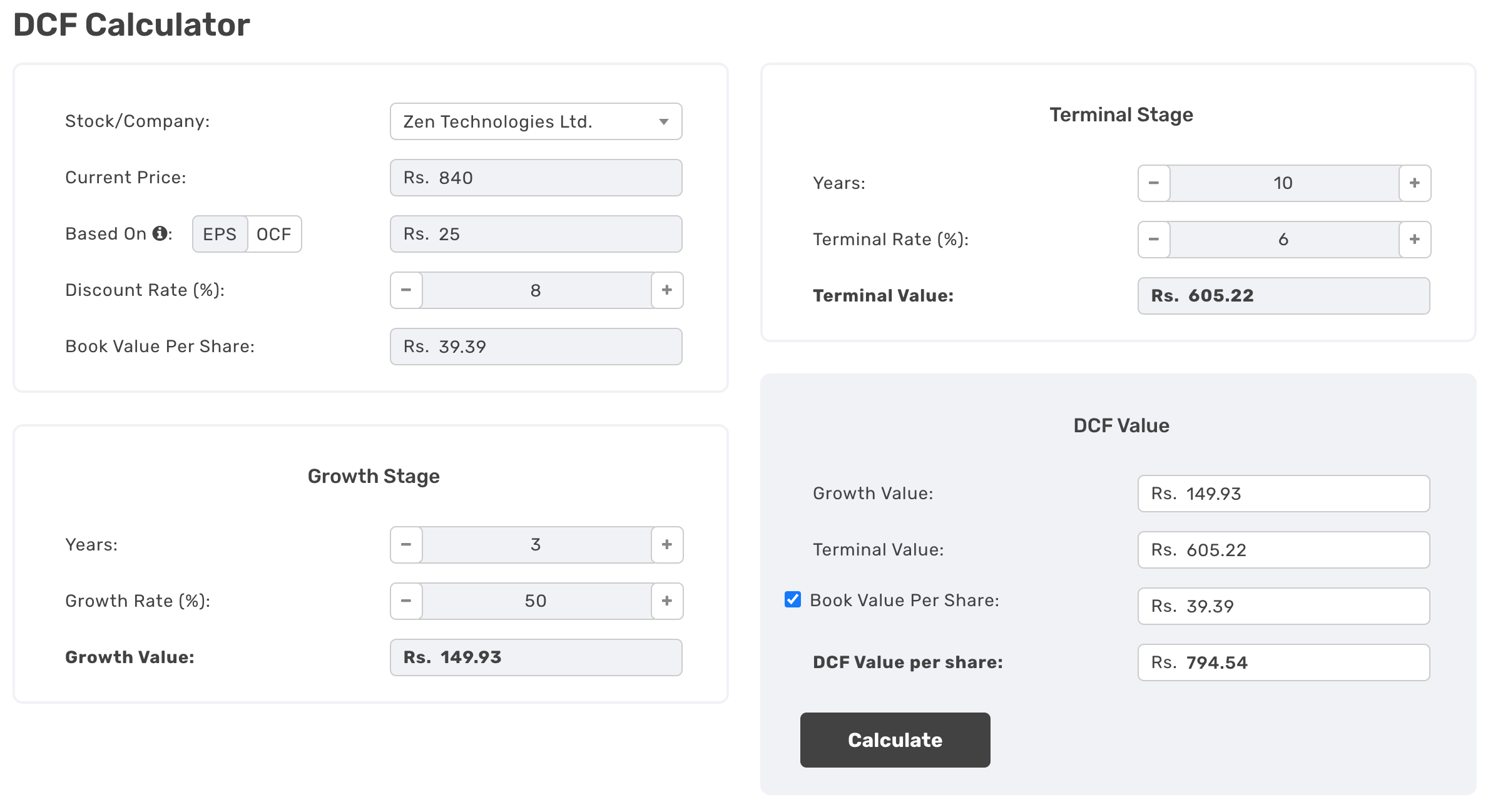

If I take the current price of the company as Rs. 840 and use the TTM EPS of Rs. 13.6, then I get a P/E ratio of around 62, which seems high until I look at the company’s future prospects.

If I take next year’s guidance of Rs. 900 Crores topline and 25% PAT margin, I get Rs. 225 Crore PAT which is roughly Rs. 25 EPS. If I use these numbers and the current price as Rs. 840, I get a forward P/E ratio of around 34.

Further, if I assume 50% growth until FY28 as guided by Zen Technologies Ltd. in its Q4Fy23 conference call, I get an estimated EPS of roughly Rs. 84, giving me an FY28 P/E ratio of 10.

If I use the above assumptions and a discount rate of 8%, I get a DCF value per share of Rs. 794.54

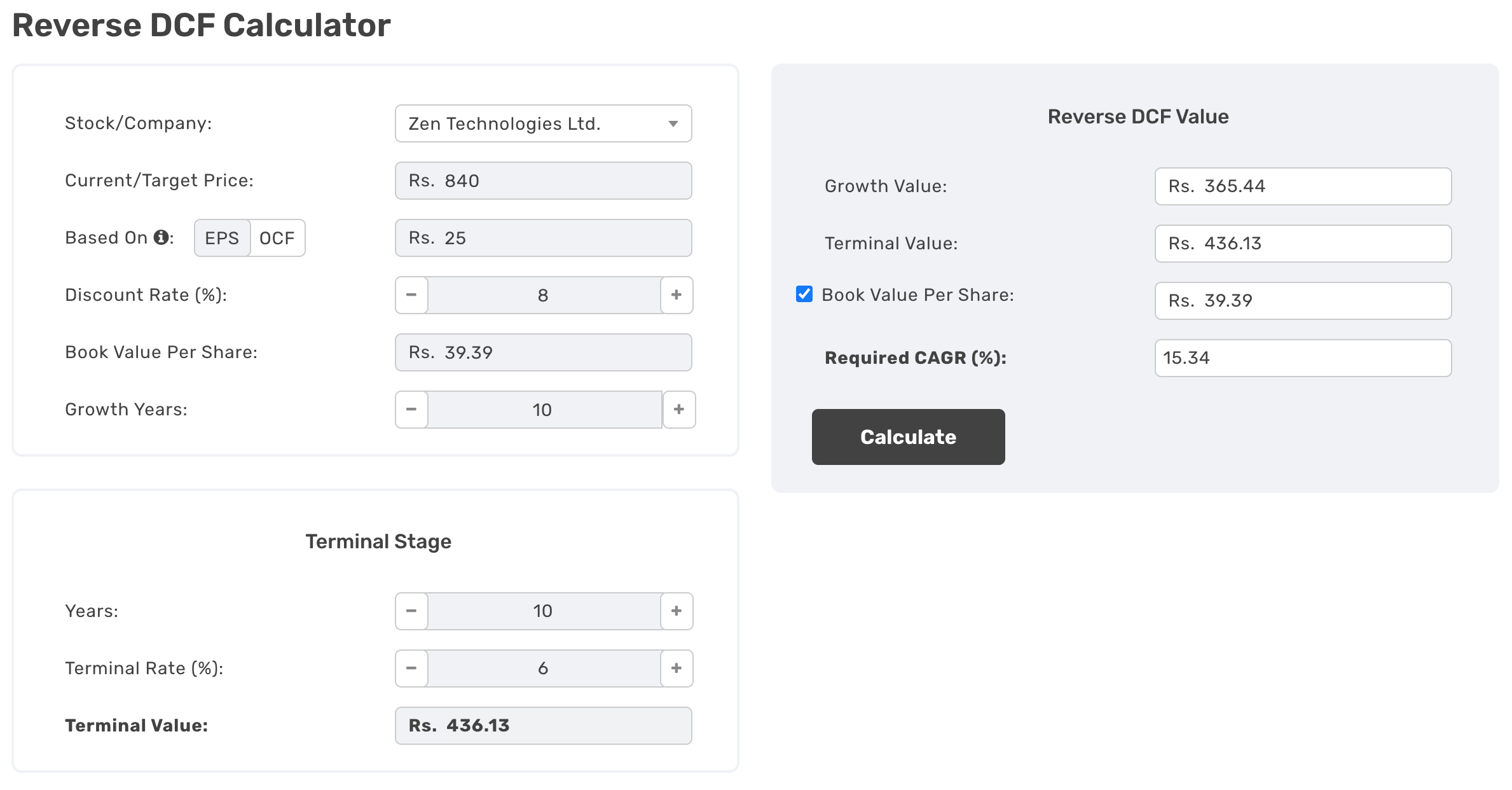

If I input the data into a Reverse DCF calculator to calculate the required CAGR for the next 10 years, I get a required CAGR value of 15.34%.

Another way to look at this is by assigning an exit multiple to the estimated FY 28 EPS. If I assign an exit multiple of 10, 20, 30, 40, and 50 to the estimated FY 28 EPS of Rs. 84, I get an estimated price of the company as Rs. 840, Rs. 1680, Rs. 2520, Rs. 3360, and Rs. 4200 in FY28.

Risks

- Future order flows not materializing as per the management’s expectations could derail the growth story.

- A change in the government at the center (Indian Government) could also impact future order flows significantly.

- Operations and profit margins might be at risk due to escalating competition and aggressive pricing strategies by international competitors. These firms may significantly drop their prices to secure a larger market share in India.

- Unfavorable macroeconomic conditions could pose a risk to the company. In such circumstances, governments may shift their focus to immediate concerns and possibly deprioritize defense spending.

- Much of the simulator production is based on specific client feedback, with no guaranteed purchase of the end product. This scenario places the company at a substantial financial risk.

- The standard governmental policy of procurement from the lowest bidder could pose a threat to the Company. Occasionally, other vendors, having already amortized their development costs, can offer cheaper solutions due to their larger capacity.

- Zen Technologies heavily relies on the Indian Government for a significant part of its business, whether it’s policy-driven or on actual product sales.

I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

This article is for information and education purposes only. I wrote this article myself, and it expresses my own opinions. I have no business relationship with any company whose stock is mentioned in this article. The facts and opinions appearing in the article do not reflect the views of Thryvv Analytics Pvt. Ltd. and Thryvv Analytics Pvt. Ltd. does not assume any responsibility or liability for the same.