Route Mobile: Is it on a route to outperform?

– Route Mobile is a leading global CPaaS player.

– Route Mobile has demonstrated revenue CAGR of almost 32% over the last five years.

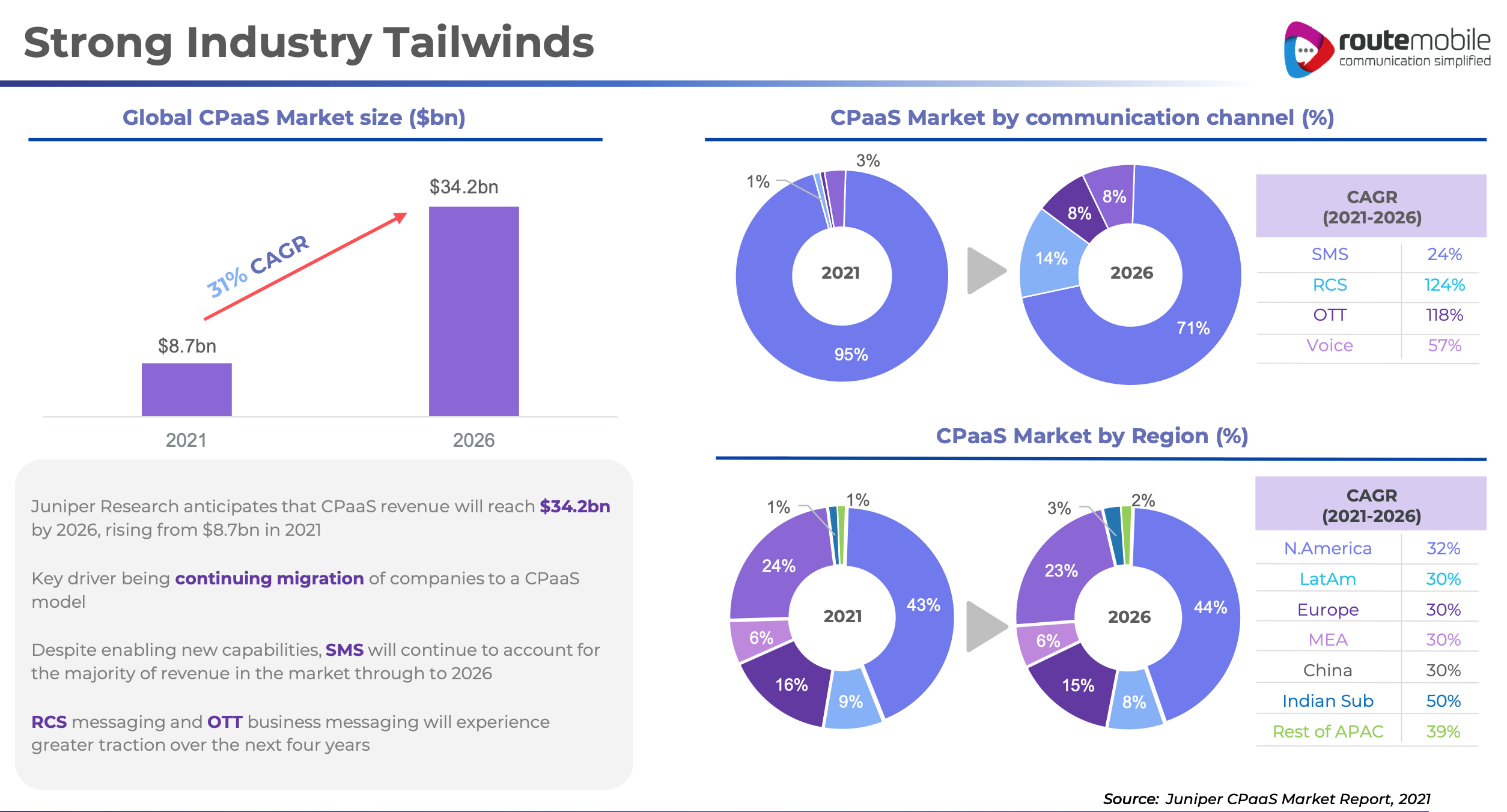

– As per a research report by Juniper Research, the global CPaaS market is expected to grow at a CAGR of 31% between 2021 and 2026.

Route Mobile Introduction

For those who are not familiar with Route Mobile, here is a brief introduction about the company from its website.

Founded in 2004, Route Mobile is a publicly listed company and among the leading Cloud Communications Platform service provider offering Communication Platform as a Service (CPaaS) solutions. We cater to enterprises, over-the-top (OTT) players, and mobile network operators (MNO) and our portfolio comprises solutions in messaging, voice, email, SMS filtering, analytics, and monetization. We deliver an entire communication product stack, based on a CPaaS principals, infusing Conversational AI across a broad range of industries including social media companies, banks and financial institutions, e-commerce entities, and travel aggregators.

In layman’s terms, the OTP (one-time password) that you receive when you login into an app like Flipkart, Netflix, or EaseMyTrip, the SMS (text message) that you receive from your bank about your balance/transactions, the OTP that you receive to confirm your shopping purchase, the pop-up chat window that you see on websites, the marketing emails, WhatsApp messages, and automated pre-recorded phone calls that you get are all enabled by a CPaaS company like Route Mobile.

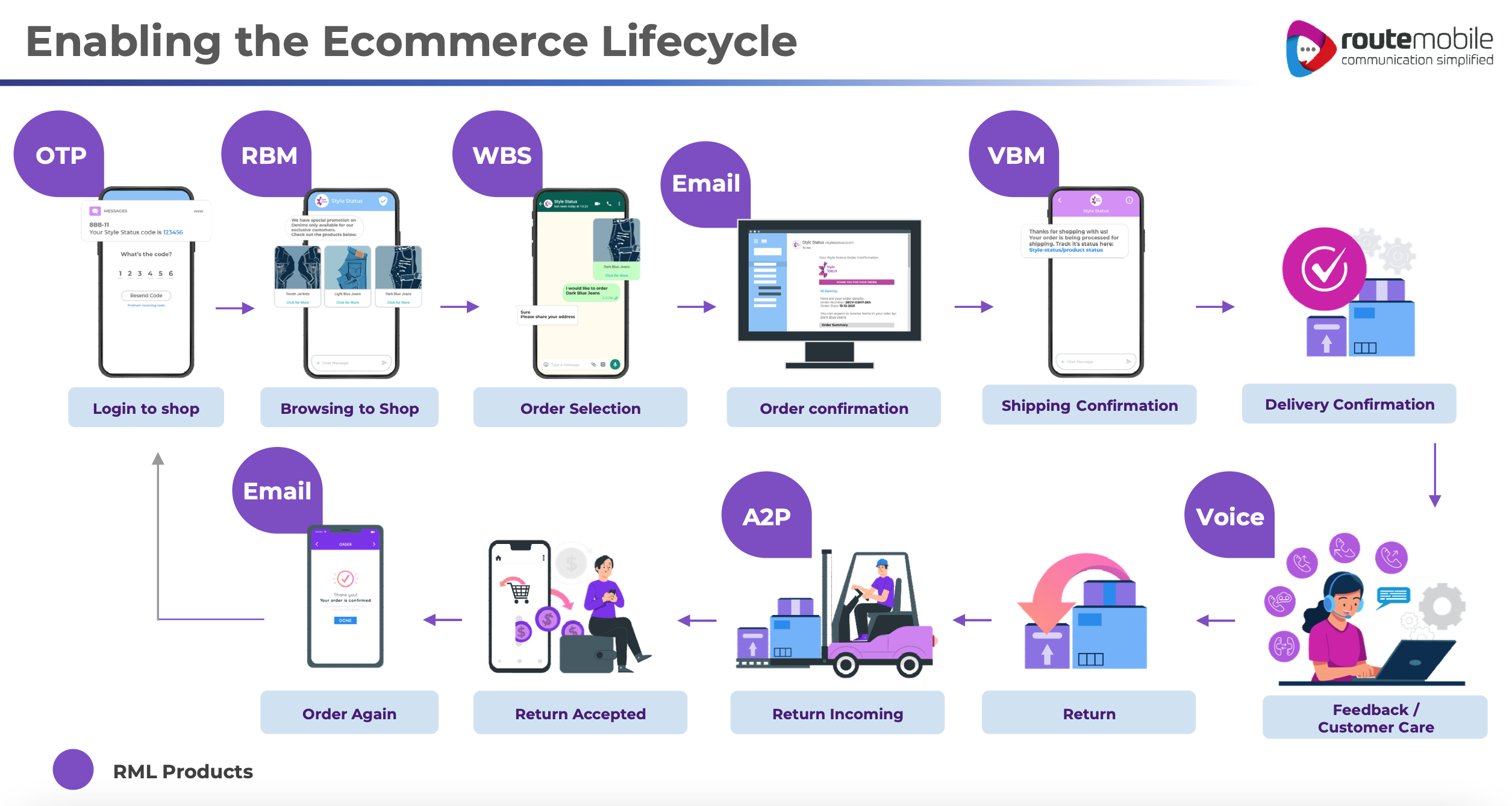

Below is an example showing the use of CPaaS in an E-commerce Lifecycle.

Industry

As per a 2021 report by Juniper Research, the global CPaaS market is expected to grow from $8.7 billion in 2021 to $34.2 billion in 2026, representing a CAGR of 31%. And Route Mobile being a leading player in the CPaaS market with a global footprint may be expected to grow above the industry average rate.

Another research report from “Mordor Intelligence” is forecasting a CAGR of 34.3% for the global CPaaS industry between 2017 and 2027, with the fastest growing market being “Asia-Pacific” where Route Mobile has a good footing.

Financials

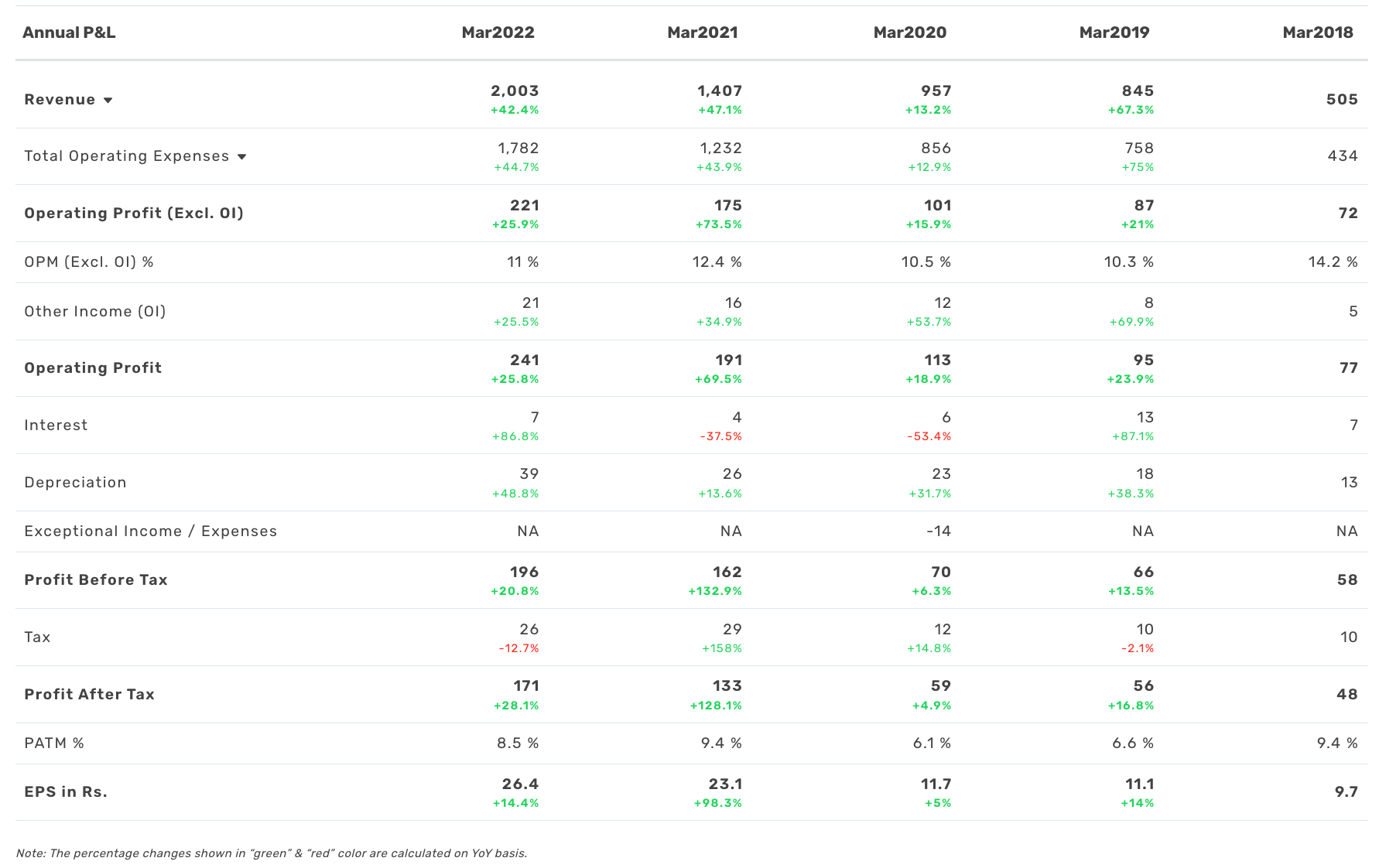

Route Mobile has demonstrated the ability to grow consistently over a period of five years with a five year revenue CAGR of almost 32%.

Also, if you take a look at the recent quarterly results, Route Mobile has demonstrated good growth while other competitors are struggling to report good numbers. However a big portion of the recent growth in revenue at Route Mobile can be attributed to increase in price of their services, so this is not a sustainable level of growth. Going forward one can expect revenue growth to normalize. Another point to note is the improvement in OPM (operating profit margin) for the last three quarters. And if you listen to the recent management conference call , the management is guiding for a further improvement in operating margin going forward.

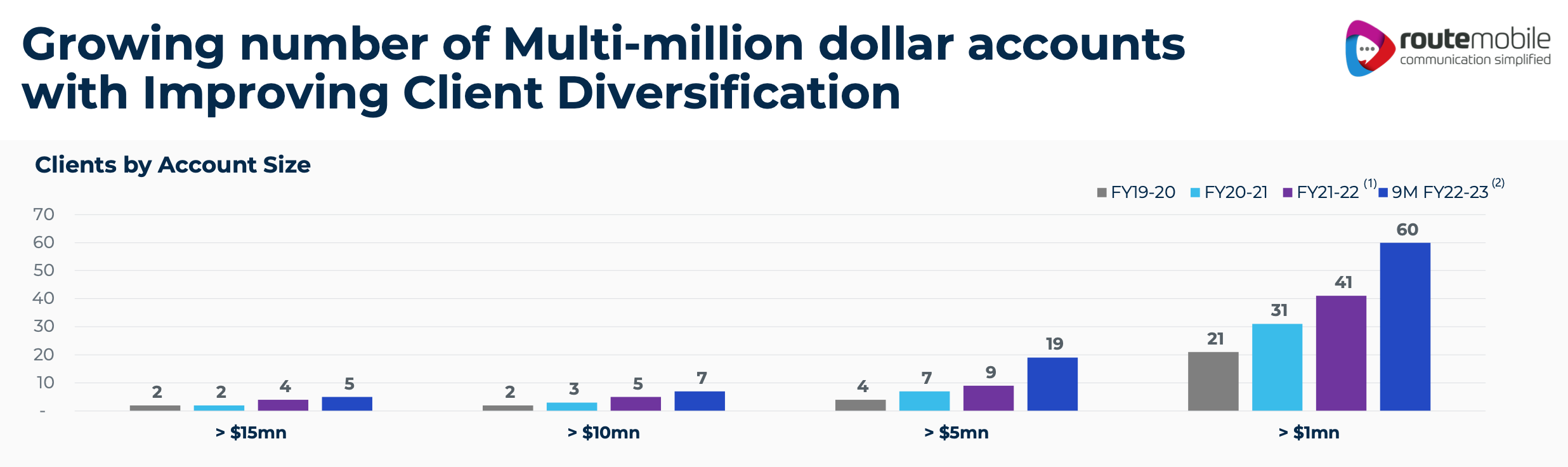

With a net revenue retention rate of 125% (as per the January 23 2023 Investor Presentation), the management has shown good ability to persuade its existing customers to spend more with the company and adopt more products/service from the company. As you can seen in the picture below, the number of clients spending more and more with Route Mobile has consistently increased over the years across all account sizes.

Valuation

Currently, Route Mobile is trading at a LTM (last twelve month) PE ratio of 58, and a TTM (trailing twelve month) PE ratio of 28.5. And if you consider the growth rate that Route Mobile has demonstrated over the past five years and factor in the strong industry tailwinds, the current valuation of Route Mobile can be justified.

Risks

- Most of the recent growth at Route Mobile has come via inorganic acquisitions and the management has indicated its appetite for more inorganic acquisitions. While inorganic acquisitions have been well executed so far, there is a risk of mismanagement in the future.

- Current global macro headwinds could potentially reduce demand and stifle Route Mobile’s growth.

- Competition could take away market share from Route Mobile.

- As per management guidance during the January 23 2023 conference call, Q4 revenue is expected to be soft compared to Q3, and operating cash flow is expected to be under pressure due to the upcoming firewall deals.

I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

This article is for information and education purposes only. I wrote this article myself, and it expresses my own opinions. I have no business relationship with any company whose stock is mentioned in this article. The facts and opinions appearing in the article do not reflect the views of Thryvv Analytics Pvt. Ltd. and Thryvv Analytics Pvt. Ltd. does not assume any responsibility or liability for the same.

Disclaimer: This article should not be taken as an investment advice. Please consult your investment advisor before making a financial decision.