Olectra Greentech: Electrifying The Indian Bus Industry

– Olectra Greentech Ltd. delivered 563 e-buses & 17 e-tippers in FY22-23.

– The company is on track to deliver 700 e-buses and e-tippers in FY23-24

– The company has an order book of 8088 e-buses as per the management conference call held on February 1st, 2024.

– The government of India is pushing for the electrification of the Indian public transport segment (bus) and providing incentives for the same.

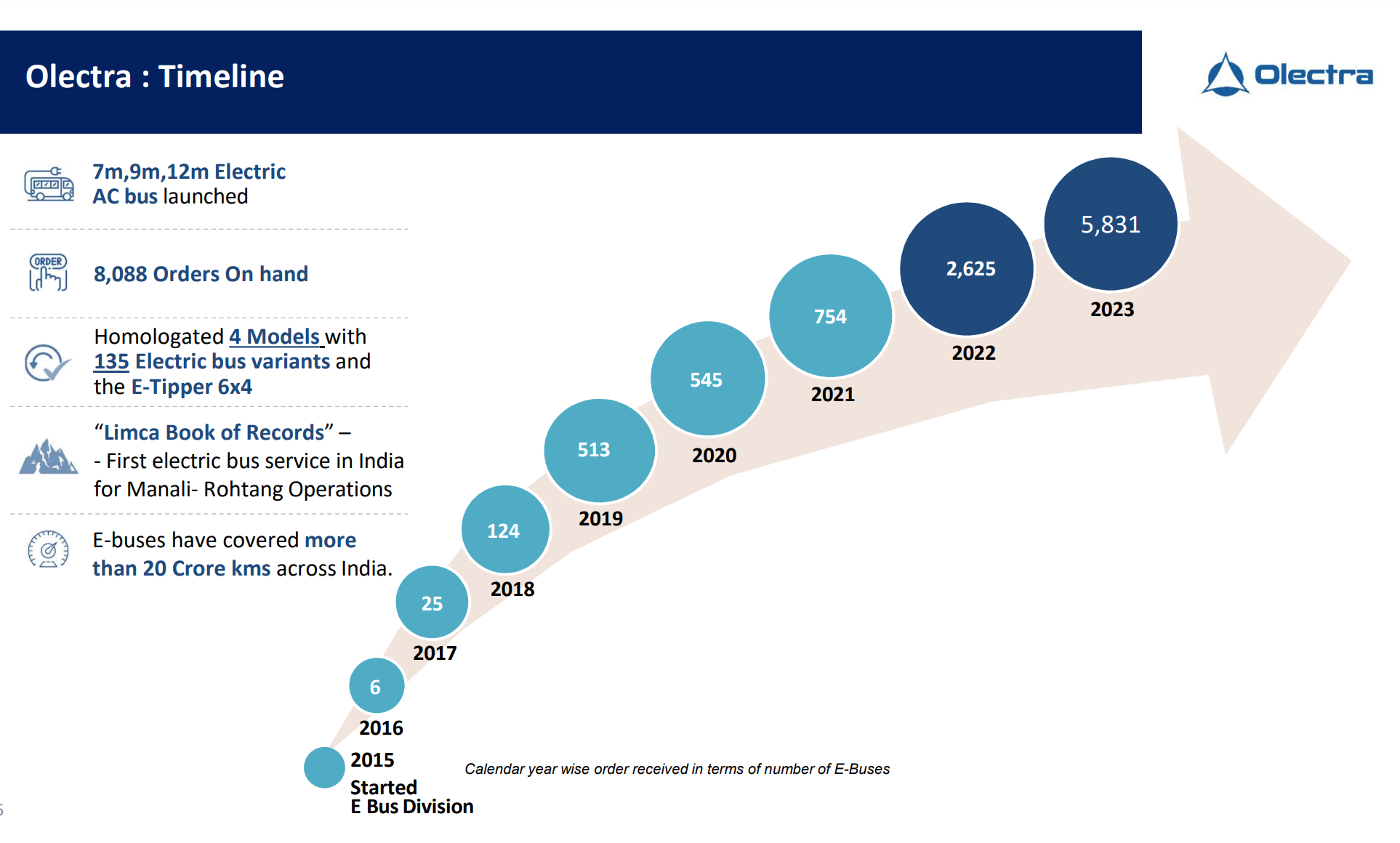

Olectra Greentech Ltd. is a manufacturer of electric buses and composite polymer insulators. It makes 7 meters, 9m, 12m buses and they have recently developed an electric tipper truck. They are also working on an electric RMC truck and have a hydrogen fuel-cell-based bus project in partnership with Reliance. The company sold 259 e-buses in FY21-22 while it sold 563 e-buses and 17 e-tippers in FY22-23. It has sold 376 e-buses and e-tippers in the nine months of FY23-24 and the management is expecting to sell 700+ e-buses and e-tipper by the end of the year FY23-24.

The company has established relationships with various STUs (state transport units) and has an order book of 8088 e-buses as per the conference call held on February 1st, 2024. The demand for e-buses is expected to keep on increasing in India with the government’s push (FAME 1.0 and FAME 2.0) for electrification of the transport sector.

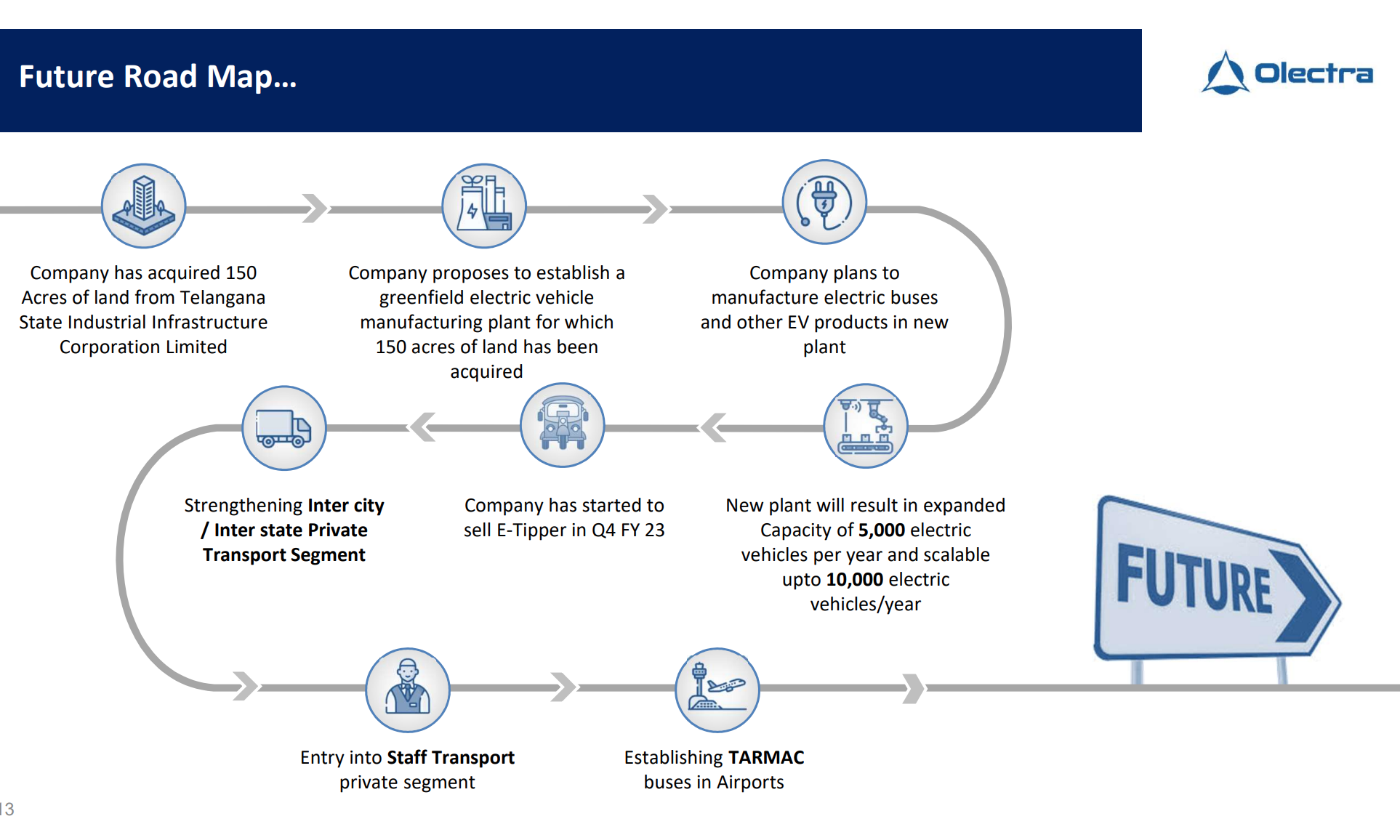

The current manufacturing capacity is 1,500 e-buses and e-tippers and the company is constructing a new plant with a capacity of 5,000 e-buses and e-tippers, expandable up to 10,000. Pilot production from the new plant is expected in Feb 2024 and the new plant is expected to be fully operational by July 2024 with a capacity of 5,000.

Looking at the Future

The below-mentioned points are taken from the management conference calls on November 7th, 2023, February 1st, 2024, and the management interview given to CNBC TV18 on January 2nd, 2024.

- The management is expecting to deliver 2500 e-buses & e-tippers in FY24-25 and 5000 e-buses & e-tippers in FY25-26.

- The company has delivered 35 e-tippers so far and has an order book of 25 e-tippers. Demos are being conducted at many private companies and the management expects to see some momentum in the next 6 months to 1 year.

- A major order from BEST (Brihanmumbai Electric Supply & Transport Undertaking) for 3000 e-buses is on the horizon where Olectra is L1. Pricing and other terms are being negotiated currently.

- Another major order of 3000 e-buses from PMC (Pune Municipal Corporation) is being awaited where the company is L1 and is currently negotiating pricing and other terms.

- A tender for Prime Minister e-Seva about 10,000 e-buses is likely to come up in the next 5 months to 6 months in about 169 cities

- The management expects the market for e-buses to grow to 40,000 in the next 2-4 years.

Source: November 7th, 2023 Conference Call, January 2nd, 2024 Interview, February 1st, 2024 Conference Call

Valuation

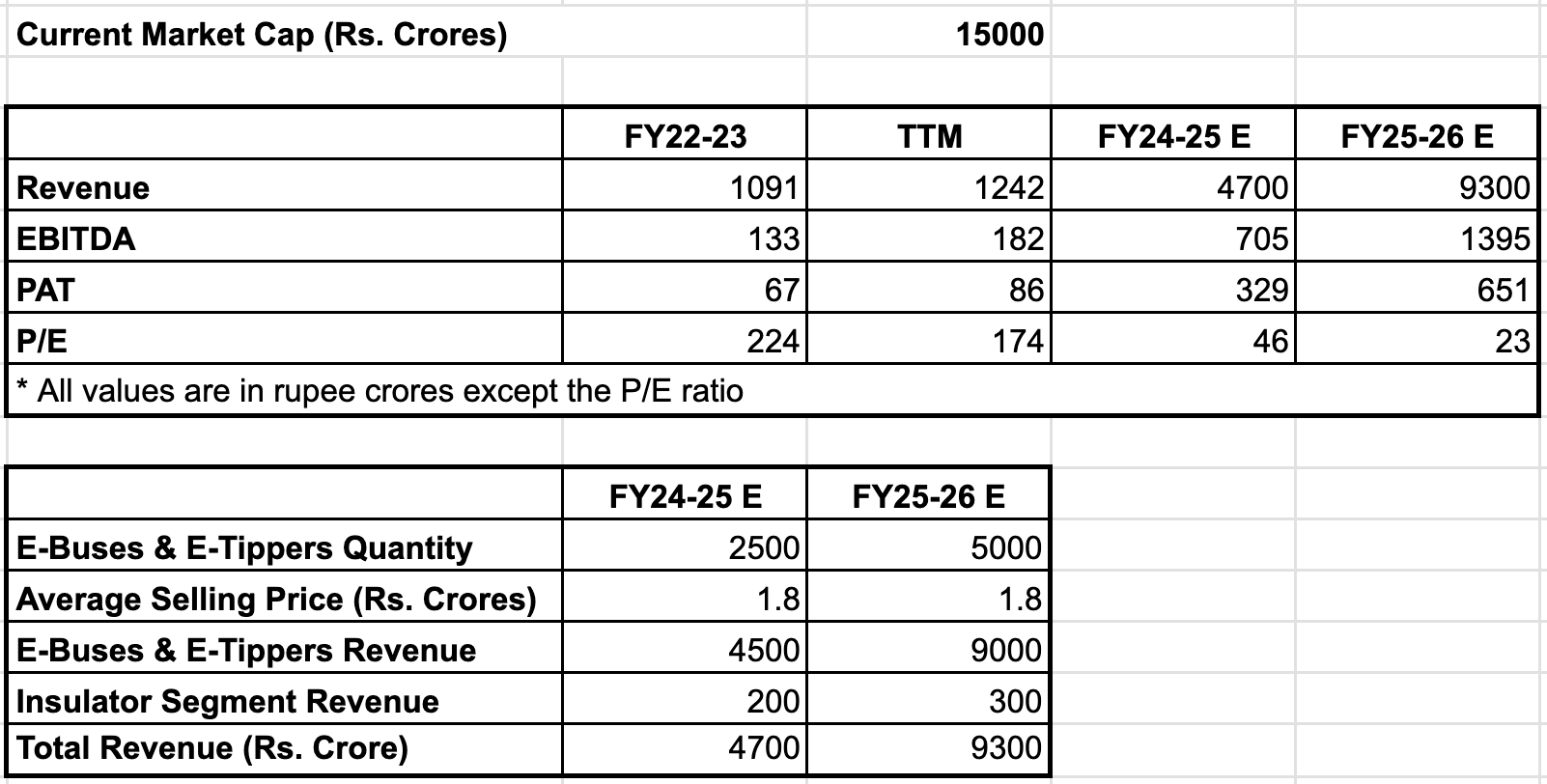

If I take the FY22-23 EPS of Rs. 8, the P/E ratio at the current price of Rs. 1,840 comes to 230. If I take the trailing twelve months (TTM) EPS of Rs. 11, the P/E ratio comes to 167. The market cap of the company is around 15,000 crores and it is doing around 1,200 crores in revenue/sales as of the trailing twelve months. On a primary look the valuation seems high, so let’s try to forecast the next two years as per the management’s guidance and see what valuations we arrive at.

As per the management, e-buses sell for anywhere between 1.2 to 2 crores depending on the size of the e-bus. And e-tipper selling price is around 1.3 to 1.4 crores. If I take that the management will deliver 2500 e-buses and e-tippers in FY24-25, and take an average selling price of 1.8 crores, I get a revenue of Rs. 4,500 Crores and if I add Rs. 200 crore revenue from the insulator segment, I get a total forecasted revenue of Rs. 4,700 crores for FY24-25. And if I take the PAT margins at 7%, I get a PAT of Rs. 329 crores. Taking the current market cap as Rs.15,000 crores, I get a P/E ratio of around 46. If I do a similar exercise for FY25-26 for 5000 e-buses and e-tippers with Rs. 300 crore revenue from the insulator segment, I get a PAT of Rs. 651 crore. And this gives me a P/E ratio of around 23.

Source: Author’s calculations based on the management’s commentary from the November 7th, 2023, and February 1st, 2024 conference calls.

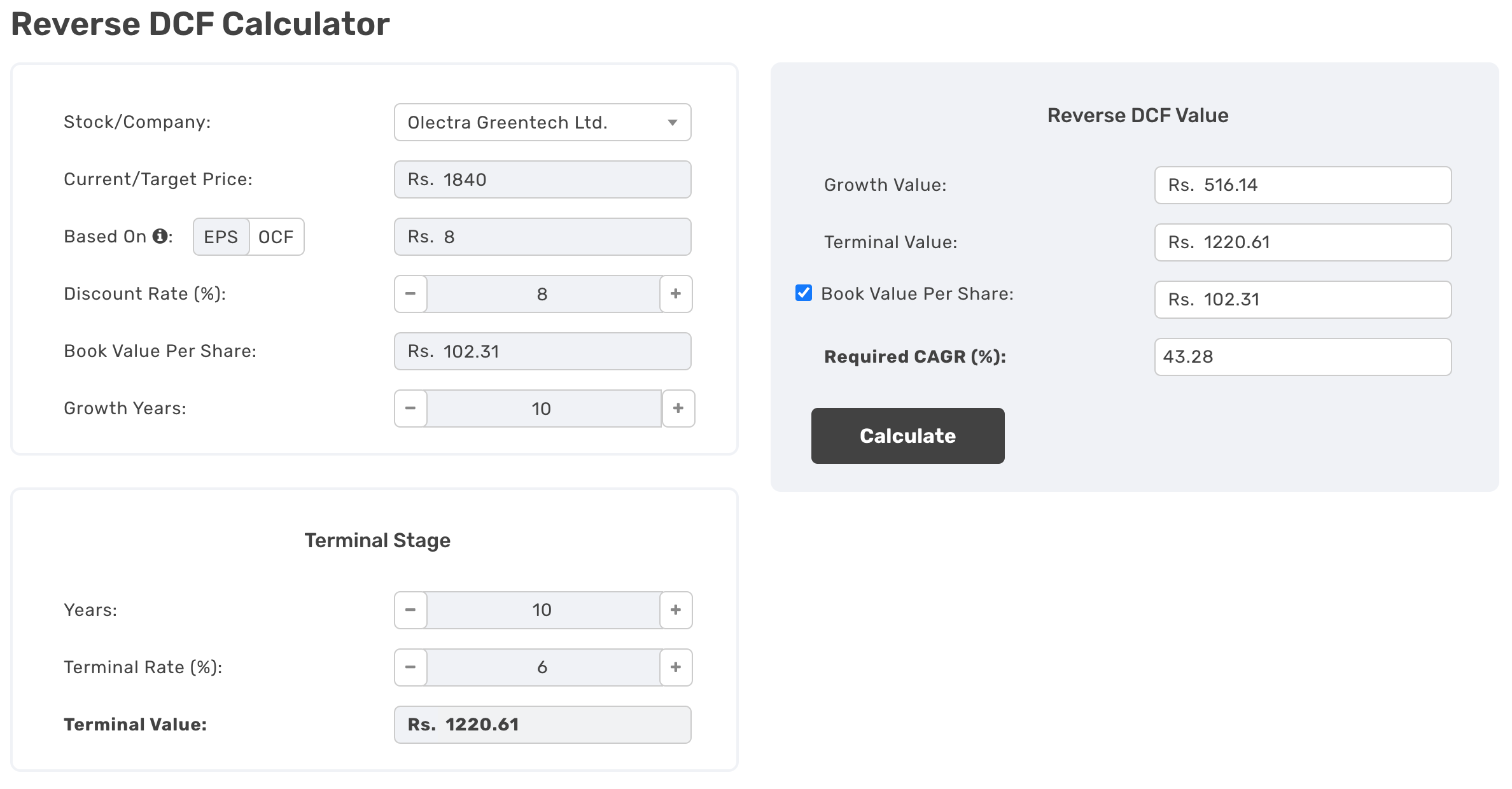

Now, if I do a Reverse DCF calculation using the values shown below, Olectra Greentech Ltd. needs a CAGR of around 43% for the next 10 years to justify the current valuations.

Your assumptions are likely to be very different than mine, so I would encourage you to try them out with the Reverse DCF calculator available at https://www.thryvv.in/reverse-dcf-calculator/ and see what you arrive at.

Risks

- In the August 10th, 2023 Conference Call the management guided for 1200-1500 e-buses & e-tippers for FY23-24. The management then reduced that guidance to 1000 in the November 7th, 2023 Conference Call. The management again reduced the guidance to 700 in the February 1st, 2024 Conference Call.

- My second biggest concern stems from their strong technology partnership with BYD (a Chinese Company). The partnership started in 2015 and as per the management, it is likely to go beyond 2025. Olectra Greentech Ltd. is dependent on BYD for the battery cells and some of the child parts relating to the powertrain. Apart from this, all the other components, are sourced locally in India. As per the management, 25-40% of e-bus components come from BYD. This heavy dependency on a Chinese company is concerning. Considering the current geo-political tensions between India and China, it is very likely that the government of India would not view relations with a Chinese company favorably.

- The management is guiding for 5000+ e-buses & e-tippers in FY25-26 and is currently struggling to reach 1000 in FY23-24. I have my doubts about the management’s ability to scale up so quickly for FY25-26.

- The government of India introduced/modified the battery testing norms and that caused the company to lose production for about 3 to 4 months. With e-buses being a new category, more such hiccups are rather likely compared to a mature industry/segment.

- The management has been talking up the hydrogen fuel-cell buses in partnership with Reliance but no tangible progress has been reported or accomplished.

- Even with the 8088 e-bus order book on hand, I am not able to understand the management’s reluctance to work in multiple shifts instead of the current one-shift structure of production.

I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

This article is for information and education purposes only. I wrote this article myself, and it expresses my own opinions. I have no business relationship with any company whose stock is mentioned in this article. The facts and opinions appearing in the article do not reflect the views of Thryvv Analytics Pvt. Ltd. and Thryvv Analytics Pvt. Ltd. does not assume any responsibility or liability for the same.