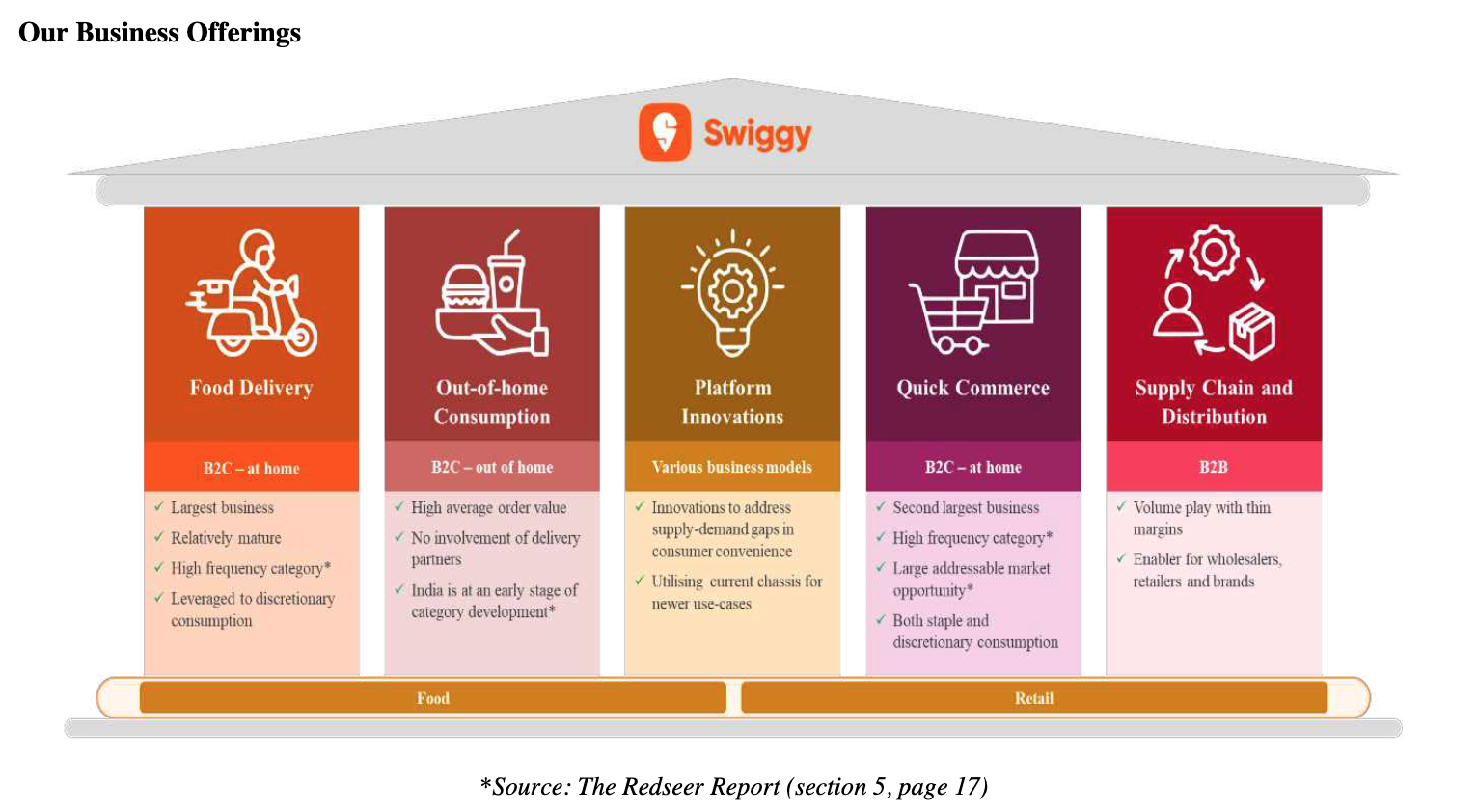

A Look At Swiggy

– Swiggy operates four businesses: Food delivery, Out-of-home consumption, Quick Commerce, and Supply Chain and Distribution.

– While the Food Delivery Business is mature and churning out positive cash flows, the Quick Commerce business seems to have the bigger potential over the long term.

– In this article, I value each business individually to arrive at a sum of the parts valuations for Swiggy.

– I also compare its valuation to globally listed peers.

Introduction

Swiggy divides its operations into five different businesses:

- Food Delivery (Swiggy)

- Out-of-home Consumption (Dineout and SteppinOut)

- Quick Commerce (Instamart)

- Supply Chain and Distribution

- Platform Innovations (Swiggy Genie, Swiggy Minis, Private Brands)

Food Delivery

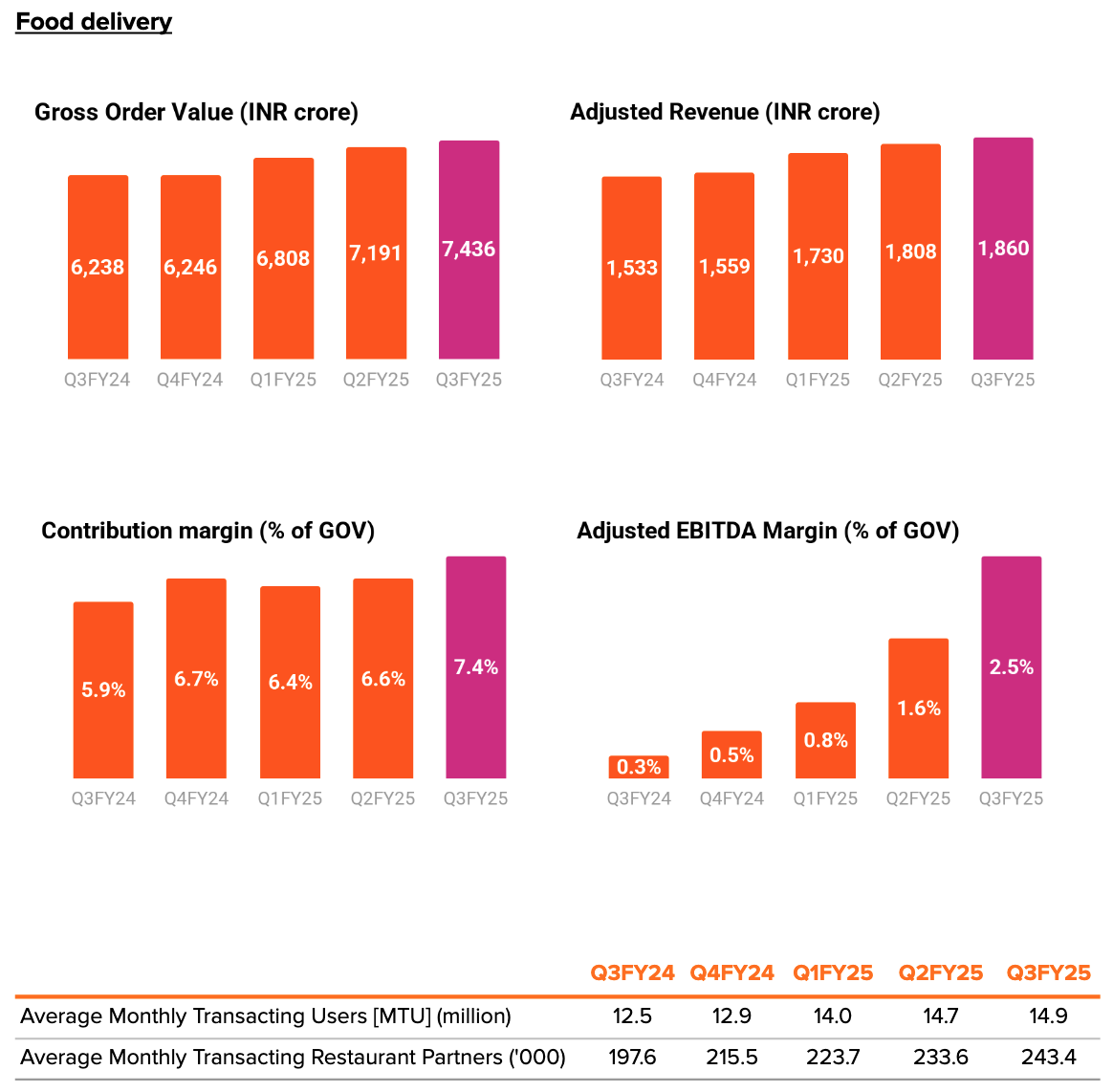

From FY2022 to FY2024, Swiggy’s Food delivery business has grown its GOV (Gross Order Value) at a CAGR (Compounded annual growth rate) of around 16%, and its Gross Revenue has had a CAGR of 17%. In the same period, the AOV (Average order value) has grown from Rs. 407 to Rs. 428, and the number of orders has grown from 454 million to 577 million.

Source: Swiggy’s RHP

If we look at the recently concluded quarter, there has been a slight acceleration in the GOV & Adjusted Revenue growth to 19% & 21% YOY (Year Over Year) respectively. There has also been healthy growth in the average monthly transacting user and average monthly transacting restaurant partners numbers. However, the biggest positive is the rapid improvement in the adjusted EBITDA margin percentage. This has improved rapidly from 0.3% in Q3FY24 to 2.5% in Q3FY25.

Source: Swiggy’s Q3FY25 Shareholder’s Letter

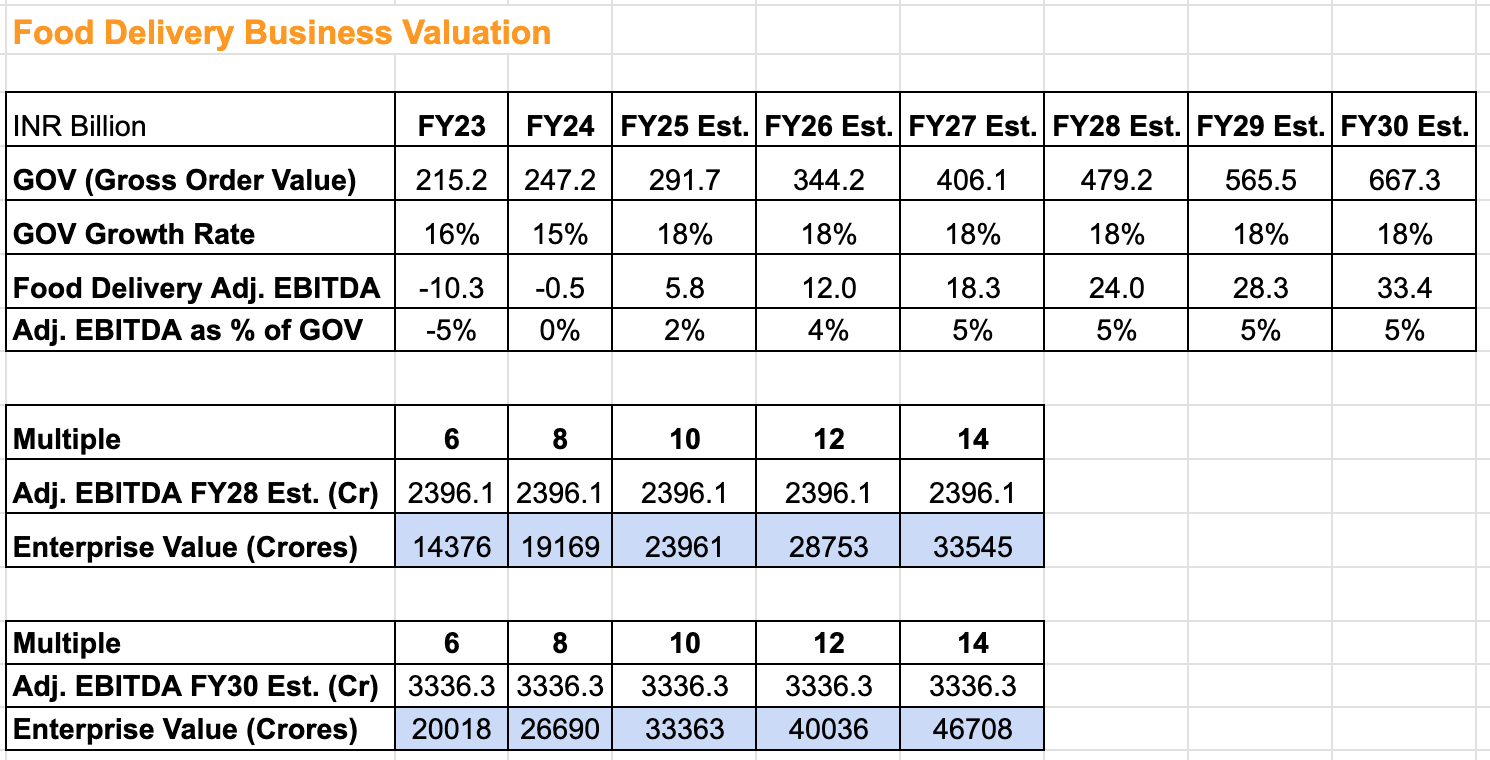

Because Swiggy is not profitable on a PAT basis, I will value it based on the Adjusted EBITDA numbers. Based on the above trends, if we estimate that the GOV will grow at 18% for the next five years (management guidance is for 18-22% in the medium-term) and the Adjusted EBITDA as a percentage of GOV will trend towards 5% (management guidance for medium-term), then we can arrive at an estimated Adjusted EBITDA of Rs. 3336 Crores in FY30. And if we are to apply a reasonable EV/Adj. EBITDA multiple of 8, we get an enterprise value of Rs. 26,690 Crores based on the FY30 estimated numbers. And if I want to be conservative, I would use the FY28 estimated numbers. And that gives me an enterprise value of Rs. 19,169 Crores.

Source: Author’s estimates

Source: Author’s estimatesOut-of-home Consumption

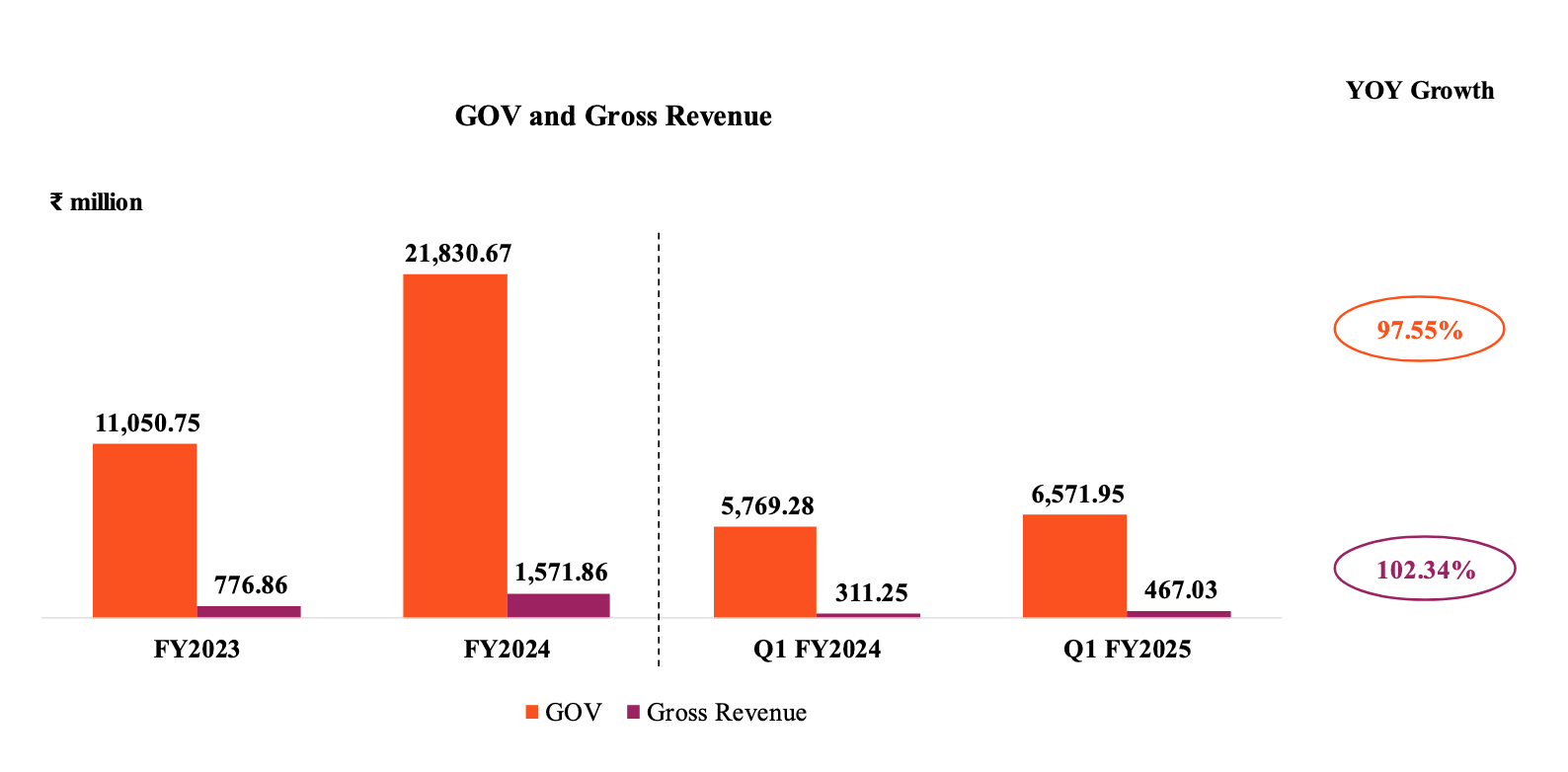

From FY2023 to FY2024, Swiggy’s Out-of-home Consumption business has grown its GOV (Gross Order Value) by 98%, and its Gross Revenue grew by 102%.

Source: Swiggy’s RHP

Source: Swiggy’s RHP

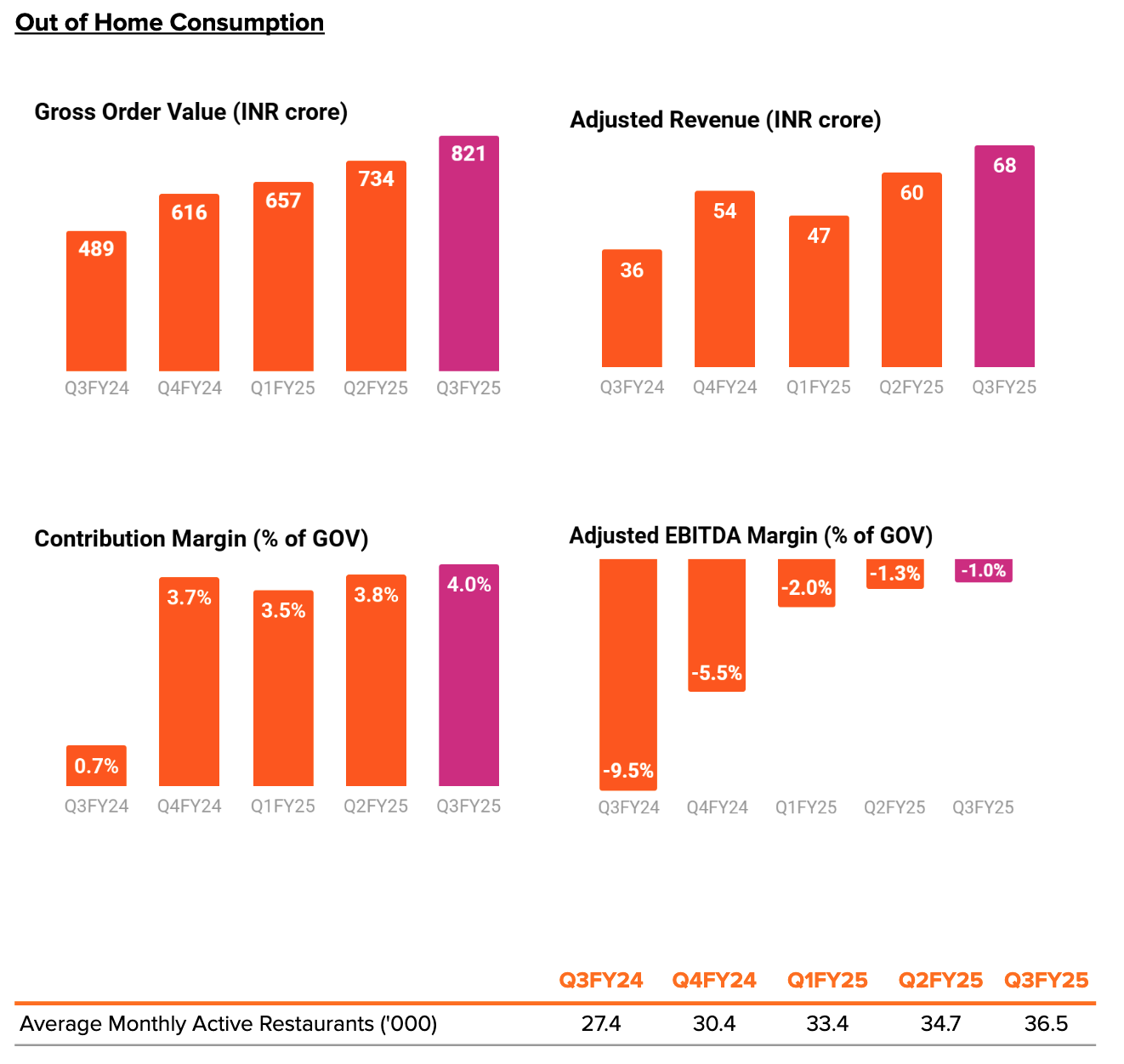

If we look at the recently concluded quarter, the GOV & Adjusted Revenue growth has come down to 68% & 88% respectively. There has also been healthy growth in the average monthly active restaurants. However, the biggest positive is the rapid improvement in the adjusted EBITDA margin percentage. This has improved rapidly from -9.5% in Q3FY24 to -1% in Q3FY25.

Source: Swiggy’s Q3FY25 Shareholder’s Letter

Source: Swiggy’s Q3FY25 Shareholder’s Letter

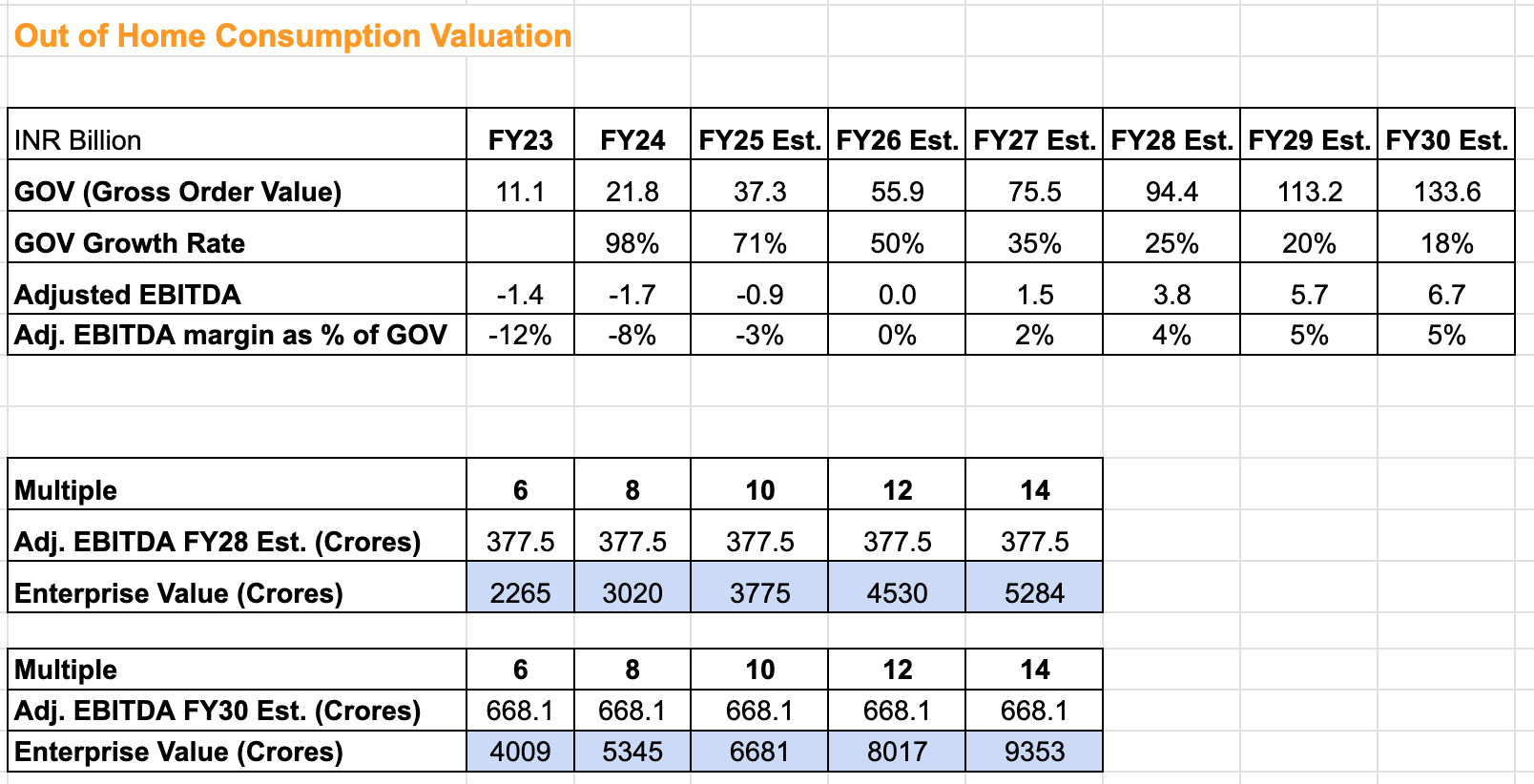

Based on the above trends, if we estimate that the GOV will grow between 71% to 18% for the next five years and the Adjusted EBITDA as a percentage of GOV will trend towards 5%, then we can arrive at an estimated Adjusted EBITDA of Rs. 668 Crores in FY30. And if we are to apply a reasonable EV/Adj. EBITDA multiple of 8, we get an enterprise value of Rs. 5,345 Crores based on the FY30 estimated numbers. And if I want to be conservative, I would use the FY28 estimated numbers. And that gives me an enterprise value of Rs. 3,020 Crores.

Source: Author’s estimates

Source: Author’s estimatesQuick Commerce

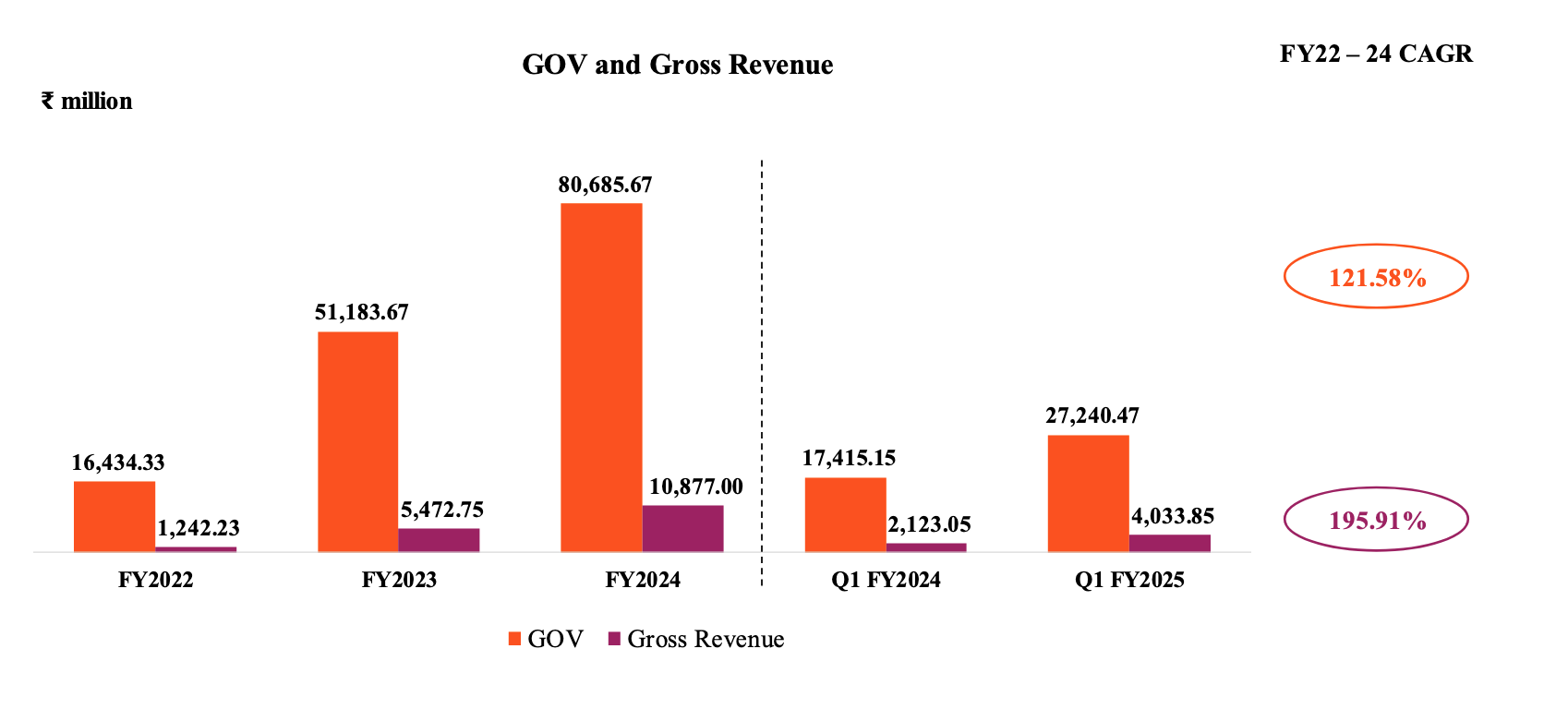

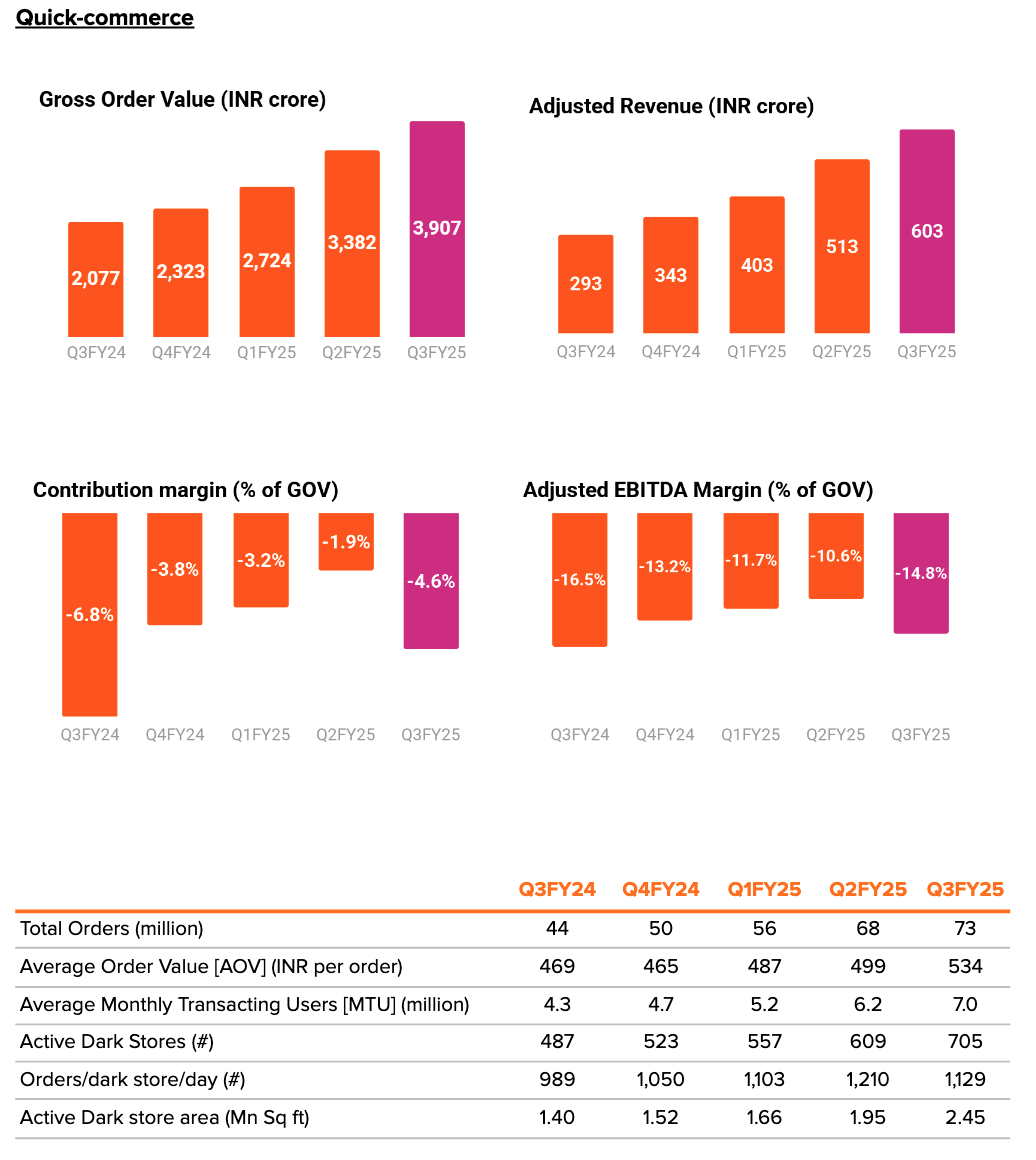

From FY2022 to FY2024, Swiggy’s Quick Commerce business has grown its GOV (Gross Order Value) at a CAGR (Compounded annual growth rate) of around 122%, and its Gross Revenue has had a CAGR of 196%.

Source:

Source: If we look at the recently concluded quarter, the GOV & Adjusted Revenue growth has come down to 88% & 106% respectively. There has also been healthy growth in total orders, AOV, etc. There has been a steady improvement in the adjusted EBITDA margin percentage. This has improved from -16.5% in Q3FY24 to -10.6% in Q2FY25. However, due to increased competitive activities in the Quick Commerce business, the adjusted EBITDA margins have taken a hit in the recent quarter. Also, management expects this to be range-bound for the near term.

Source: Swiggy’s Q3FY25 Shareholder’s Letter

Source: Swiggy’s Q3FY25 Shareholder’s Letter

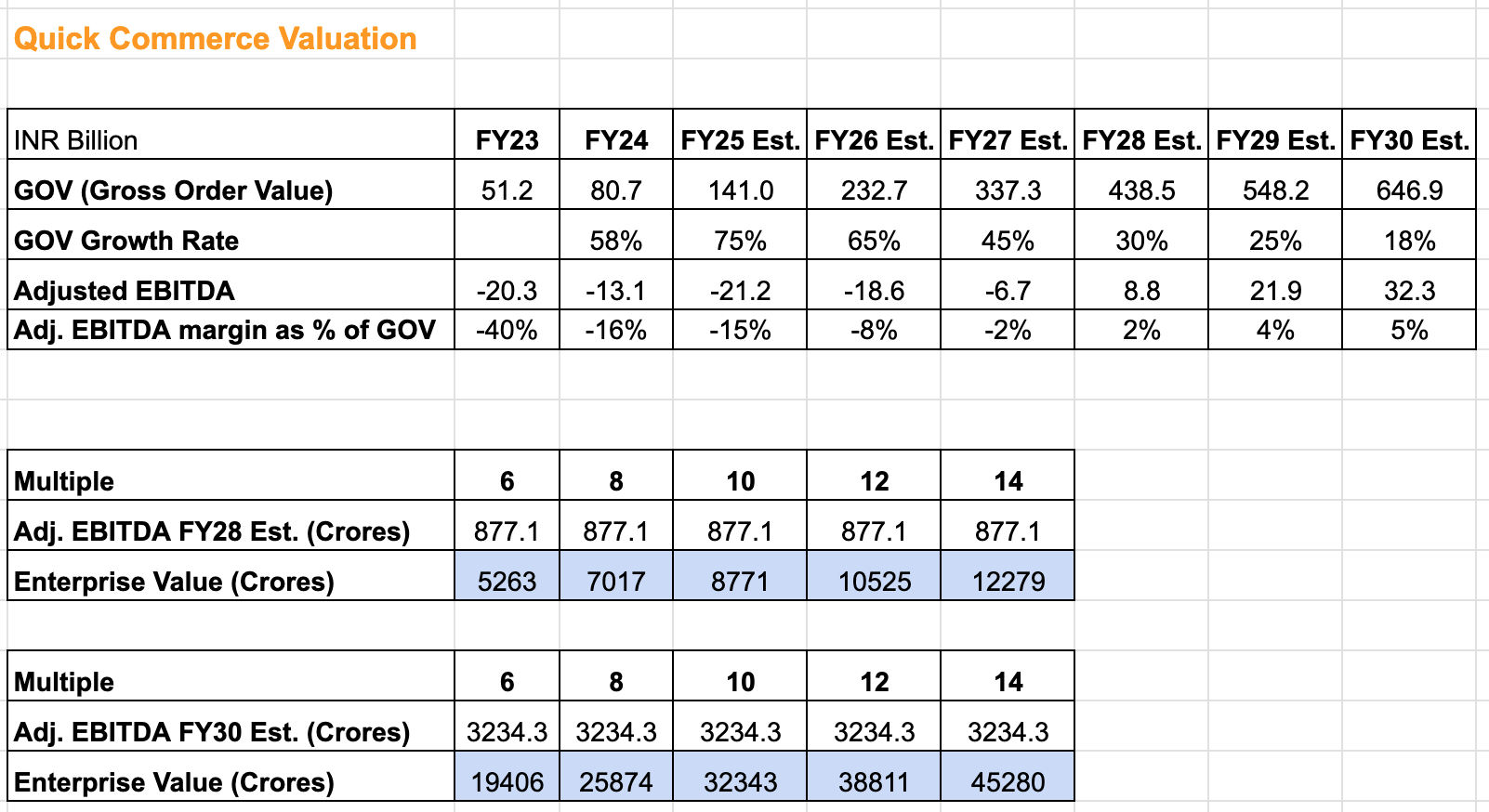

Based on the above trends, if we estimate that the GOV will grow between 75% to 18% for the next five years and the Adjusted EBITDA as a percentage of GOV will trend towards 5%, then we can arrive at an estimated Adjusted EBITDA of Rs. 3,234 Crores in FY30. And if we are to apply a reasonable EV/Adj. EBITDA multiple of 8, we get an enterprise value of Rs. 25,874 Crores based on the FY30 estimated numbers. And if I want to be conservative, I would use the FY28 estimated numbers. And that gives me an enterprise value of Rs. 7,017 Crores.

Source: Author’s estimates

Source: Author’s estimates

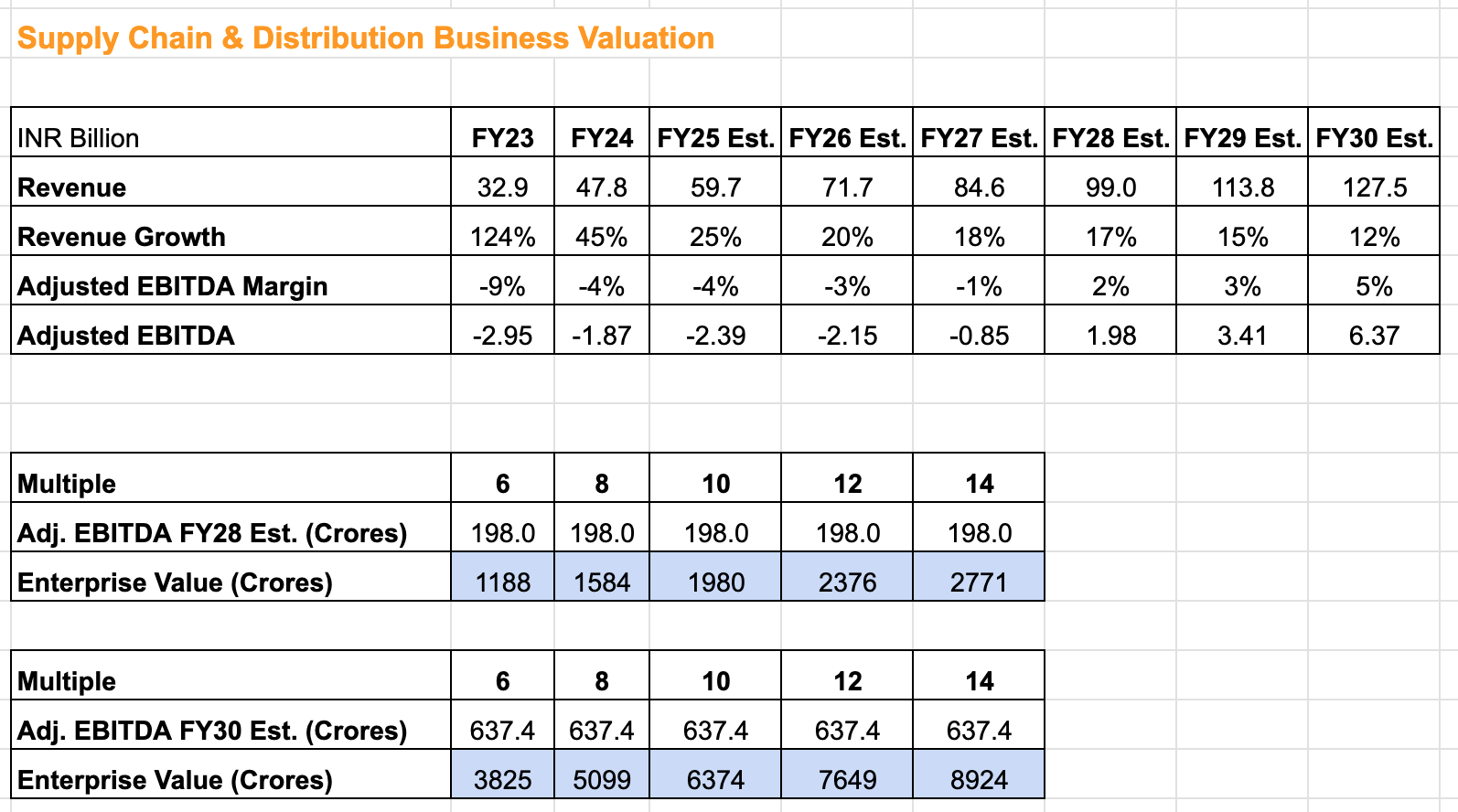

Supply Chain and Distribution

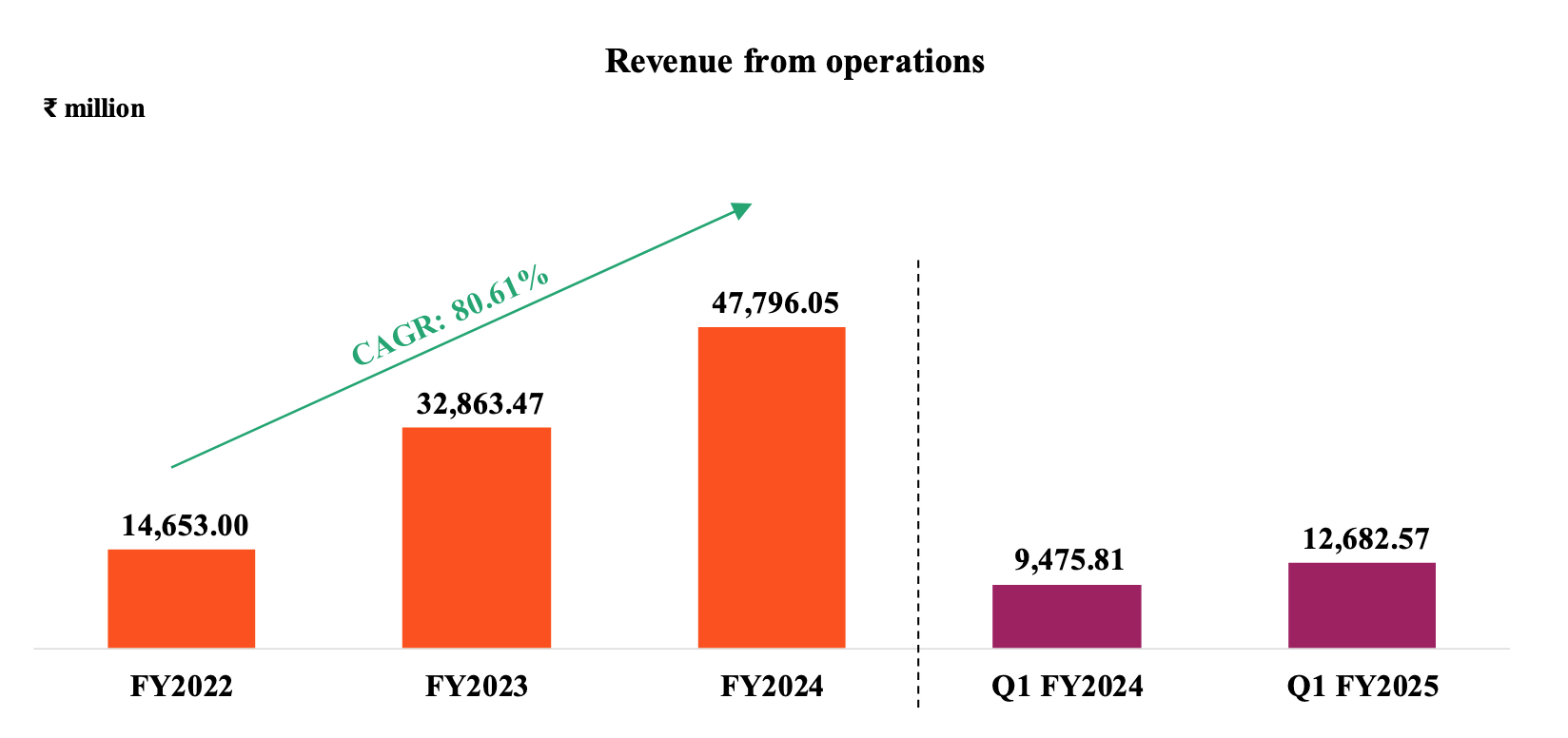

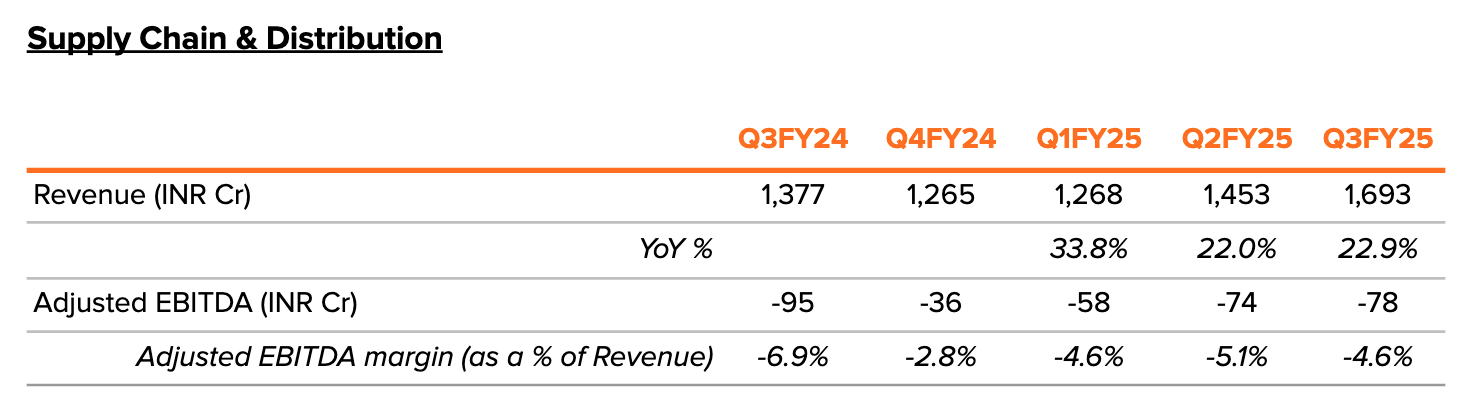

From FY2022 to FY2024, Swiggy’s Supply Chain and Distribution business has grown revenue at a CAGR (Compounded annual growth rate) of around 81%. Source: Swiggy’s RHP

Source: Swiggy’s RHP

If we look at the recently concluded quarter, the Revenue growth has come down to 23%. The adjusted EBITDA margin percentage has remained around -5% for the last three quarters.

Source: Swiggy’s Q3FY25 Shareholder’s Letter

Source: Swiggy’s Q3FY25 Shareholder’s Letter

Based on the above trends, if we estimate that the revenue will grow between 25% to 12% for the next five years and the Adjusted EBITDA as a percentage of revenue will trend towards 5%, then we can arrive at an estimated Adjusted EBITDA of Rs. 637 Crores in FY30. And if we are to apply a reasonable EV/Adj. EBITDA multiple of 8, we get an enterprise value of Rs. 5,099 Crores based on the FY30 estimated numbers. And if I want to be conservative, I would use the FY28 estimated numbers. And that gives me an enterprise value of Rs. 1,584 Crores.

Source: Author’s estimates

Source: Author’s estimatesSwiggy’s Valuation

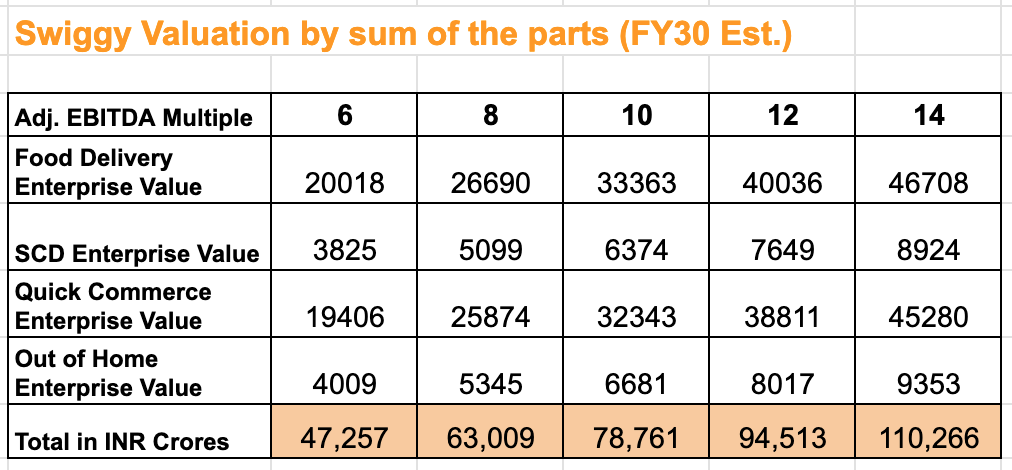

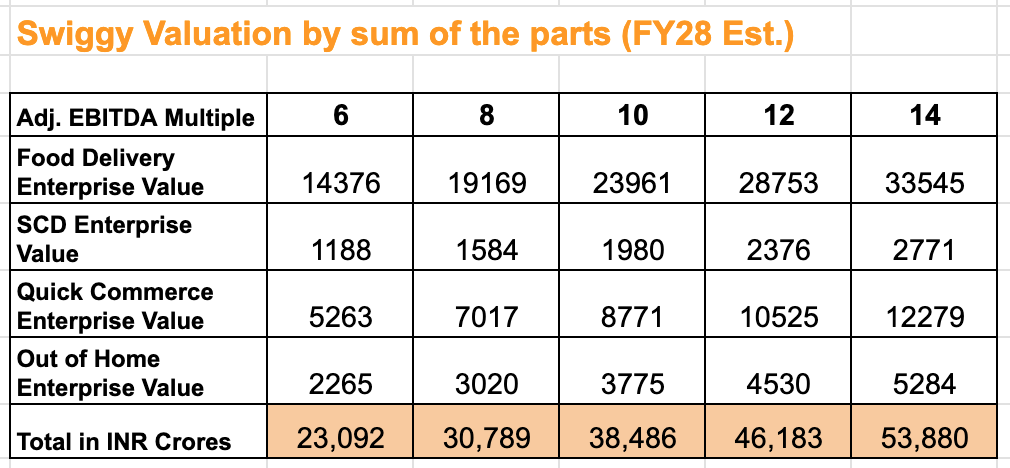

Based on the valuation exercise that I have done above for the four businesses separately, we can arrive at a combined valuation of the company by adding the valuation of the four businesses. If I do the math, I arrive at an enterprise value of Rs. 63,009 Crores assuming an exit multiple of eight times FY30 estimated adjusted EBITDA. If I want to be conservative, I would use the FY28 numbers, which gives me an enterprise value of Rs. 30,789 Crores. The reason one sees such a big difference between the two numbers is the delayed improvement in the adj. EBITDA margin percentage of the Quick Commerce business.

Source: Author’s estimates

Source: Author’s estimates

Since all businesses except the food delivery business are early-stage businesses, and the management is more focused on the growth of those businesses rather than profitability, the assumptions that I have made above for the growth rates and Adjusted EBITDA margin for those two businesses are extremely likely to be wrong.

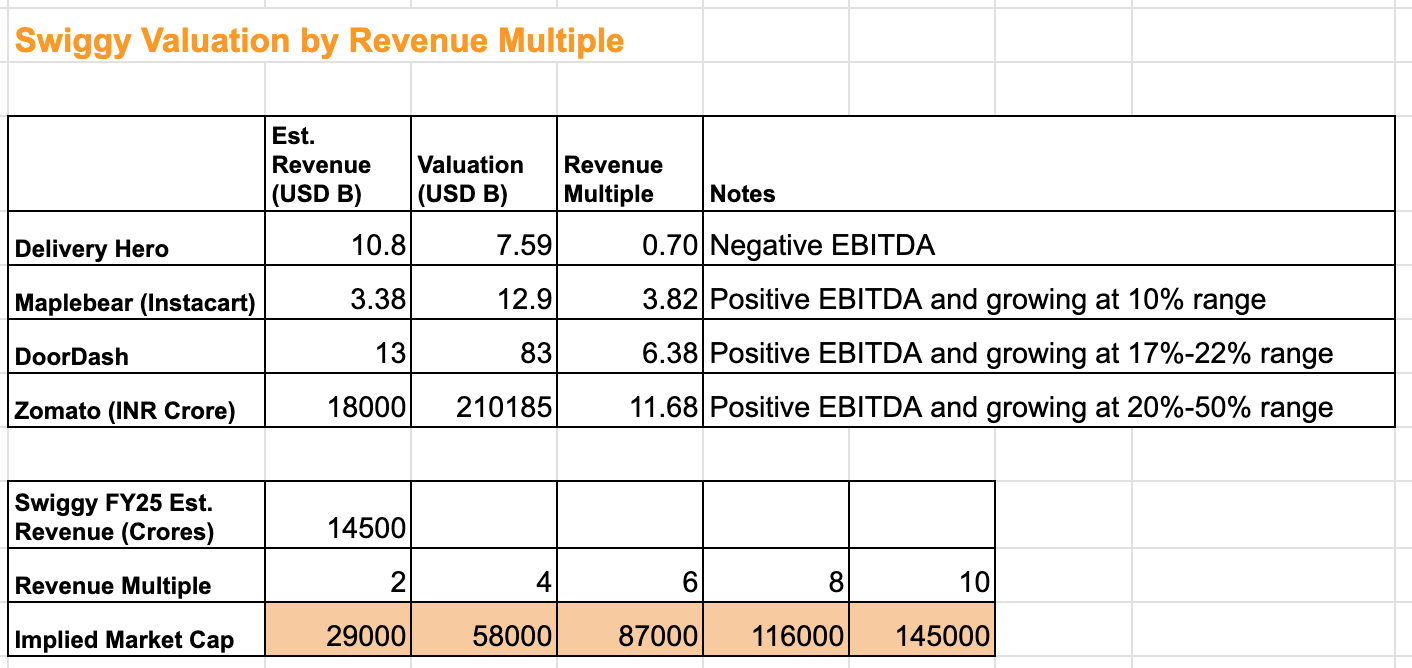

Another way to value Swiggy is by assigning it a revenue multiple based on what other global competitors are currently valued at. In order to arrive at the right revenue multiple for Swiggy, I have looked at three global competitor’s and Zomato’s revenue, public valuation, and growth rates.

Source: Author’s estimates

Source: Author’s estimatesAs you can see from the table, the revenue multiple is higher for companies that are EBITDA positive and have a higher revenue growth rate. Since Swiggy is growing at a decent rate (20%-40%) and is making progress towards being EBITDA positive, I am comfortable assigning it a revenue multiple of 6. So that gives me a Market Cap of Rs. 87,000 crores based on FY 25 estimated revenue assumption of Rs. 14,500 crores. Keep in mind, that Zomato is currently trading at around 11 times its FY 25 estimated revenue.

If you are more pessimistic or optimistic about Swiggy’s prospects, you can vary the growth rates, Adjusted EBITDA margins, and the exit multiples that you assign to arrive at a valuation that you think is right for Swiggy.

Swiggy is currently trading at a Market Cap of around Rs. 77,000 crores.

Risks

Apart from the macro and other obvious risks, below are few additional risks to Swiggy’s businesses.

- Competitors could take away market share and delay the path to profitability by engaging in price wars.

- I have assumed that over the medium to long term, there won’t be a significant difference between Swiggy’s EBITDA & Adjusted EBITDA numbers. However, they could be meaningfully different and my use of Adjusted EBITDA numbers to arrive at an Enterprise value could look like an obvious error.

- Swiggy switched from an all-in-one master app strategy to individual apps for separate businesses. While I think it is the right move, it puts a little bit of doubt in the management’s ability to get the strategy and direction first time right going forward.

- Since Quick Commerce is gaining rapid acceptance across India, it is attracting big established companies like Flipkart, Amazon, etc to the party.

I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

This article is for information and education purposes only. I wrote this article myself, and it expresses my own opinions. I have no business relationship with any company whose stock is mentioned in this article. The facts and opinions appearing in the article do not reflect the views of Thryvv Analytics Pvt. Ltd. and Thryvv Analytics Pvt. Ltd. does not assume any responsibility or liability for the same.