Delhivery: A Leader In Indian Logistics

– Delhivery revolutionized the Indian logistics industry by enabling the Indian e-commerce industry to deliver packages on time, accept payment on delivery, and enable hassle-free returns.

– Delhivery’s IPO price band was Rs. 462 to Rs. 487 (May 2022). And as of March 15th 2024, it is trading for Rs. 436.

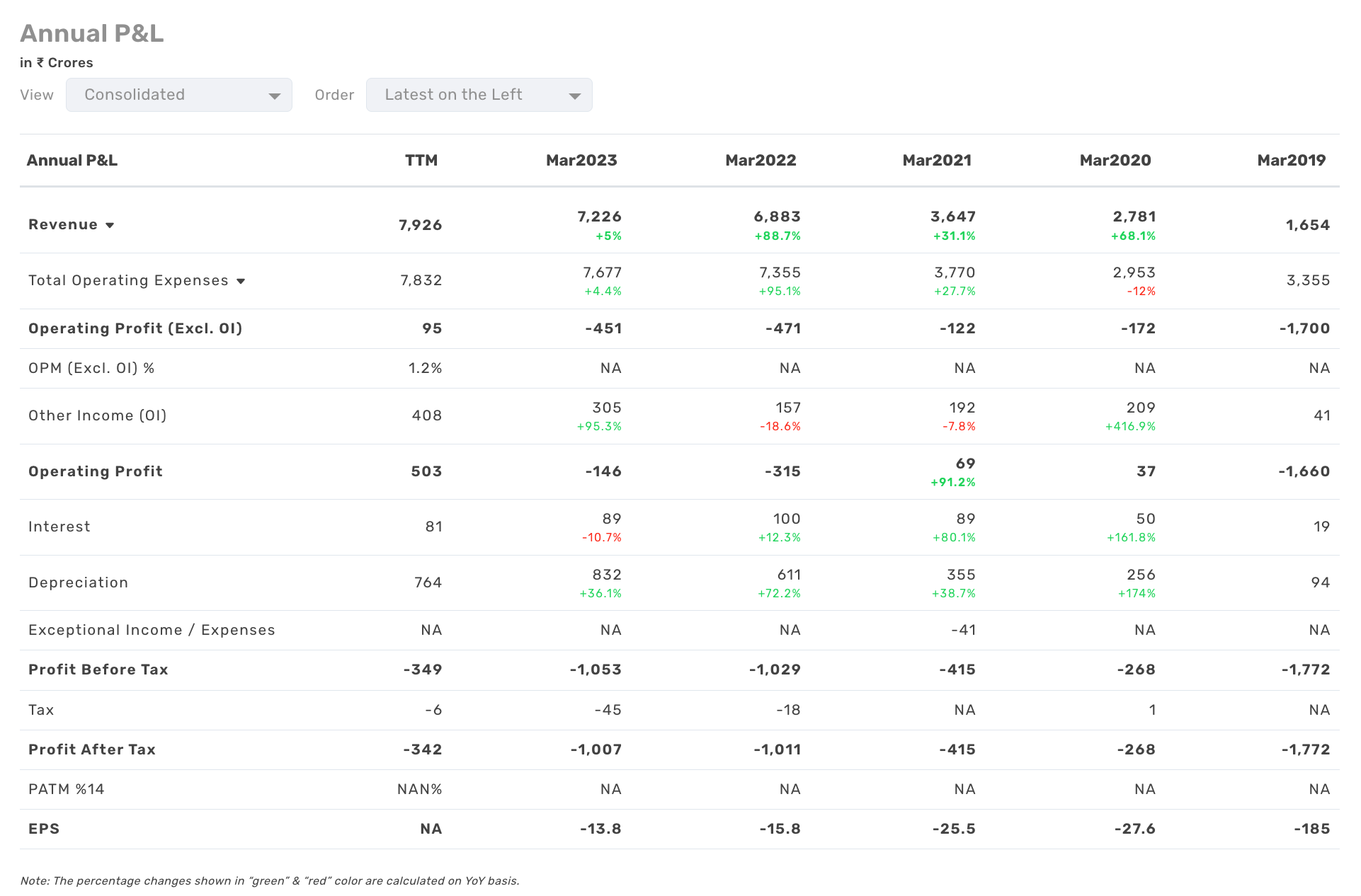

– Delhivery’s revenue has grown from Rs. 1,654 Crores as of March 2019 to Rs. 7,926 Crores as of the trailing twelve months, while also turning profitable as of Q3Fy24.

– A new promising initiative from Delhivery is its OS1 business which is a SaaS (Software as a service) software/API.

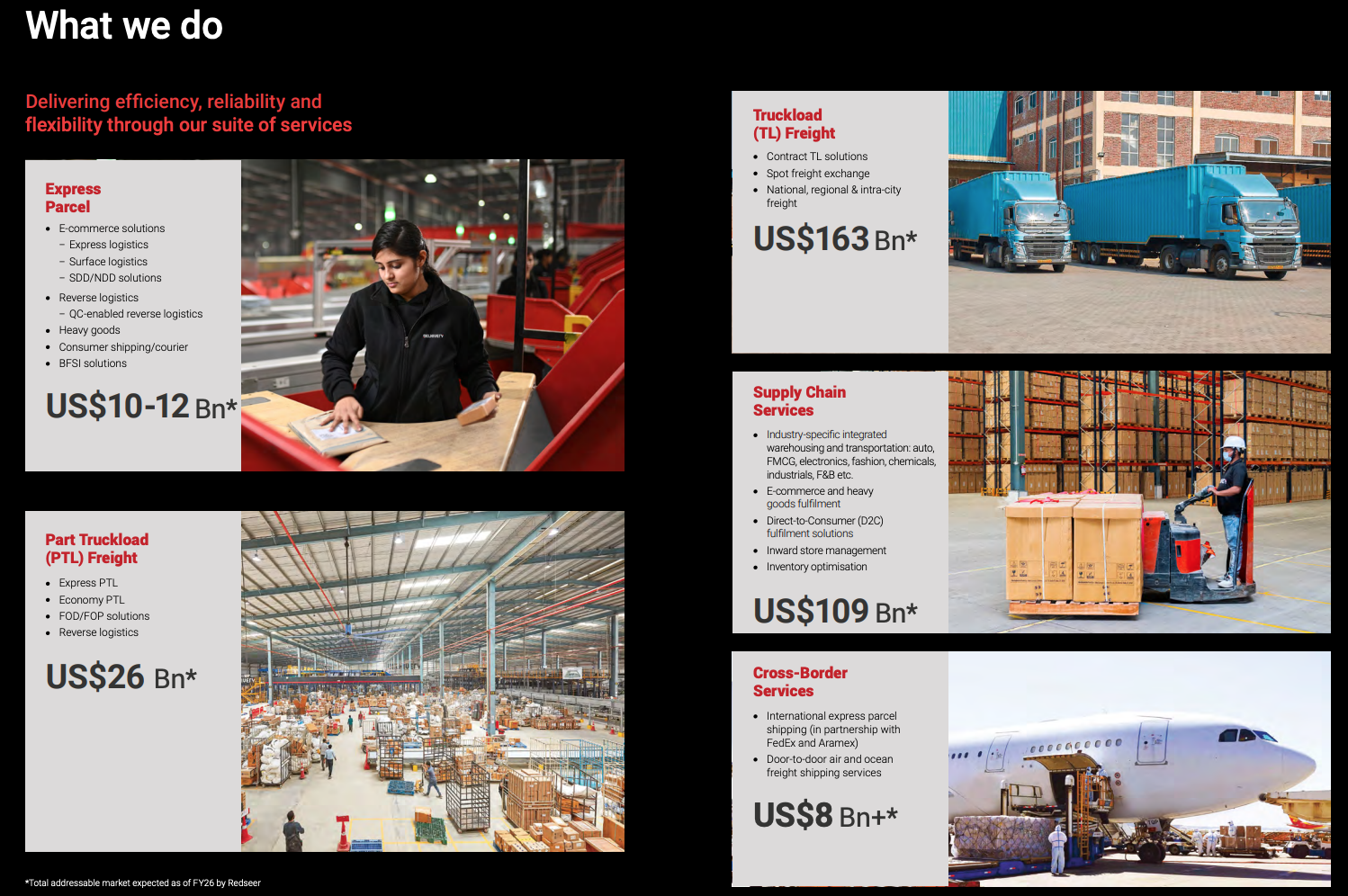

Delhivery is a modern logistics company that offers the following services:

- Express Parcel

- E-commerce solutions

- Express logistics

- Surface logistics

- SDD/NDD solutions

- Reverse logistics

- QC-enabled reverse logistics

- Heavy goods

- Consumer shipping/courier

- BFSI solutions

- E-commerce solutions

- Part Truckload (PTL) Freight

- Express PTL

- Economy PTL

- FOD/FOP solutions

- Reverse logistics

- Truckload (TL) Freight

- Contract TL

- Spot freight exchange

- National, regional, & intra-city freight

- Supply Chain Services (SCS)

- Industry-specific integrated warehousing and transportation: auto, FMCG, electronics, fashion, chemicals, industrials, F&B, etc.

- E-commerce and heavy goods fulfillment

- Direct-to-consumer (D2c) fulfillment solutions

- Inward store management

- Inventory optimisation

- Cross-Border Services

- International express parcel shipping (in partnership with FedEx and Aramex)

- Door-to-door air and ocean freight shipping services

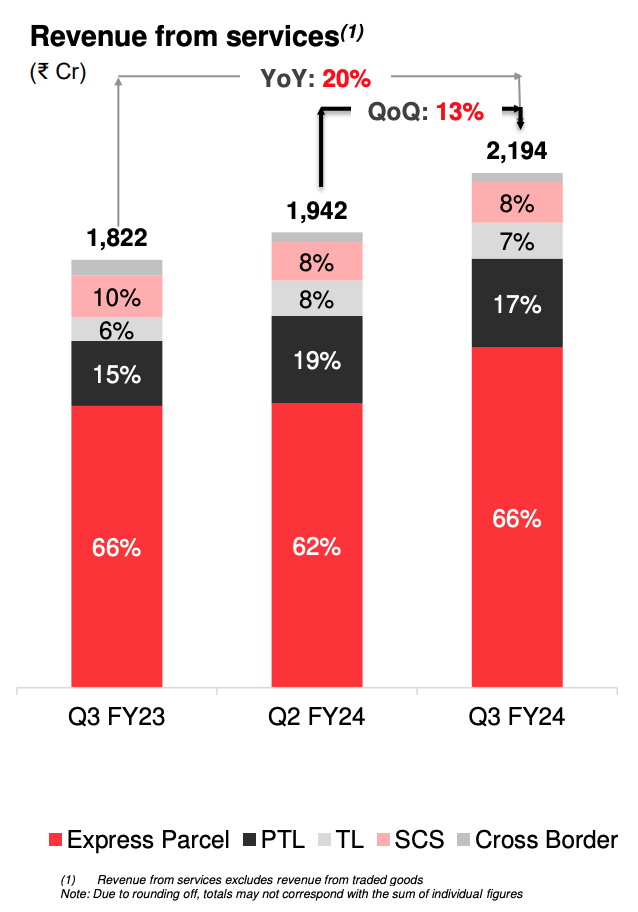

As of Q3FY2024, Delhivery receives 66% of its revenue from the express parcel business, 17% of revenue comes from PTL, 7% from TL, 8% from SCS, and the remaining from cross-border services. Delhivery’s growth story and success are closely linked with the growth and success of e-commerce in India, domestic consumption, and the rise of India on a global stage.

Valuation

Delhivery’s IPO price band was Rs. 462 to Rs. 487 (May 2022). And as of March 15th 2024, it is trading for Rs. 436. At the same time, Delhivery’s revenue has grown from Rs. 6,883 Crores as of March 2022 to Rs. 7,926 Crores as of the trailing twelve months, while also turning profitable as of Q3Fy24.

Delhivery did not make any profits until the last quarter so one cannot value it using the P/E ratio. Delhivery is just coming out of its initial heavy investment phase, so the OPM & PAT margins are nowhere near their true potential.

Current Data

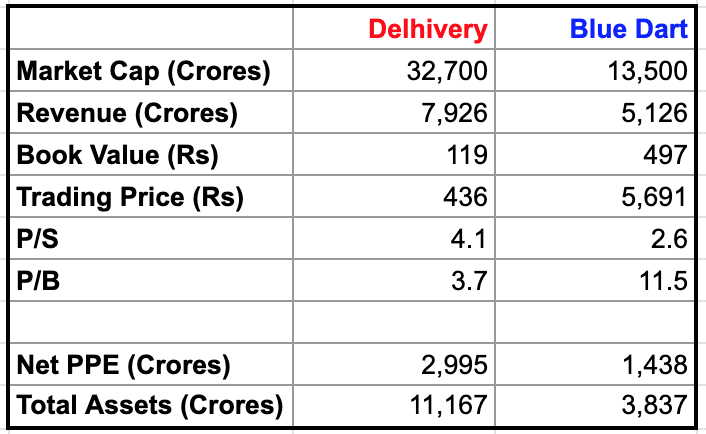

Presently, one can value it based on the P/S and P/B ratio. Delhivery’s current market cap is around Rs. 32,700 crores and its TTM (trailing twelve months) Sales/Revenue are Rs. 7,926 crores. So that gives us a P/S ratio of 4.1. And as of March 2023, Delhivery’s book value was Rs. 119 and it is trading at Rs. 436 as of March 15th 2024. So that gives us a P/B ratio of 3.7.

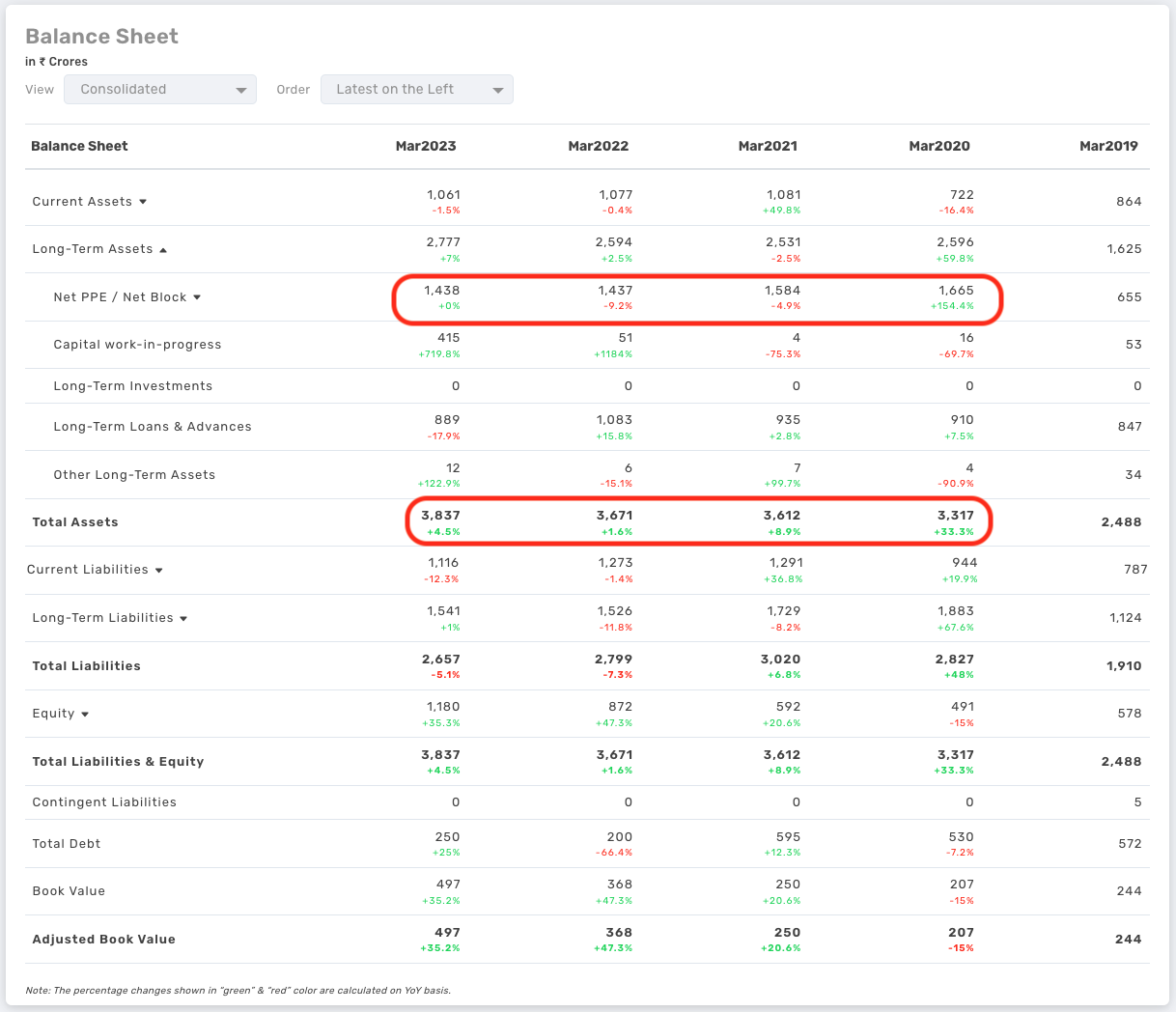

Delhivery’s listed competitor Blue Dart Express Ltd. has a market cap of Rs. 13,500 crores and its TTM sales are Rs. 5,162 crores. So that gives us a P/S ratio of 2.6. And as of March 2023, Blue Dart’s book value was Rs. 497 and Blue Dart is trading for Rs. 5691 as of March 15th 2024, so that gives us a P/B ratio of 11.5.

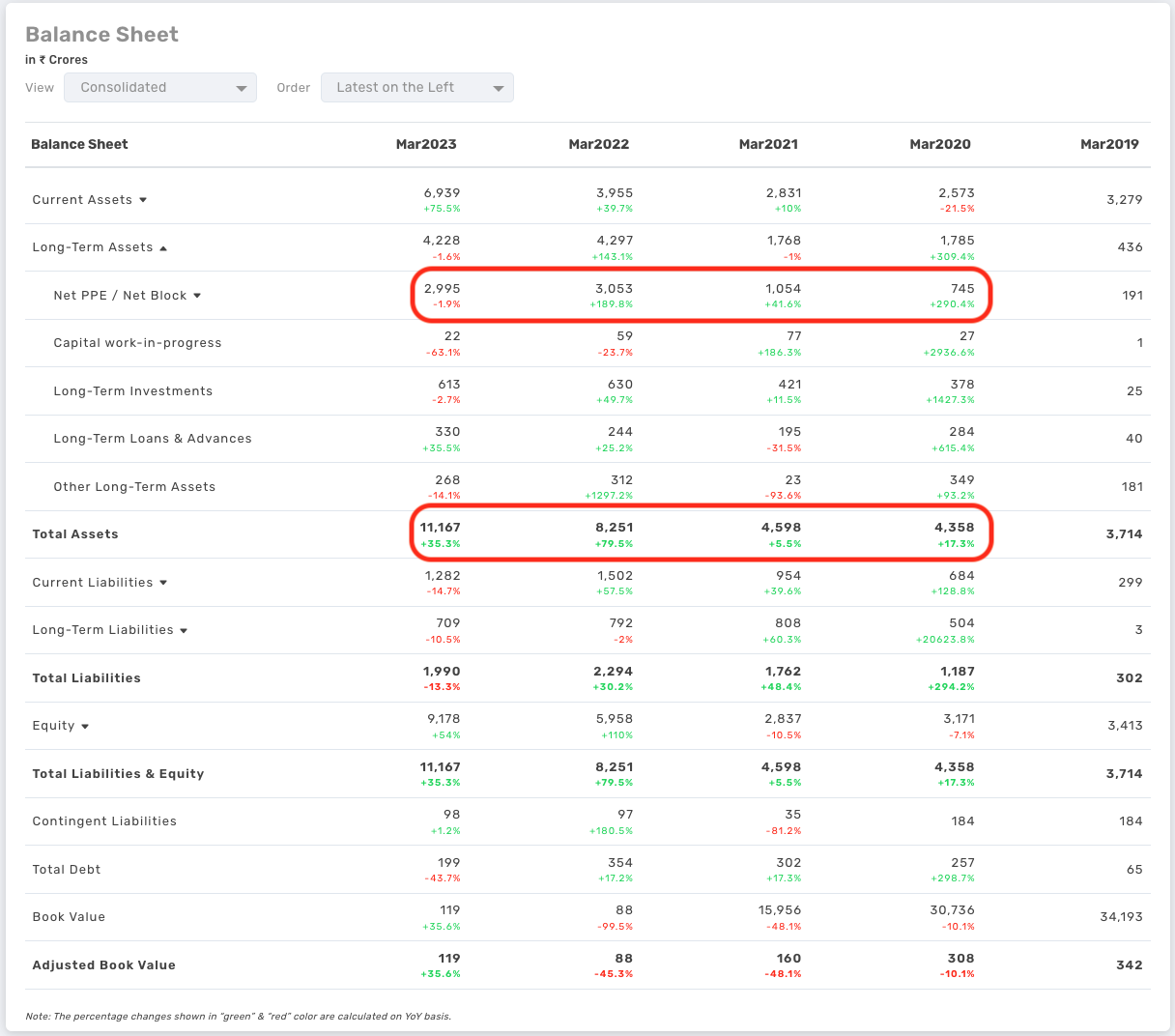

One has to keep in mind that Blue Dart Express Ltd. is a mature company compared to Delhivery and is already operating at an OPM of 18.1% and a PAT margin of 7.2% as of March 2023. Also, looking at the Net PPE & Total Assets of the two companies, one can see that Delhivery has invested a lot over the years in improving its infrastructure while Blue Dart has not. This nicely sets up Delhivery to capture market share going forward.

Delhivery’s Balance Sheet

Delhivery’s Balance Sheet Blue Dart’s Balance Sheet

Blue Dart’s Balance SheetValuation based on P/S Ratio

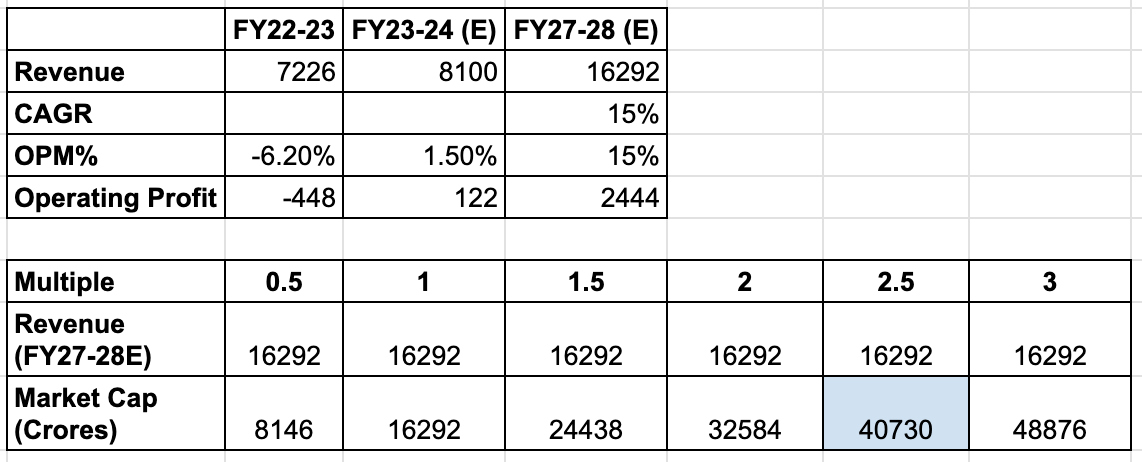

One can also value Delhivery based on the P/S ratio. As mentioned earlier, Delhivery’s publicly listed competitor Blue Dart Express Ltd. currently trades at a P/S ratio of 2.6. So if I assume Revenue CAGR of 15% for Delhivery until Fy27-28, I get an estimated revenue of Rs. 16,292 Crores in FY27-28. And if I assign a 2.5 multiple to that revenue number, I get a Market Cap of Rs. 40,730 Crores for Delhivery.

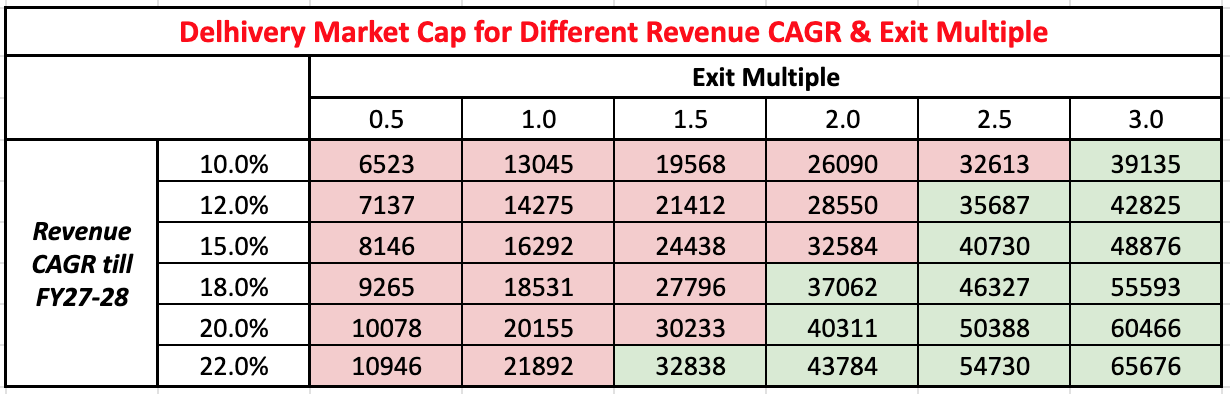

I have also varied the Revenue CAGR between 10% to 22% and the Exit Multiple from 0.5 to 3 and created a table that shows the Market Cap of Delhivery for the various combinations of Revenue CAGR and the Exit Multiple. Based on how optimistic or pessimistic you are about Delhivery, you can arrive at a Market Cap that you feel is right for Delhivery.

Valuation based on Operating Profit

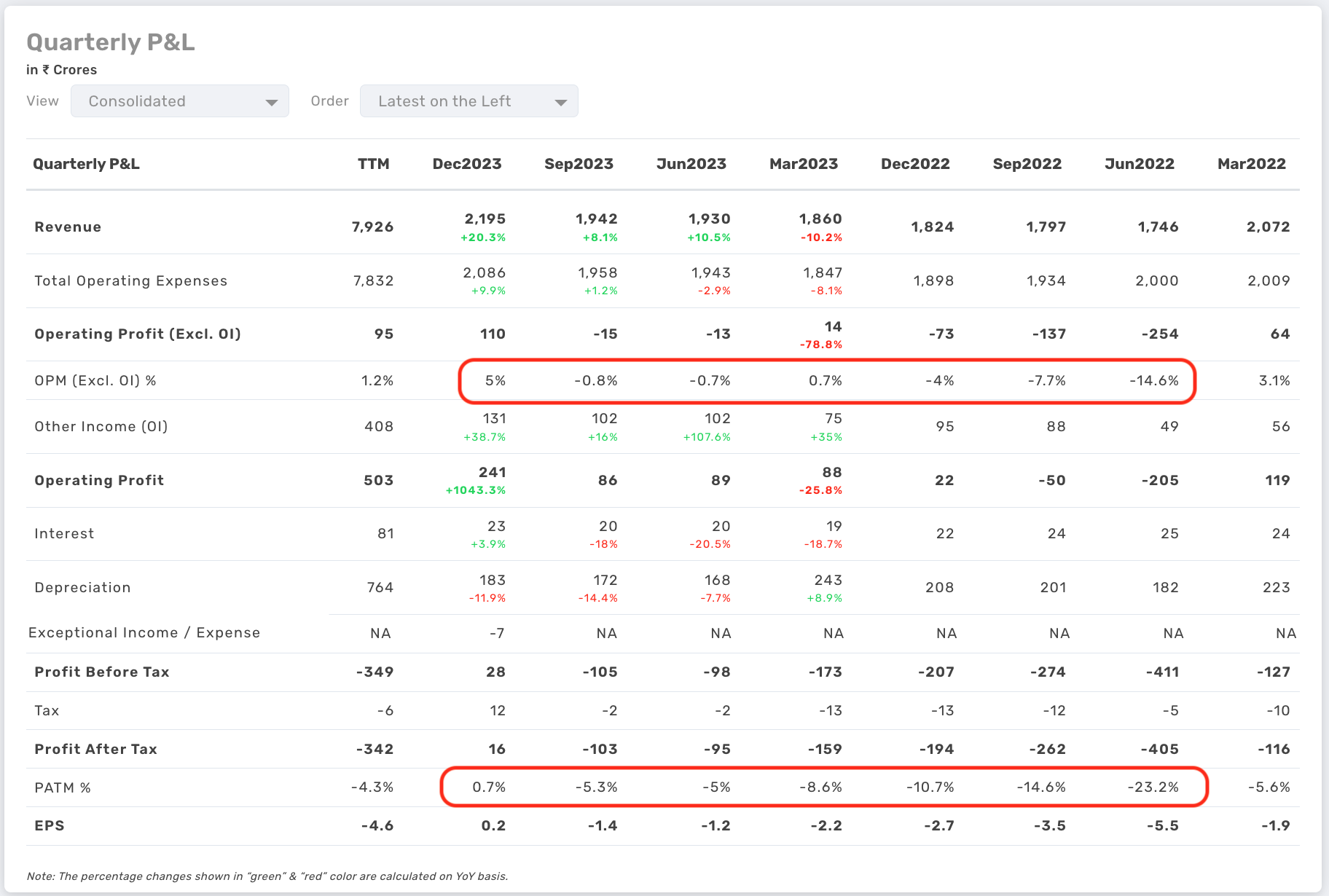

Q3FY24 was the first profitable quarter for Delhivery. The table below shows the OPM & PAT margin improvement from June 2022 to Dec 2023.

Delhivery’s Quarterly P&L

Delhivery’s Quarterly P&LOPM has gone from -14.6% in June 2022 to +5% in Dec 2023. And PAT margin has gone from -23.2% to +0.7% in Dec 2023. This improvement in both margins is expected to continue going forward and OPM will eventually settle between 16-18% over the long term.

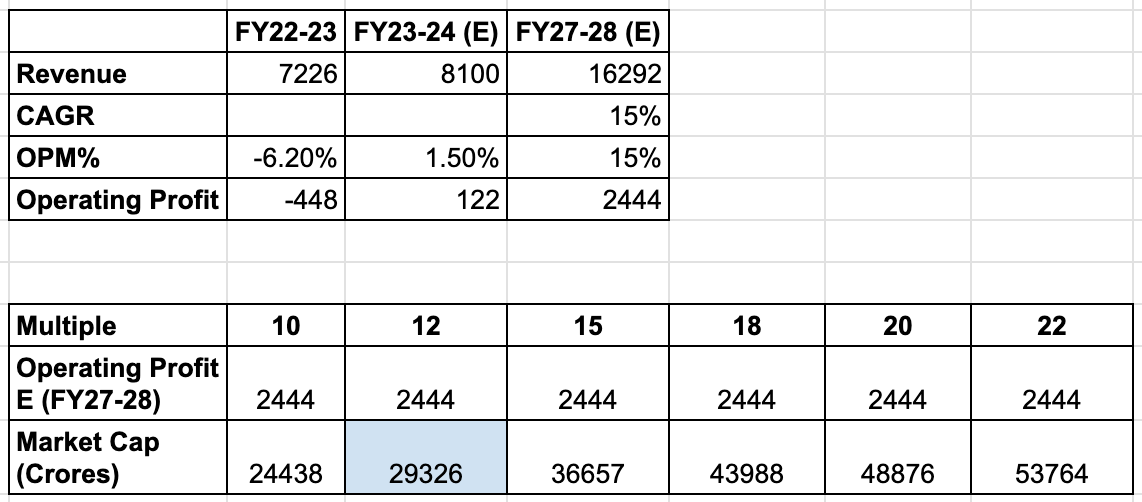

Assuming a revenue CAGR (compounded annual growth rate) of 15% until FY27-28 and an operating profit margin (OPM%) of 15%, I get an operating profit of Rs. 2,444 Crores for FY27-28. And if I use an exit multiple of 12 for FY27-28, I get a Market Cap of Rs. 29,326 Crores.

If one looks at the December 2023 quarter, the OPM% was 5%. And the management is guiding for a long-term target of 16-18%, so it is likely that my 15% assumption may be too low for FY27-28. Also, the management is saying that additional revenue will have an incremental margin of 35% to 50% (operating leverage kicking in), so it is possible that Delhivery reaches 18% OPM% much earlier than FY27-28.

Two more variables that affect the valuation are Revenue CAGR and Exit Multiple. I have gone with a Revenue CAGR of 15% and an Exit Multiple of 12. But you might be a bit more optimistic or pessimistic about Delhivery’s future prospects than I am. Hence, I have created three scenario tables to show the Market Cap by varying these three factors: Revenue CAGR, OPM%, and Exit Multiple.

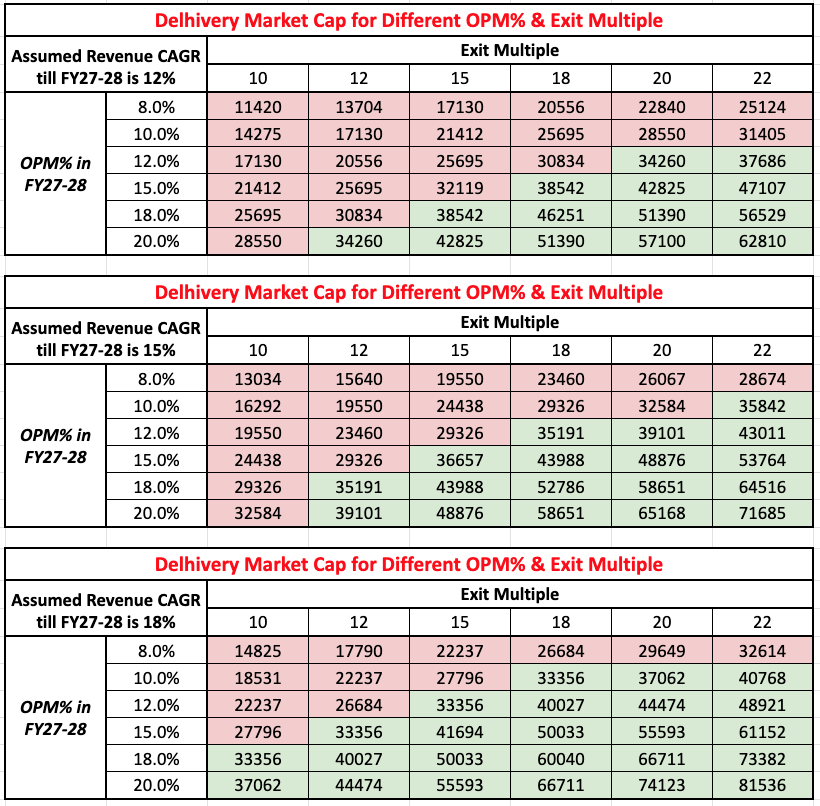

The first table assumes a revenue CAGR of 12% till FY27-28 and shows various values of Market Cap (in Crores) depending on the combination of OPM% & Exit Multiple. The second table assumes a revenue CAGR of 15% till FY27-28 and shows various values of Market Cap depending on the combination of OPM% & Exit Multiple. The third table assumes a revenue CAGR of 18% till FY27-28 and shows various values of Market Cap depending on the combination of OPM% & Exit Multiple.

If one looks at the table, one can see that I get a wide range of values for the Market Cap ranging from as low as Rs. 11,420 Crores to as high as Rs. 81,536 Crores. The Market Cap of Delhivery is Rs. 32,700 Crores as of March 15th 2024. What Market Cap value is reasonable, depends on your assumptions for the Revenue CAGR, OPM%, and the Exit Multiple.

Notes from Q3FY24 Call

I am quoting what the management said on the call and what I understood.

- Yields are best during Q3 of any year due to the seasonality (Diwali shopping, etc). Yields in Q4 are likely to be less than Q3.

- The mix of heavy shipments is likely to keep on increasing. It is a key strategic focus.

- Expect e-comm volumes to keep growing at a long-term sustainable range of 15-20%.

- Capex is 7.5% of revenue. Capex is expected to be marginally lower in FY24-25.

- Management is very confident in their ability to maintain the market share.

- Incremental margins (margins on additional revenue compared to the previous period) are close to 50% and the management expects them to remain so. Incremental margins will come down at some point in time but for the next few quarters, the management expects them to remain around 50%. The reasons for high incremental margins are:

- Utilization has increased from 51% to 63%. And this is expected to keep improving.

- DC capacity utilization is around 45-60% for non-metro and close to 75% for metro regions.

- Tauru gateway was built for 350,000 freight units. Over the years Delhivery has learned to engineer this better and now the same gateway can do 450,000 to 500,000 freight units.

- Delhivery does not expect any significant investment/expansion for the next year.

- Better automation and technology will also help increase the margins

- According to the management, the incremental gross margin will settle at 30-35% eventually. But it is not expected to go below 30%.

- According to the management, the investments that Delhivery needed to make in the PTL business to gain market share and to continue to grow against other organized players have already been made in the past many years. Organized players including Delhivery are only 45% of the PTL market so the market share will keep moving to organized players from the unorganized sector. Delhivery is very optimistic about the PTL sector.

- Delhivery continues to see growth in the top 20 cities. In metro cities, the growth comes from the increase in number of packages being ordered per year by a customer. In India, the number of packages ordered by a person per year is 4 while that is 72 in China. So the management thinks the top 20 cities have not plateaued yet. The management expects that they will keep growing.

- The management thinks that the utilization can reach 70-75% max.

- Traditional logistics companies have always operated with a reverse robinhood strategy. You go to SME customers and make 50% gross margins and you go to bigger accounts and make practically nothing and use them to justify base scale and the network. That is not how Delhivery is organized. Delhivery is set up to make healthy margins with all customers. Delhivery operates the lowest-cost network. Delhivery is expanding the salesforce to significantly expand the base of SME customers and even smaller customers that are classified as retail customers. The management thinks that they are under-served.

- The management does not expect any other significant mega facility to come up soon. There will be minor facility expansion upgrades at a few places.

- Since Delhivery’s competitors are not well integrated across the segments, they cannot offer the prices that Delhivery can offer.

- The management explained that there are two kinds of utilization: 1. the no. of km that you drive and 2. the utilization of the containers aggregated over the trucks. the bigger driver for Delhivery will come from better utilization of the containers. They are already driving a significant percentage of total kms using TT (Tractor Trailer). Utilization has gone up from 20% to 63-64%. Going forward the management expects to get around 70%. With more PTL volume compared to express, the utilization will go up. Careful selection of higher-density clients will also improve utilization. Delhivery’s technology enables them to stuff/fill trucks better (this is a competitive advantage).

- Stable margins over the long term will sit at 16-18%.

- The management continues to see 40%+ incremental gross margins and expects it to continue for some time.

- OS1 monetization should begin from Q1 FY25. We expect OS1 to slowly ramp up over Fy25 and Fy26.

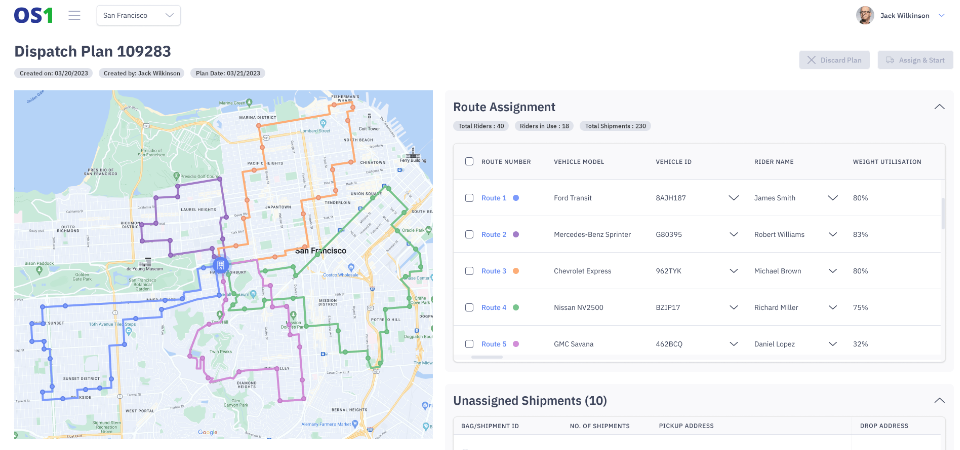

OS1

OS1 is Delhivery’s SaaS (Software as a service) initiative. OS1 is a scalable, easy-to-deploy platform to manage logistics operations. There are three modules: DispatchOne, LocateOne, and RTOne. With DispatchOne, you can automate dispatching operations such as order allocation, route planning, driver operations, and delivery tracking. LocateOne improves the field operations with address standardization, address validation, Geocoding, and reverse geocoding. RTOne is a data-driven returns prediction solution that helps minimize returns.

DispatchOne

DispatchOne enables centralized dispatching. It allows you to consolidate orders across multiple channels – spreadsheet uploads, manual entries, and API integrations with 3rd party systems. View driver availability statuses in real-time and assign orders for dispatch.

DispatchOne helps plan and optimize routes. One can improve on-time deliveries while keeping fuel costs under check with effective route optimization. Generate routes with a single click using Route Optimizer and create efficient plans. Optimize for shipment weight, volume and delivery time-slots while planning routes.

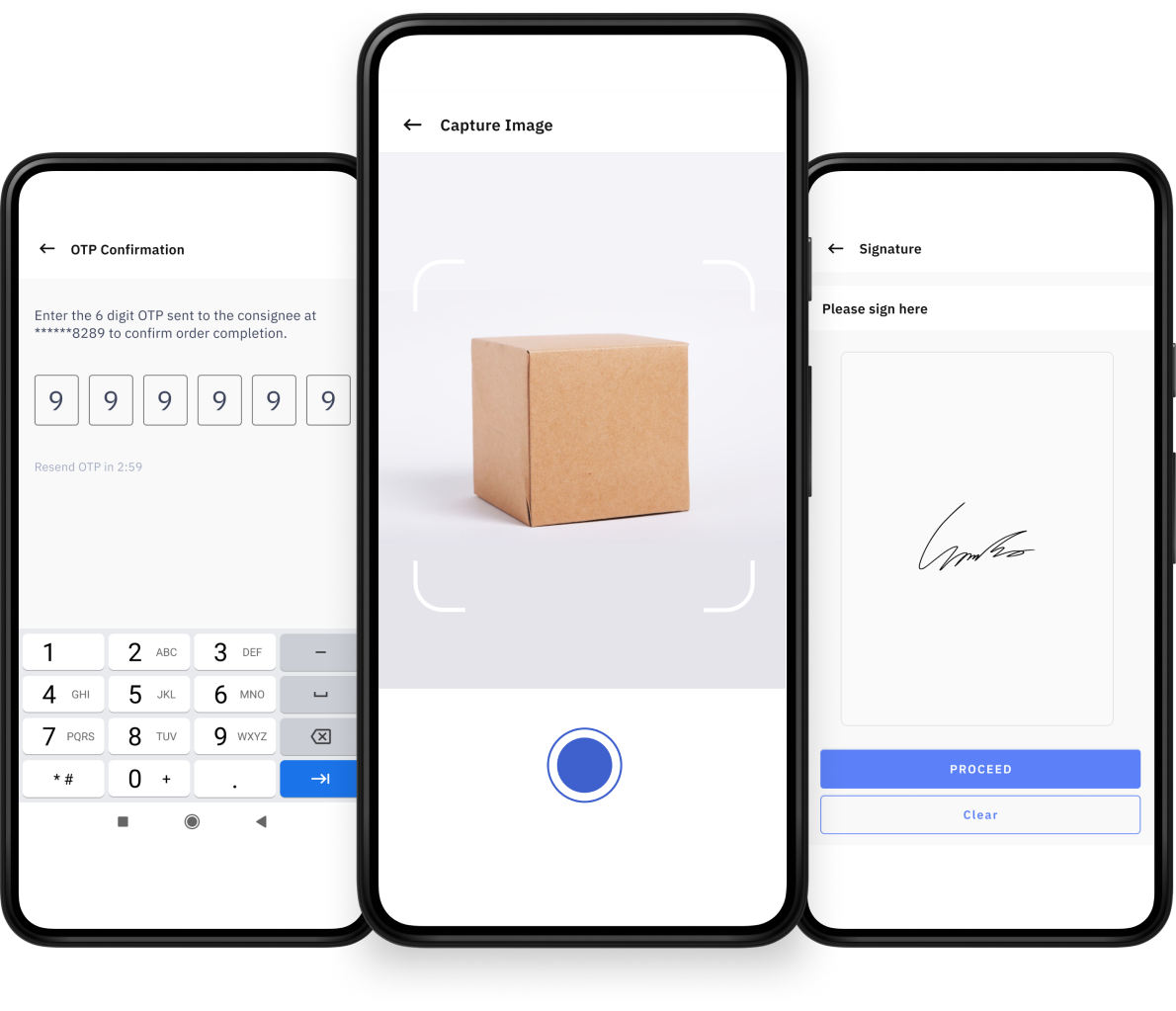

DispatchOne driver app empowers the drivers with an easy-to-use, intuitive mobile app. It enables them to communicate with customers in real-time, mark delivery statuses, and capture proof of delivery on the app.

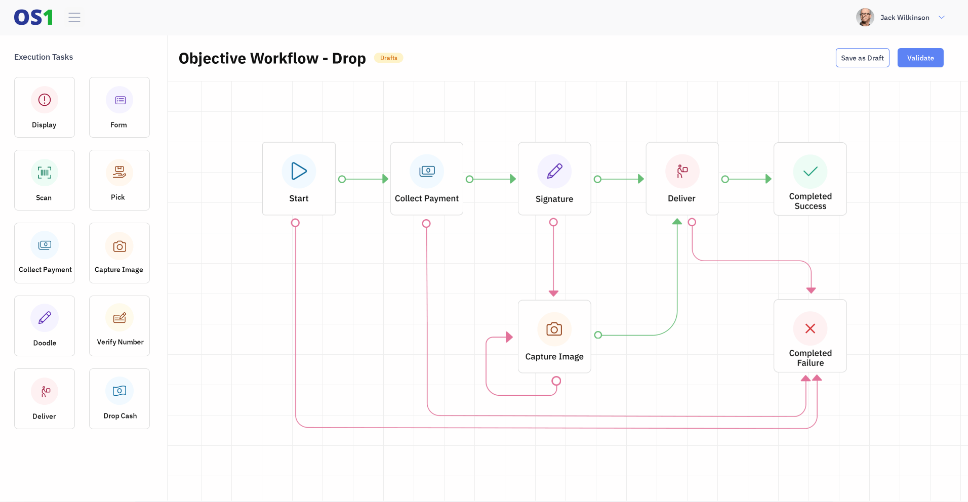

DispatchOne delivery process is configurable. One can design and modify delivery processes using DispatchOne’s drag and drop workflow builder. One can improve driver and customer experience by enabling scanning of the orders, OTP verification, signature verification, or multiple cash on delivery options as per the business requirements. One can roll out process improvements and changes quickly to enhance customer experience and improve operational efficiency.

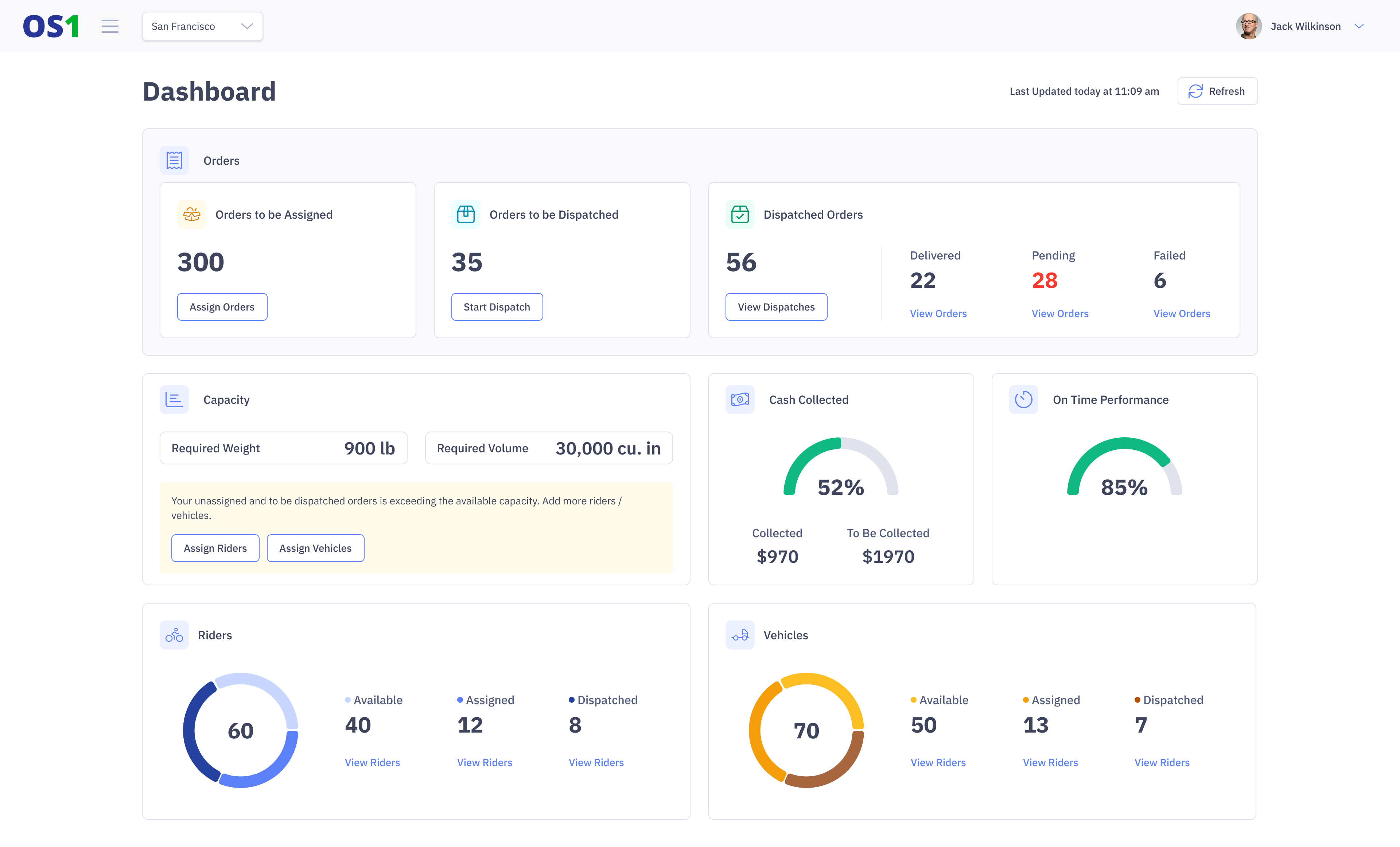

DispatchOne also enables real time order visibility. It allows you to monitor, track, and trace deliveries centrally in real-time. It helps mitigate anticipation anxiety for customers by providing them with real-time updates.

DispatchOne also provides instant proof of delivery. It helps ensure safety and on-time delivery of all orders with real-time electronic proof of delivery. One can get instant updates when the orders are delivered. It allows the collection of contactless signatures, photo proof of delivery, and even validate recipients at the time of delivery.

DispatchOne also provides analytics & insights. It helps identify blindspots and bottlenecks to achieve on-time, cost-efficient deliveries with the help of intuitive reports. It helps meet customer expectations by incorporating process changes and data-driven business decisions based on insightful and actionable analytics.

LocateOne

LocateOne provides address standardization. One can auto-complete addresses by getting accurate information including fields that have not been entered, such as PIN code, Sector etc. It reduces ambiguity and eventually delivery times with standard address formats.

LocateOne also allows you to validate the address that has been entered. It also works as a geocoder and a reverse geocoder. i.e. it gives you the address’s latitude and longitude based on the address and the reverse geocoder converts a given latitude and longitude into a standard address format. This improves the efficiency of field operations and deliveries.

RTOne

RTOne assigns scores to the customers based on insights that are derived from customer delivery behavior across 1B+ (one billion plus) shipments, spanning 18,500+ pin codes pan-India. This allows the seller to make proactive interventions like enabling or disabling COD (cash on delivery), order confirmation through multiple channels like phone calls, SMS & WhatsApp, and minimizing the chances of returns.

With the help of RTOne, one can identify patterns and behaviors pertaining to returns over a period of time and drive critical business decisions on the types of inventory, payment, or delivery options to offer, based on the returns risk. All this helps reduce the rate of returns significantly.

Conclusion

- Delhivery has a strong moat that stems from its world-class logistics infrastructure, automation, technological know-how, and a competent leadership team; all of which enables Delhivery to be the lowest-cost logistics operator while being profitable.

- Delhivery has executed well over the last many years. Delhivery’s revenue has grown from Rs. 1,654 Crores as of March 2019 to Rs. 7,926 Crores as of the trailing twelve months.

- Delhivery also turned profitable as of Q3FY24 and is likely to continue to improve the PAT margins going forward as the operating leverage starts to kick in.

- A new promising initiative from Delhivery is its OS1 business which is a SaaS (Software as a service) software/API.

- Whether Delhivery is undervalued or overvalued is a decision that the reader can make based on the various valuation methods and the assumptions described earlier in this article!

If you haven’t, take a look at Delhivery’s facility videos to see how impressive those facilities are. Also, listen to Delhivery’s MD & CEO Sahil Barua and you will be impressed with his knowledge of the logistics industry and his vision for Delhivery.

Risks

Below are some risks to watch out for (this is not a comprehensive list):

- New or present competitors going after market share at the expense of margins.

- Rising fuel prices and inflationary pressures on wages and assets can impact cash flows and profitability.

- Reliance on partners and other third parties for certain aspects of the business such as first-mile, mid-mile, last-mile services, contractual manpower, fleet etc. poses additional risks to the operations and financial condition.

- E-commerce customers contribute a significant portion of volume and revenue. Accordingly, Delhivery’s business growth is significantly correlated with the growth of e-commerce and more generally, commerce, in India.

- Delhivery obtains a significant portion of the business from a few large customers across multiple services. Their future actions may have an adverse impact on Delhivery’s business.

- Truck driver shortages can disrupt operations and impact the top & bottom line.

I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

This article is for information and education purposes only. I wrote this article myself, and it expresses my own opinions. I have no business relationship with any company whose stock is mentioned in this article. The facts and opinions appearing in the article do not reflect the views of Thryvv Analytics Pvt. Ltd. and Thryvv Analytics Pvt. Ltd. does not assume any responsibility or liability for the same.