Infobeans: A small cap IT company worth taking a look at!

– Infobeans is a small cap IT company that provides digital transformation and product engineering services.

– For the last five years, Infobeans has grown revenue and PAT at a CAGR of 28% and 33% respectively.

– However, the recent revenue growth has come at the cost of deteriorating operating and PAT margins.

Introduction

Infobeans founded in the year 2000 is a small cap IT company that operates in two categories; namely “Digital Transformation” and “Product Engineering”.

The digital transformation part of the business focuses on providing design, development, and other related services in the areas of Cloud, UX, Application modernisation (digitisation of legacy applications and dependencies), packaged implementation, and enterprise mobility.

The product engineering part of the business focuses on providing design, development, implementation, sustenance and other related services for Robotic Process Automation (RPA) (via its partnership with UiPath), Salesforce, Servicenow, Continuous Integration and Continuous Delivery (CICD) and Agile Testing Framework (ATF), Content Management System (CMS), Automation, and Data transformation.

Story so far

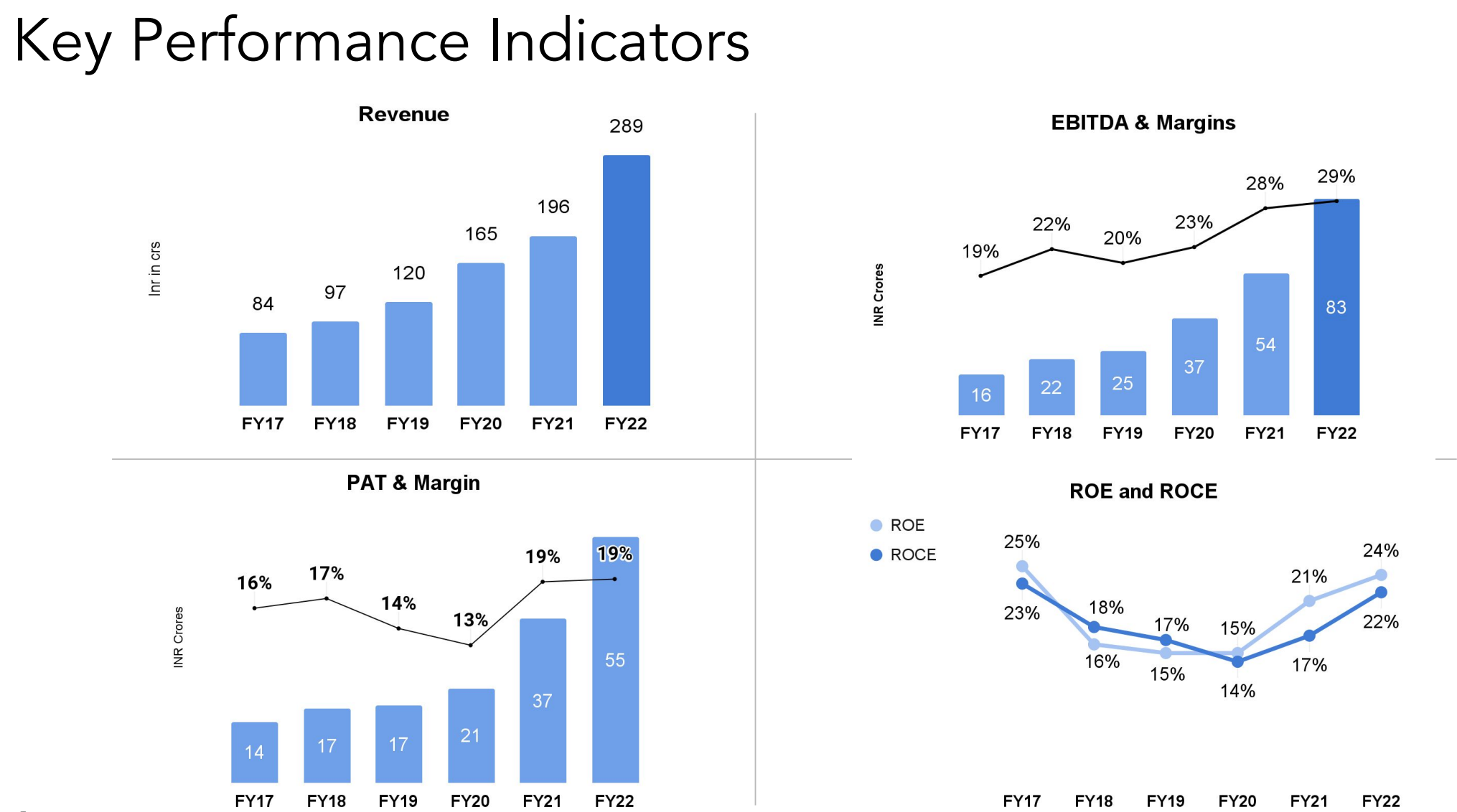

For the last five years, Infobeans has been able to grow revenue, EBITDA, and PAT at a CAGR of 28%, 41%, and 33% respectively. A part of the growth can be attributed to the post COVID boom that happened in the IT industry.

Source: Infobeans investor presentations Apr-June 2022

The growth has been a mix of organic expansion and inorganic acquisition. The two acquisitions; namely Philosophie in 2019 and Eternus in 2021, are doing well and contributing to the growth. Both acquisitions have given the company access to a number of enterprise clients. InfoBeans is now working with 14 organization with over a billion $ in revenue in comparison to 6 organizations in March 2022.

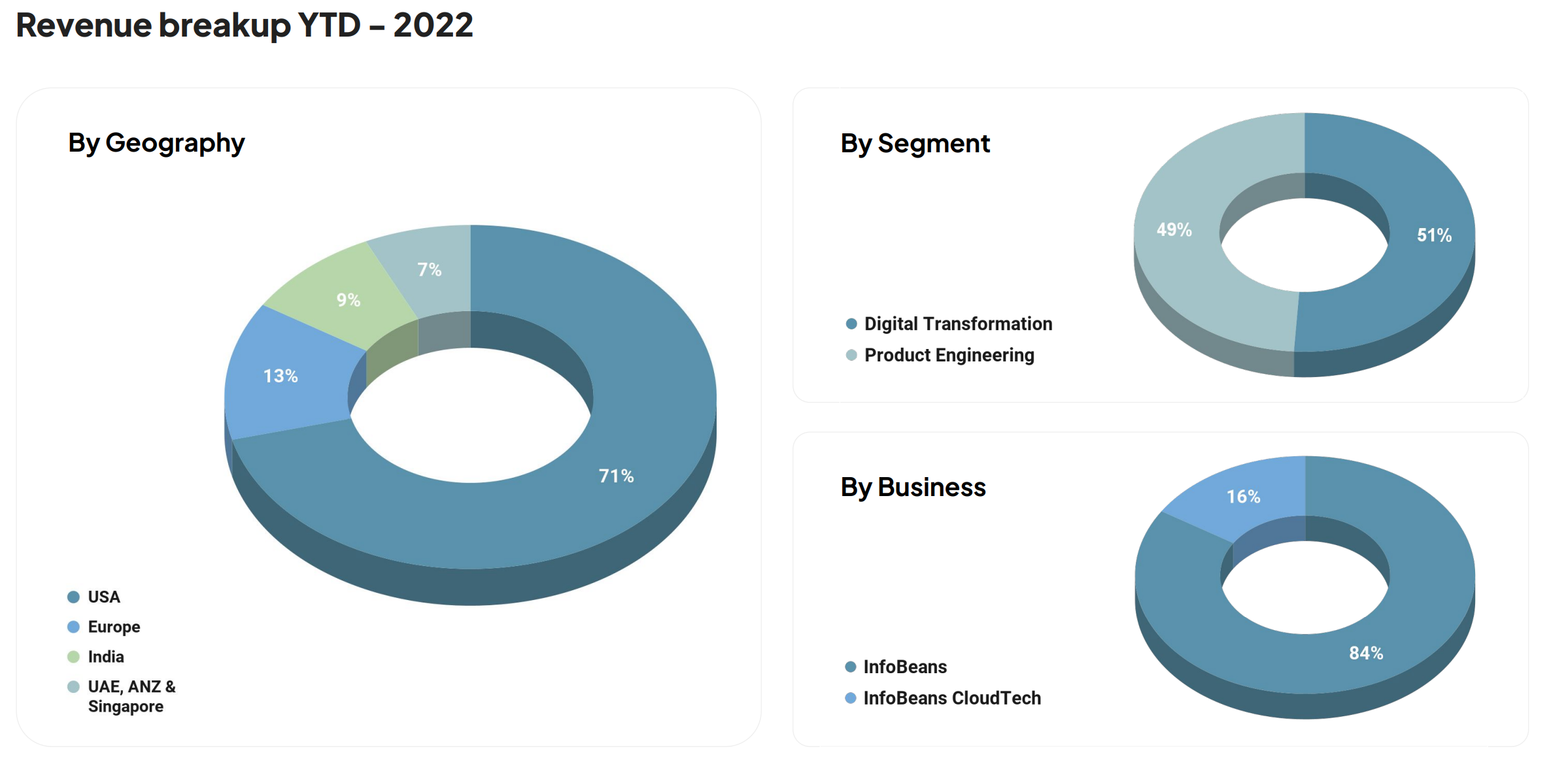

The image below shows Infobeans revenue breakup by geography, business segment and business unit.

Source: Infobeans investor presentation Dec 2022

Source: Infobeans investor presentation Dec 2022

Path Forward

Management has highlighted that for organic growth their main focus is on the land and expand model. The management plans to leverage the Salesforce and Servicenow partnerships to gain access to large enterprise clients and then cross sell other services.

The management is looking for inorganic acquisition targets in USA and is also looking to expand into new emerging technologies like AI, ML, metaverse, blockchain technology, etc.

The management team has stated that for the last 10 years they have doubled the revenue in every three year cycle and they aim for that to continue going forward.

Infobeans Valuation

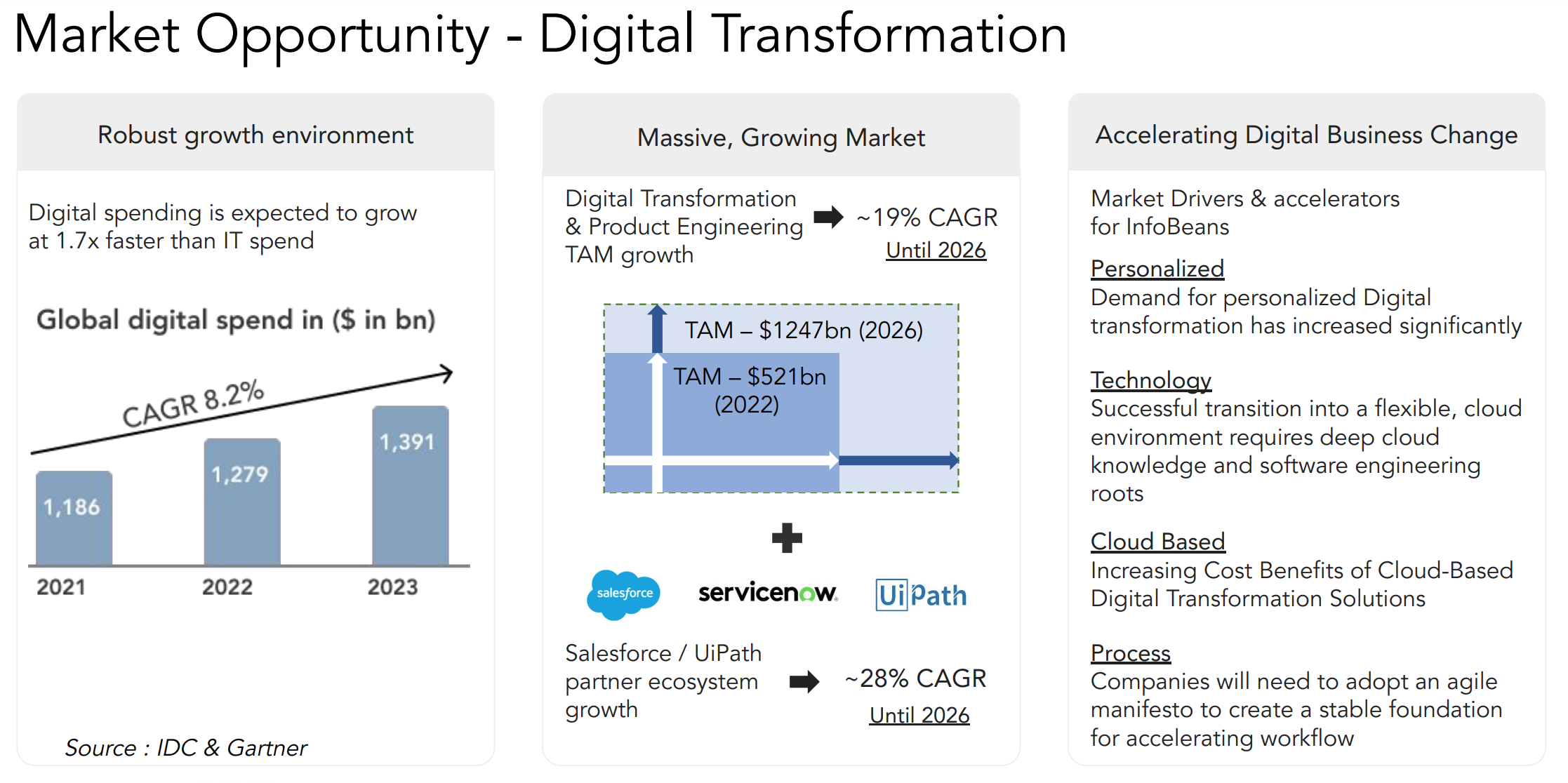

If I calculate the PE ratio based on the trailing twelve months EPS, Infobeans is currently trading at a PE ratio of approximately 22. And if one takes a look at the market opportunity that Infobeans addresses, one can see that the market is expected to grow at a CAGR of 19% until 2026.

Source: Infobeans investor presentations Apr-June 2022

Source: Infobeans investor presentations Apr-June 2022

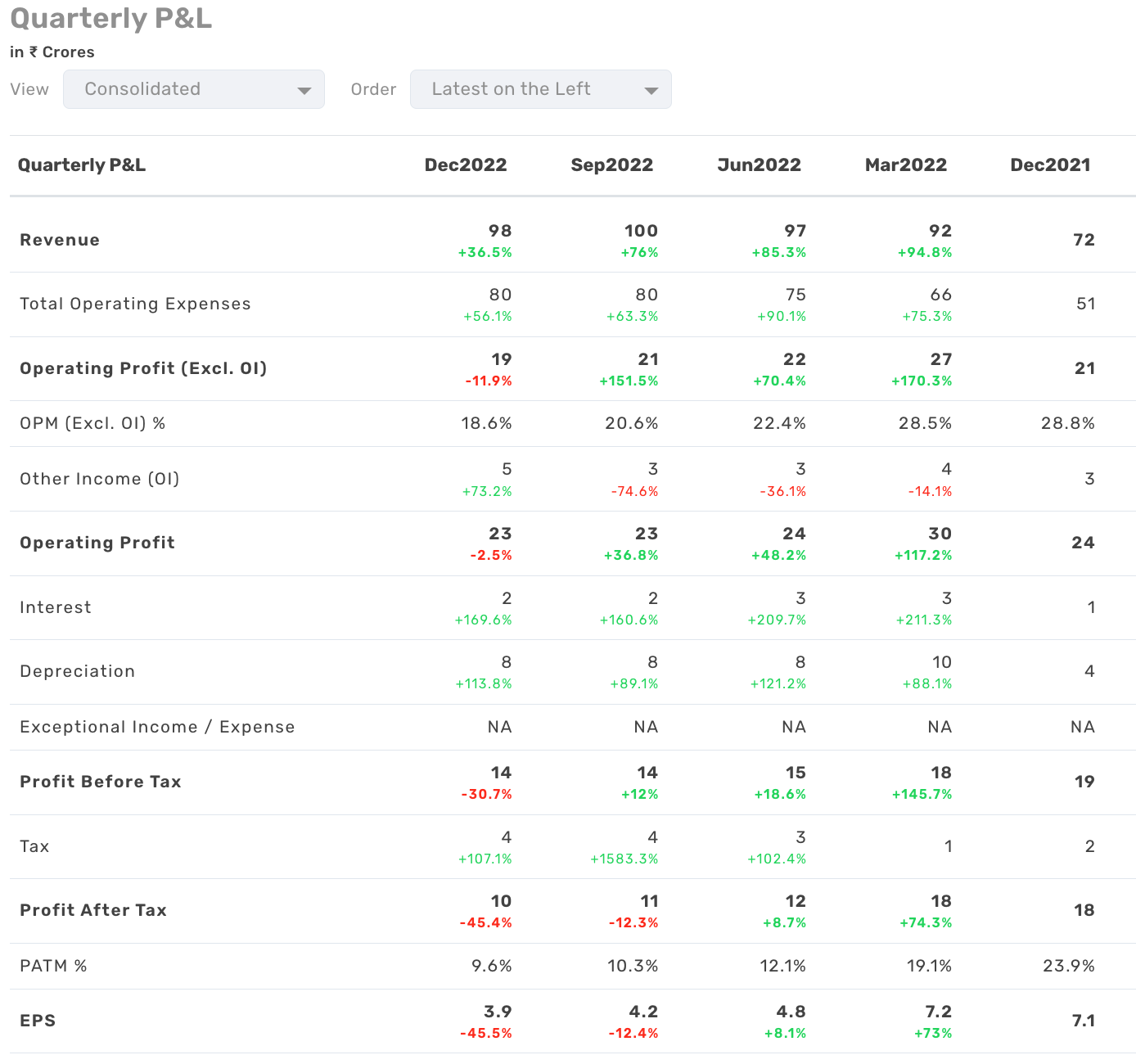

However, for the last few quarters the operating and PAT margins have contracted significantly and it can be a cause of concern if the trend continues long term. One can see that the OPM has contracted from 28.8% in December 2021 to 18.6% in December 2022. Also, the PAT margin has contracted from a high of 23.9% in December 2021 to 9.6% in December 2022.

The management has given few reasons for the decrease in the margins:

- The post COVID boom increased the cost of hiring and talent retention.

- They have intentionally focused on growing the top line while sacrificing the bottom line in the short term.

- Infobeans had an approx. INR 7 crore grant (other income) in September 2021.

- Acquisition (Eternus Solutions) cost is also a factor in the margin reduction.

The management expects the cost of hiring and talent retention to normalize soon and that will help with improving the margins going forward. However, for the upcoming quarter management has mentioned that they will be hit by a one time retention bonus that they had agreed to in the past. So, margins are likely to look bad for the upcoming quarter.

Infobeans’s balance sheet is strong with little to no debt.

Infobeans Management

Infobeans is still run & managed by its three founders who are still young and hungry for more. All three founders have so far shown the ability to execute and create a work culture that is admired. This is evident from the numerous awards and recognitions that Infobeans has received as a “Great place to work”.

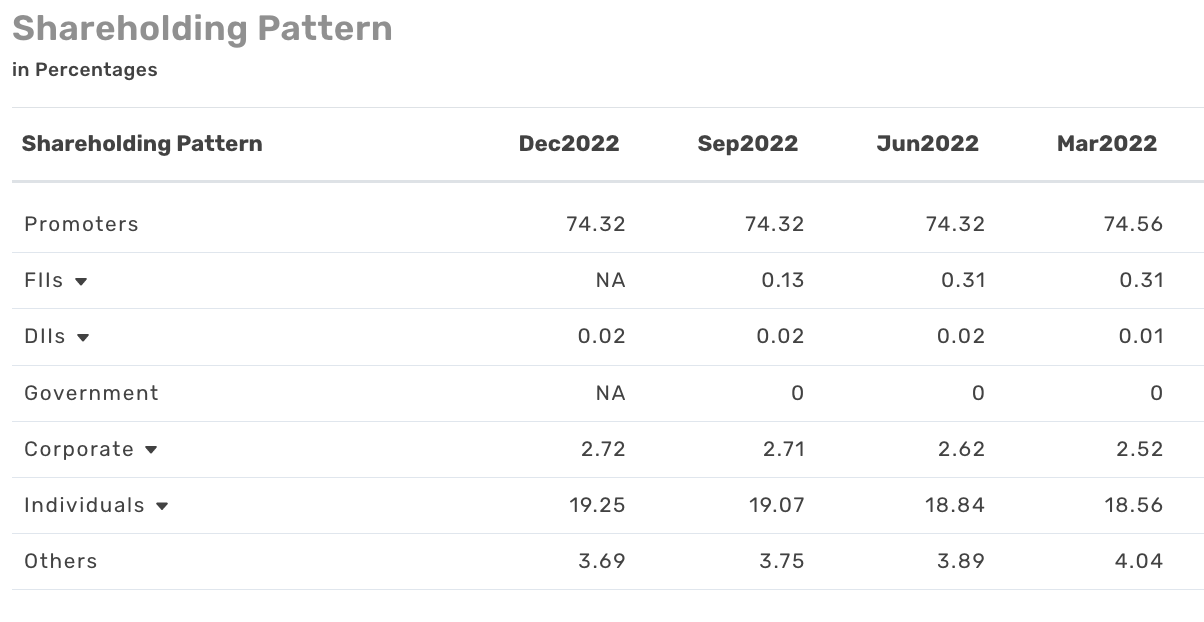

The founders also own a significant portion of the company at around 75%. And institutional holding is almost nil. If the company, keeps on executing, institutions will start participating, potentially resulting in a rerating of the company in the long term.

Headwinds

- Macro environment could derail the growth.

- Global or US recession could have a big impact on Infobeans as 71% of its revenue comes from the USA.

- If the operating and PAT margins do not show improvement in the next few quarters, investors are likely to move away from the company assuming it was a one time beneficiary of the post COVID boom that lifted the entire IT sector.

- Retention bonus hitting in the upcoming quarter could put pressure on the margins in the short term.

- The current slowdown in IT spending and budgets could last longer than anticipated.

I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

This article is for information and education purposes only. I wrote this article myself, and it expresses my own opinions. I have no business relationship with any company whose stock is mentioned in this article. The facts and opinions appearing in the article do not reflect the views of Thryvv Analytics Pvt. Ltd. and Thryvv Analytics Pvt. Ltd. does not assume any responsibility or liability for the same.

This article should not be taken as an investment advice. Please consult your investment advisor before making a financial decision.